-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Bosideng (3998.HK) - Product integration improves profitability, Domestic down brands continue to upgrade

Tuesday, August 10, 2021  4589

4589

Bosideng(3998)

| Recommendation | Accumulate |

| Price on Recommendation Date | $5.630 |

| Target Price | $6.220 |

Weekly Special - 2333 Great Wall Motor

Investment summary

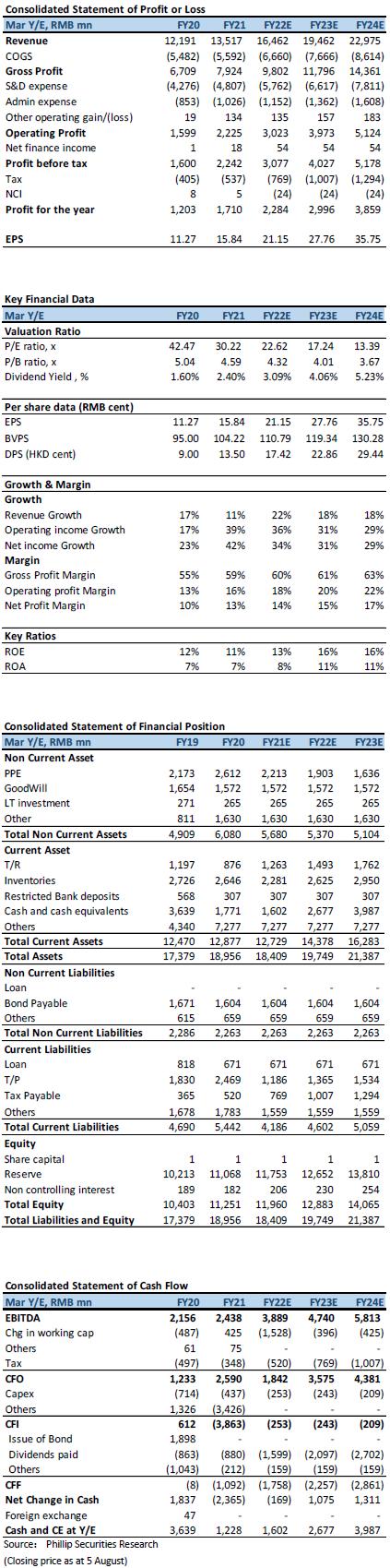

The company announced its annual report for the FY20/21 on July 21. Revenue increased by 10.9% Yoy to CNY 13.52 billion, which was lower than our expectation. The net profit attributable to the parent for the year was CNY 1.71 billion, an increase of approximately 42.1%, beat our expectations. It mainly due to the decrease in the company's expense ratio during the period and the increase in profitability. The company declared a final dividend of HKD 10.0 cents per share. The total dividend for the year was HKD 13.5 cents, with a dividend payout ratio of 70.8%.

The company's brand down revenue increased, main brand down improve company GPM

The company's performance was generally in line with expectations. In terms of revenue, it was lower than our expectation. The company's annual revenue recorded approximately CNY 13.52 billion, which was 5% lower than our expectation. The main reason was that the company's branded down jacket wholesale business revenue was lower than our expectation. The company's net profit recorded approximately CNY 1.71 billion, which beat our expectations and was 12% higher than our expectations. This was mainly due to the improvement in product efficiency and the decrease in the proportion of company expenses during the period under the operating leverage. The company's net profit growth faster than revenue growth was also due to the improvement in GPM. The company's overall GPM for the 2020/21 fiscal year was approximately 58.6%, an increase of 3.6 ppts compared to the same period last year. The GPM of the branded down apparel business increased by 3.9 ppts compared to the same period last year. As the self-operated proportion of Bosideng down jackets has increased, it will greatly help increase the GPM.

Improved inventory level, product integration strategy improves product efficiency further

During 2020, the company will mainly focus on handling inventory issues in FY2019/2020. During FY21, the company strategically reduced wholesale sales and actively adopted destocking measures. In addition, China was affected by the early winter and other climates last year. Solving inventory problems within the scope of controlled discounts has limited impact on profitability. The company's inventory level at the end of FY21 was CNY 2.65 billion, a Yoy decrease of 2.9%. The inventory turnover days increased by about 20 days to 175 days compared with last year. This was mainly due to the fact that the beginning inventory was affected by the epidemic, which was at a relatively high level, and the impact was about 12 days. In addition, in order to cooperate with the company's new replenishment measures, the proportion of raw materials in the inventory has risen sharply, accounting for 30% of the total inventory (16% in the same period last year), which will affect the inventory turnover days of about 8 days; if excluding raw materials, the company's inventory turnover days are about 127 days, and the company's long-term goal is 100-110 days (excluding raw materials).

The company will carry out product integration reforms in 2020 to improve the company's supply chain and inventory issues in the long run. It was mainly implemented in self-operated stores last year. In terms of distributing goods, in the first batch of distributing goods, for different stores and users, distributing goods according to their store status, and the quantity is also controlled below 30% of the expected sales; the implementation of quick return and replenishment, the products in store sold every day will be replenished the next day, quick sell and quick replenishment; further improve pull production, from the previous quick return to production 20-25 days to 5-7 days production, to achieve 10-day pull return orders; strengthen O2O ecology, both online and offline channels share the same inventory to further improve the efficiency of goods. The company plans to further implement the product integration policy to franchisees in FY22. In the future, franchisees only need to order the first batch when they place an order, and replenish the goods when the product is sold. In addition, the franchisee is also allowed to exchange new products before the specified period. It helps improve product efficiency on the one hand, and effectively improve terminal inventory levels on the other.

Valuation and investment advice

Bosideng's earnings this year beat our expectations. In solving the inventory problem, it strategically reduced the proportion of its wholesale business. As a result, the revenue from branded down jackets was lower than our previous expectation (previously expected: CNY 11.89 billion), but the company further improved its product efficiency. Profitability has risen sharply. In the coming year, the company plans to further promote product integration to franchisees. Under strict inventory management, it will effectively avoid the possibility of the company needing to increase retail discount in the future. The future profitability will be more stable, and the target online and offline discounts will not be discounted. The company plans to further upgrade its channels, from business-oriented to brand-oriented, and strive to become high-end, aiming to build 2+13 cities (Beijing and Shanghai plus 13 new first-tier cities). We adjusted the company's future revenue forecasts and profitability, lowered the company's FY22E/FY23E revenue to CNY 16.46/19.46 billion, raised the company's FY22E/FY23E EPS to CNY 21.15/27.76 cent, and raised the target price to HKD 6.22 corresponding to FY22/FY23 24.99x/19.05x expected P/E. Considering the current price level, maintain the Accumulate rating.

Investment risk

-The development of women's clothing business is not as expected

-Increased industry competition

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()