-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Shanghai Haohai Biological Technology (6826.HK) - Front-Runner in All Specific Sectors

Monday, June 6, 2016  9554

9554

Shanghai Haohai Biological Technology(6826)

| Recommendation | Buy |

| Price on Recommendation Date | $39.550 |

| Target Price | $48.180 |

Weekly Special - 175 Geely

Front-Runner in All Specific Sectors

Shanghai Haohai Biological Technology Co., Ltd. focuses on production and sales of absorbable biomedical materials, targeting at the four areas: orthopedics, medical aesthetics and wound care, ophthalmology, anti-adhesion and hemostasis, accounting for 43%, 18%, 11%, and 27% of the market share respectively in 2015.

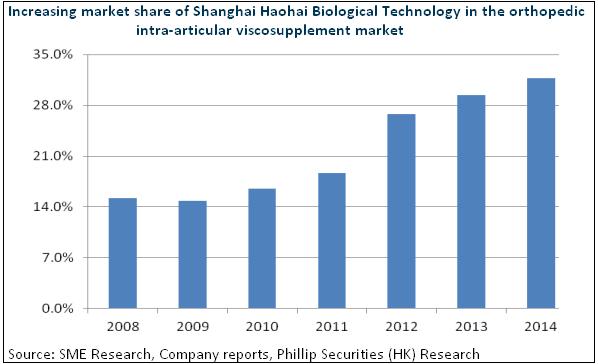

At present, its products in all specific sectors have formed high degree of market concentration, and achieved a leading position in the market. Specifically, based on the revenues in 2014, as reported by Southern Medicine Economic Research Institute, the company is China's largest producer of intra-articulat viscosupplement products, with a market share of 31.7%, and is China's second-largest producer of recombinant human epidermal growth factor (rhEGF), accounting for 15.3% of the market share. Meanwhile, the company is China's largest producer of OVD products and anti-adhesive products, accounting for, respectively, 41.8% and 48% of the market share.

With respect to the products of the company, medical chitosan for bone joint injection is the only protective agents in articular cartilage registered as class III medical devices in China, which is characterized by its unique water solubility, greatly reducing the probability of allergic reactions and improving product safety. Healin-branded rhEGF product is the first rhEGF product registered internationally, and was approved by the CFDA as a new class I drug in 2001.

Rapid Growth of Results

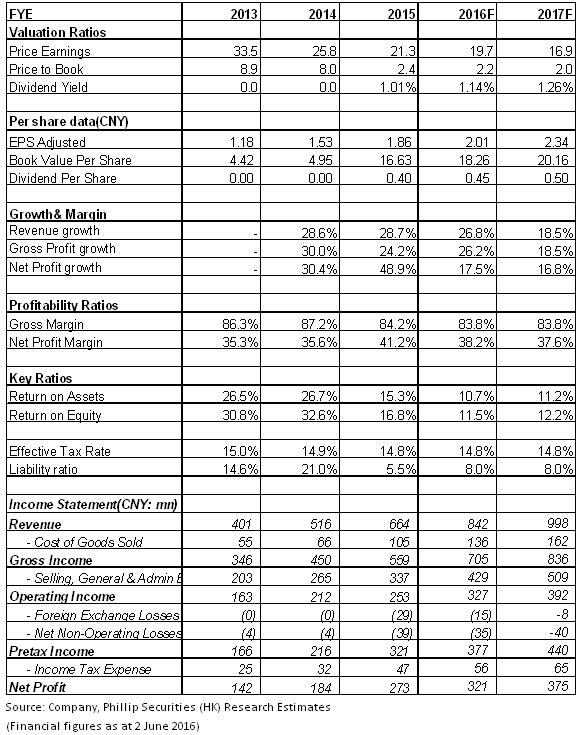

In 2015, despite the slowdown in the pharmaceutical industry, by virtue of competitive products and professional marketing network, the company achieved a revenue of RMB0.66 billion, a YoY growth of 29%. The net profit was RMB0.27 billion, an annual growth of 49%.

Specifically, although prices of sodium hyaluronate injection, the main orthopedic products, fell by 10%, its revenue still rose by 10% to RMB0.228 billion. In addition, market shares of newly launched chitosan for orthopedics use and plastic surgical products "Matrifill" rapidly expanded, revenues of which soared by 107% and 235% to RMB5600 million and RMB8700 million, respectively, becoming the main growth points.

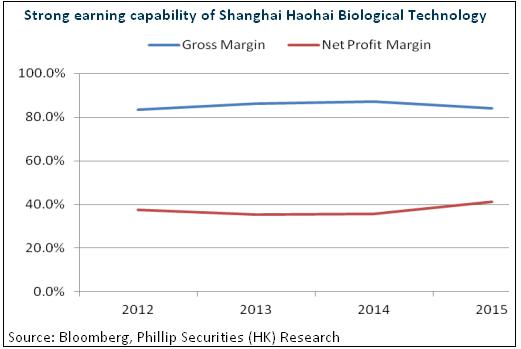

Although the completion of upgrading and industrialization reform caused increase in depreciation, and the company gross profit margin fell by 3% to 84.2%, IPO financing raised interest revenue by RMB3400 million and raised the gain from currency exchange by RMB2800 million, which eventually led to performance significantly outperforming the revenue growth.

Product Serialization Continues to Strengthen Competitive Advantages

Shanghai Haohai Biological Technology is taking various measures to strengthen its competitive advantages. Firstly, the company strengthens research and development (R&D), with R&D expense to revenue ratio increasing by 0.2% to 5.3% in 2015. Matrifill is the first CFDA-approved sodium hyaluronate gel for single-phase cross-linking injection. Its second generation of cross-linking sodium hyaluronate gel has gone through clinical trials, and its medical device registration application has been accepted. The third generation of QST gel has entered clinical trials. Therefore, the company's products will achieve a combined effect of serialization and differentiation, and are expected to maintain rapid growth.

Besides, considering the prospect of the market of medical aesthetics, the company established independent and professional marketing team for Matrifill products, combining direct selling with franchising. Meanwhile, the company also built professional marketing team for ophthalmology, anti-adhesion and hemostasis businesses. Marketing restructuring is expected to support the company in achieving better growth. Chitosan has been present on the health insurance directory in Beijing, Shanghai and other major cities, and its growth is expected to accelerate.

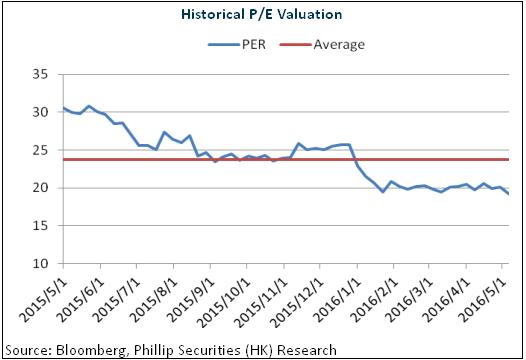

Overall, the company will maintain its competitive edge. Relying on the broad market of medical aesthetics and ophthalmology, the company is expected to maintain the rapid growth. We give an estimation of 20x EPS in 2016, and the target price is HKD48.18, with the "Buy" rating maintained. (Closing price as at 2 June 2016)

Risks

Drop in prices of sodium hyaluronate injection exceeds expectation;

Competition intensifies;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()