-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Fosun Pharma (2196.HK) - To Advance into Immune-Cell Therapy Market

Friday, January 20, 2017  26259

26259

Fosun Pharma(2196)

| Recommendation | Accumulate |

| Price on Recommendation Date | $25.150 |

| Target Price | $29.500 |

Weekly Special - 175 Geely

To Advance into Immune-Cell Therapy Market

Fosun Pharma intends to make an investment equivalent to no more than USD80 million in establishing a joint venture, Kite Biotechnology, with KITE, each of which owns a 50% share, with a view to developing the cancer T cell immunotherapy market in Mainland China, Hong Kong and Macau. Kite Biotechnology will acquire KITE's commercial rights for KTE-C19 in China, as well as the pre-option to license future products (namely KITE-439 and KITE-718).

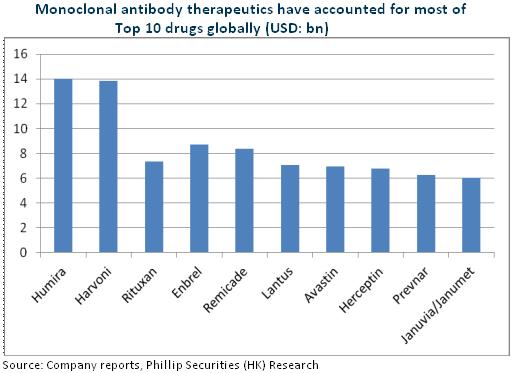

Tumor immunotherapy is the biggest breakthrough in cancer therapy in recent years, and Car-T is the most advanced technology in tumor immunotherapy. Currently, KITE, Novartis and Juno take the lead in international R&D, and KITE's KET-C19 is expected to be approved in 1H2017, making the world's first Car-T therapy product. Fosun Pharma, via domestic cooperation with KITE, will also be at the frontiers of the global immune-cell research. Moreover, KET-C19 indications cover around 160,000 patients, with a potential market size of RMB16 billion, and all three products have not satisfied clinical needs, with an estimated potential market size of more than RMB50 billion.

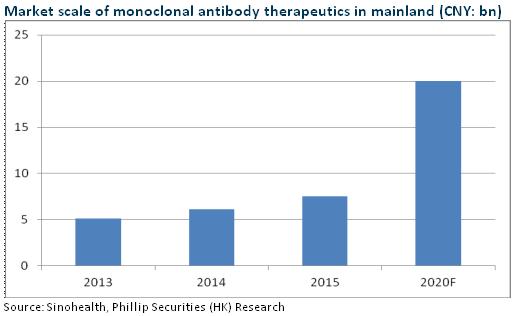

It is also worth mentioning that the company has secured the top 3 in domestic monoclonal antibody (McAb), and the two technological platforms, McAb and Car-T, are expected to create synergistic effects and help the company to become a benchmark in China's biological tumor treatment industry. At the same time, the company once again adopts JV model following the JV cooperation with Intuitive Surgical, proving its capability to cooperate with international top pharmaceutical companies. The model is likely to be duplicated in future expansion and support the company's international expansion.

McAb R&D Takes the Lead

At present, the rituximab and trastuzumab of Henlius are undergoing the Phase III clinical trial, and are expected to appear on the market in 2018 and 2020, respectively, and another three McAbs are in Phase I and one has obtained the clinical approval document. Rituximab US patent expires in 2018, which means the cost-effective domestic generic drugs are expected to quickly seize the lymphoma drug market, with an estimated penetration rate of 50% and a corresponding market size of approximately RMB2.3 billion. The company, following CPGJ in submitting the listing application, still takes the lead. Overall, since 2016, Henlius has significantly improved its R&D efficiency, coupled with well-established product lines and Fosun's strong sales capability, we expect Henlius to lead the domestic McAb field.

All-round Layout Supports Steady Growth

Fosun Pharma is also the second largest shareholder of Sinopharm Group, China's largest pharmaceutical distributor. It has, in the medical service sector, nearly 7,000 beds(including beds in construction and not been included in the consolidated financial statement), coupled with agent cooperation of such medical devices as Leonardo's robot, the company has made a layout throughout the whole industrial chain of medical and healthcare industry. We expect the company to maintain an annual growth of 20%+, since the biotech layout of McAb and Car-T is expected to rapidly lift its R&D level, the acquisition of Gland Pharma in India will promote its internationalization, and China's two-vote system reform and other reforms will also increase the market share of medical distribution and service business. We grant the company an estimation of 17.5x EPS in 2017 and a target price of HKD29.5, with the "Accumulate" rating. (Closing price as at 18 Jan 2017)

Risks

Drug price drop above expectation;

Acquisition and integration below expectations;

Geopolitical risks in the expansion of overseas business.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()