-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Hongkong & Shanghai Hotels (45.HK) - Premium Hospitality & Leisure Services Provider

Thursday, January 5, 2017  17066

17066

Hongkong & Shanghai Hotels(45)

| Recommendation | Accumulate |

| Price on Recommendation Date | $8.460 |

| Target Price | $9.700 |

Weekly Special - 002050 Sanhua

Worldwide Top Tier Hotel Brand

Hongkong & Shanghai Hotels primarily operates in hospitality and leisure services segments and about 73% of its revenue in 1H2016 comes from the hotel segment. The company is most well-known for its famous hotel chain, Peninsula Hotel. Peninsula Hotels are located in the large major cities in North America, Europe and Asia and the footprints of Peninsula Hotels can be found not just in Hong Kong, but also in Tokyo, Paris, New York and Chicago. In total, Peninsula Hotels have over 3,000 available rooms with about 2,200 available hotel rooms in the Asian continent, contributing to about 70% of the total available hotel rooms of the whole group and about 70% of the total revenue of the hotel segment across years. In particular, the Hong Kong segment of Peninsula Hotel has been the company's main revenue engine, with about 24% of the revenue generated by Hong Kong Peninsula Hotel in 1H2016. The company's hotel operation business does not only include the hotel room leasing business, but also include food and beverage, the shopping arcade and the associate office building leasing business. In particular, these arms of the hotel business contribute to about 46% of the hotel operation segment revenue in 1H2016.

Apart from the company's hotel operation business, the company also engages in the investment property business, with residential, retail and commercial properties available for leasing. The investment property business generates about 17.5% of the total revenue in 1H2016. In particular, the residential arm of the investment property generates a majority of its revenue, most of which are generated by the residential property in Repulse Bay, Hong Kong and with a GFA of almost 1,000,000 square feet. The company has an ownership percentage of 100%.

Expansion to European Continent

According to the diagram below, Peninsula Hotel has strong presence mainly in the developed cities in Asian and American continents. However, the company has a lack of presence in the developed European region and has only one hotel in Paris. The company has been actively expanding to the European continent. In December 2015, the company announced that the London Westminster Council has approved the company's proposal to build the new hotel, `The Peninsula London`, at Grosvenor Place. Further in 26/7/2016, the company has acquired the full attributable interest of `The Peninsula London`. `The Peninsula London` will provide 190 hotel rooms and up to 28 residential apartments, each come with their own leisure and spa facilities. Besides the company will also build 23 intermediate affordable home nearby. The hotel and the apartments will be completed in 2021.

The company has also been preparing to break into the Middle East region by setting up a joint venture with other company to invest EUR150Mn for the development of `The Peninsula Istanbul`. Besides, the company has acquired 70% majority interest for the hotel development project, `The Peninsula Yangon` in Myanmar. The project consists of the development of a hotel complex as well as a residence complex, `The Peninsula Residences Yangon`. The master lease of the site for `The Peninsula Yangon` has been signed on 23/7/2016.

We believe these projects will not only allow the company to break into the European region and the Southern Asian region, but also allows the company to generate sizable revenue, given London being the heart of Europe and the district near the hotel site being the traditional luxurious residential area. Moreover, Istanbul is also one of the most popular destination for travel in Middle East and we expect the hotel to become one of the important milestone for the company's expansion.

