-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CMS (867.HK) - Innovative Development and Transformation Continues

Tuesday, January 21, 2020  6051

6051

CMS(867)

| Recommendation | Accumulate |

| Price on Recommendation Date | $12.040 |

| Target Price | $13.350 |

Weekly Special - 2333 Great Wall Motor

Project Update

The company recently issued announcements on the progress of various businesses: 1. On 13 January 2020, Neurelis announced that the U.S. FDA had approved its product VALTOCO (diazepam nasal spray) as an acute treatment of intermittent, stereotypic episodes of frequent seizure activity (i.e., seizure clusters, acute repetitive seizures) that are distinct from a patient's usual seizure pattern in people with epilepsy 6 years of age and older. Moreover, the company has been actively carrying out the regulatory application and other related work of VALTOCO in China since Neurelis submitted the NDA to the U.S. FDA, and has recently acquired the clinical trial notice of diazepam nasal spray from the National Medical Products Administration of China. The company is required to conduct a comparative pharmacokinetic study in Chinese subjects, and to submit a post-marketing study plan to further verify the efficacy and safety at the same time of submitting the NDA. 2. The company has signed a Collaboration Agreement on 5 December 2019 with Cambridge Judge Business School (CJBS) and AstraZeneca, and it will invest in the UK biotech and life sciences sectors over the next five years. Since 2015, AstraZeneca has played a role in mentoring biotech and life sciences researchers and innovators and has partnered with CJBS on various programs to promote enterprise and support entrepreneurship amongst life sciences researchers and students. Through the Collaboration Agreement, the company, AstraZeneca and CJBS demonstrate a common objective of strengthening the pipeline of opportunities in biotech and life sciences, more specifically in the areas of therapeutics, diagnostics, devices and digital health, thus providing the invested companies with greater access to international markets in particular Greater China. 3. The company signed a License Agreement with Sun Pharma Advanced Research Company Ltd. (SPARC) for five innovative products on 5 November 2019. The company gained an exclusive license with the right to grant sublicenses to develop and commercialize the products in Greater China. The initial term of the agreement shall be 20 years from the first commercial sale of the products in the Territory and may be extended for additional 3 years increments conditionally. The five innovative products are: (1) TaclantisTM/PICS, indicated for metastatic breast cancer (MBC), locally advanced or metastatic non- small cell lung cancer (NSCLC) and metastatic adenocarcinoma of the pancreas; (2) XelprosTM Ophthalmic Emulsion, indicated for reduction of elevated intraocular pressure (IOP) in patients with open-angle glaucoma, or ocular hypertension; (3) PDP-716 Eye Drops, proposed for the reduction of elevated IOP in patients with open-angle glaucoma or ocular hypertension; (4) SDN-037 Eye Drops, indicated for eye pain and inflammation after cataract surgery; (5) ElepsiaTM XR Tablet, indicated as adjunctive therapy for the treatment of partial onset seizures in patients 12 years of age and older. 4. The company signed a License and Supply Agreement with Biocon Limited for three generic products on 12 September 2019, and it gained an exclusive license to register and commercialize the products in Greater China. The initial term of the agreement shall be 10 years and may be extended for every fixed period of two years on a product-by-product basis conditionally.

Innovation Research Drives Development

At present, the company's long-term object is focusing on innovation research, actively investing in overseas R&D companies or reaching strategic cooperation with a view to establish an innovative product group with sufficient competitive advantages and market potential to meet China's unmet clinical needs. In the med-term, the company focuses on complex generic drugs and through strategic cooperation with leading overseas generic drug companies, it plans to deploy complex generic drugs with high generic barriers. In the short-term, the company focuses on the distribution of high-quality generic drugs that have been listed overseas, and establishes a generic drug product group that has sufficient market competitiveness, high quality and affordable costs. In addition, the company, as a traditional medicine marketing and promotion enterprise, currently covers more than 57,000 hospitals and medical institutions in its promotion network, covering all provincial administrative regions in China, and basically covering the main departments of tertiary hospitals and secondary hospitals.

Raise TP and Maintain "Accumulate" Rating

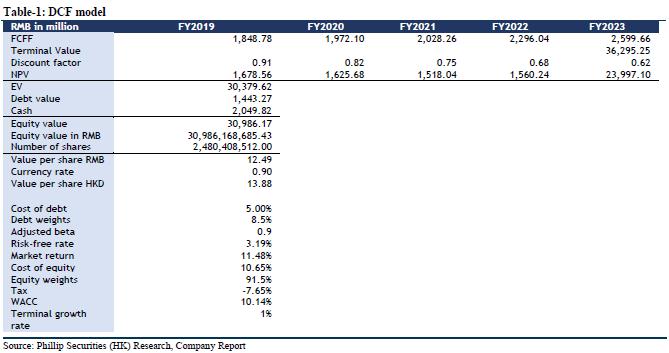

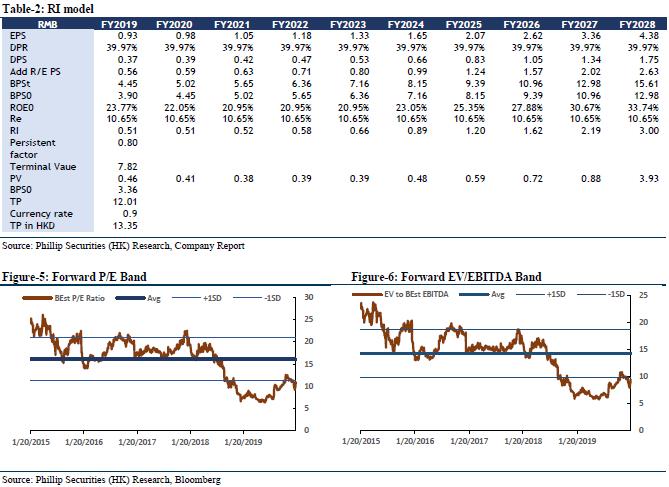

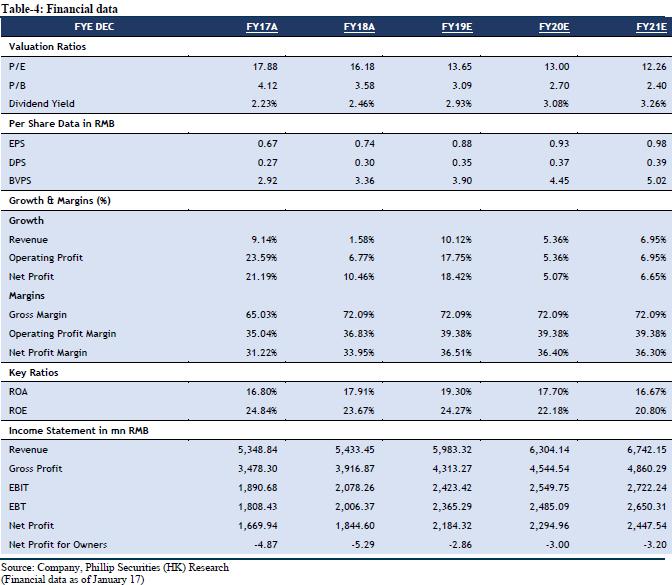

We maintain our forecast for company performance growth using DCF model and residual income model to value. Assuming equity cost is 10.65%, debt cost is 5%, and WACC is 10.14%. We get TP of HKD 13.88 and HKD 13.35 respectively. The higher valuation result corresponds to FY19/FY20/FY21 15.14x/14.41x/13.59x PE, which has an increase of +10.85% compared to the current price (HKD 12.04 as of January 17, 2020), maintaining an “Accumulate” rating.

Risk

The launch of new products fails expectations; Industry policy risk.

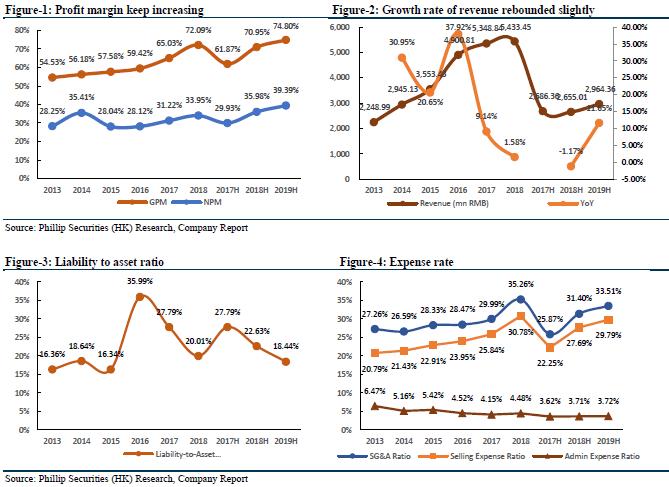

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()