Hotel Segment Performance

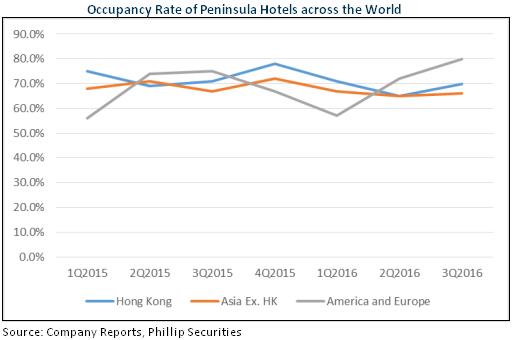

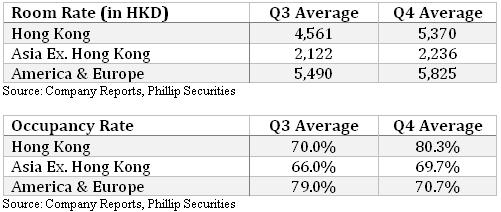

Hotel occupancy rate in general has improved in 3Q2016 in comparison with 2Q2016, with the Peninsula Hotels in American and European continents continuing its 3-quarter consecutive growth in occupancy rate from 57% in 1Q2016 to 80% in 3Q2016. The hotel occupancy rate in Asian region has dropped slightly due to the renovation work being carried out in the Beijing hotel. The occupancy rate in Hong Kong has improved from 65% in the 2Q2016 to 70% in 3Q2016. We expect the occupancy rate to further improve for the reason that the fourth quarter is a traditional holiday season and fourth quarter result consistency outperformed the result in third quarter in the past for most of the regions.

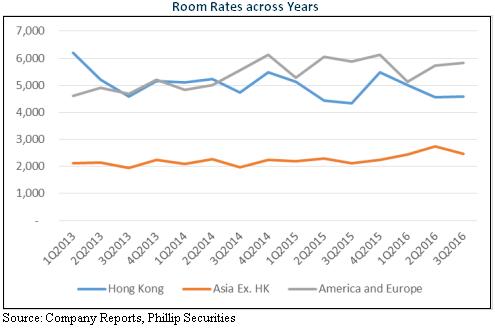

The following is the average room rates in each quarter the company charges.

Apart from hotel in Hong Kong, which has shown a deteriorating trend in room rate ever since 2013, Hotels in other continents has a general rising trend, as evident by the average room rates for hotels in Asia has risen from the 3-quarter average of HKD2,064 in 2013 to the 3-quarter average of HKD2,552 in 2016. For the hotels in America and Europe, the 3-quarter average room rate has risen from HKD4,732 in 2013 to HKD5,572 in 2016. However, the one for Hong Kong has dropped from HKD5,333 in 2013 to HKD4,718 in 2016.

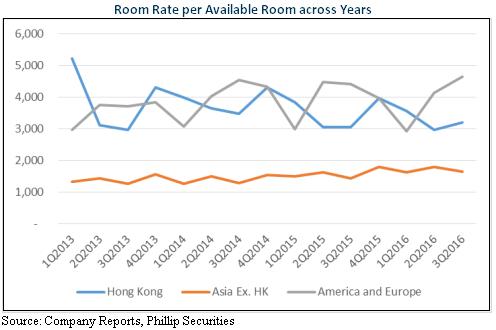

We expect the room rates per available room to improve in the fourth quarter of 2016 and rise above that of the third quarter of 2016. Traditionally, the room rate in the fourth quarter is much higher than the room rate in the third quarter in all regions while occupancy rate is higher in the fourth quarter than in the third quarter in all regions except America & Europe.

Despite the fact that the room rate being traditionally higher in the fourth quarter, we expect the Hong Kong region performance not to reach 2013 high in both occupancy rate and room rate perspective because of Renminbi, the currency which the majority of the Hong Kong overnight visitors use, has depreciated by a large amount ever since it reached its high in 2014. This will affect the purchasing power these tourists have in Hong Kong, thereby affecting the demand for top tier hotels.

Financial Analysis

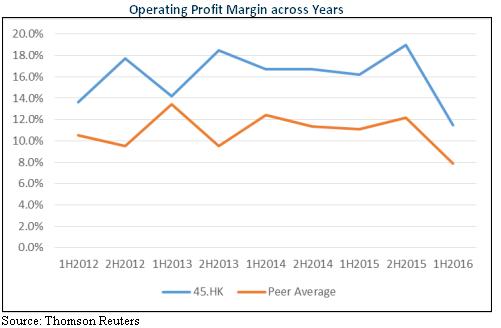

Comparing the company with its peers operating in the luxurious hotel segment, the company consistently achieves a higher operating profit margin than its peers do. However, the margin has contracted during 1H2016 because the Beijing and Chicago Peninsula Hotels were both under renovation but ordinary operating expenses such as personnel and utility expenses were incurred as usual, leading to a lower profit during the period. Such downturn is considered to be temporary and will recover in the future.

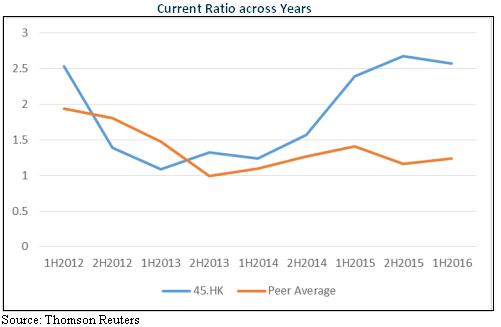

The company also has very strong liquidity, with its current ratio way above its peers. In particular, the entire cash balance in 1H2016 can be used to pay off all the current portion of the outstanding payable and the current ratio is more than two times of its peers in both 2H2015 and 1H2016.

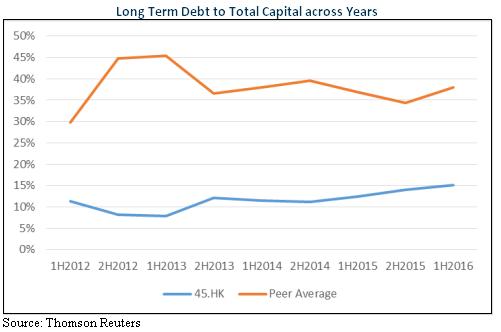

Besides, the company has very low leverage in comparison with the sector, allowing the company to face challenges in the tourism sector in a more prepared manner as well as employing capital into new development project quickly especially with its huge cash balance.

Valuation

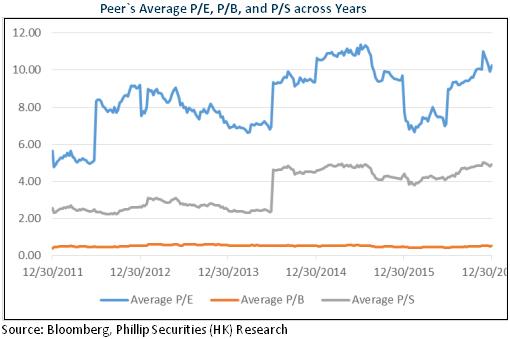

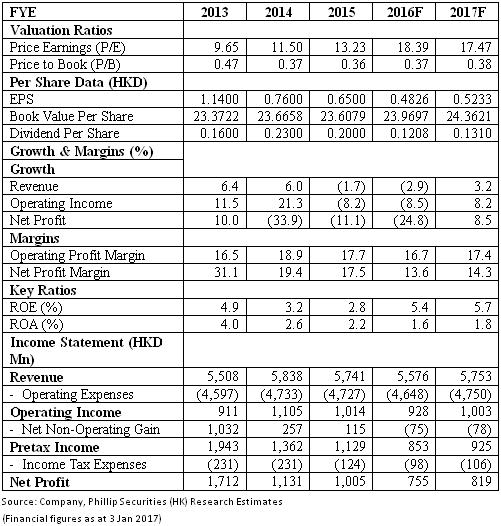

The peer average P/E, P/B and P/S are 8.41x, 0.52x and 3.55x respectively. The company's target price is therefore $9.70, with Accumulate rating assigned. (Closing price as at 3 Jan 2017)

Risk

Increased exposure in Europe and Middle East, which have high risk of terrorist attack

Delay in opening of new hotels

Rapid depreciation of Renminbi

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()