-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Ming Yuan Cloud Group (909.HK) - Digitalization of the real estate ecological chain, SaaS business maintains rapid growth

Tuesday, October 12, 2021  12042

12042

Ming Yuan Cloud Group(909)

| Recommendation | Buy |

| Price on Recommendation Date | $27.200 |

| Target Price | $42.400 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

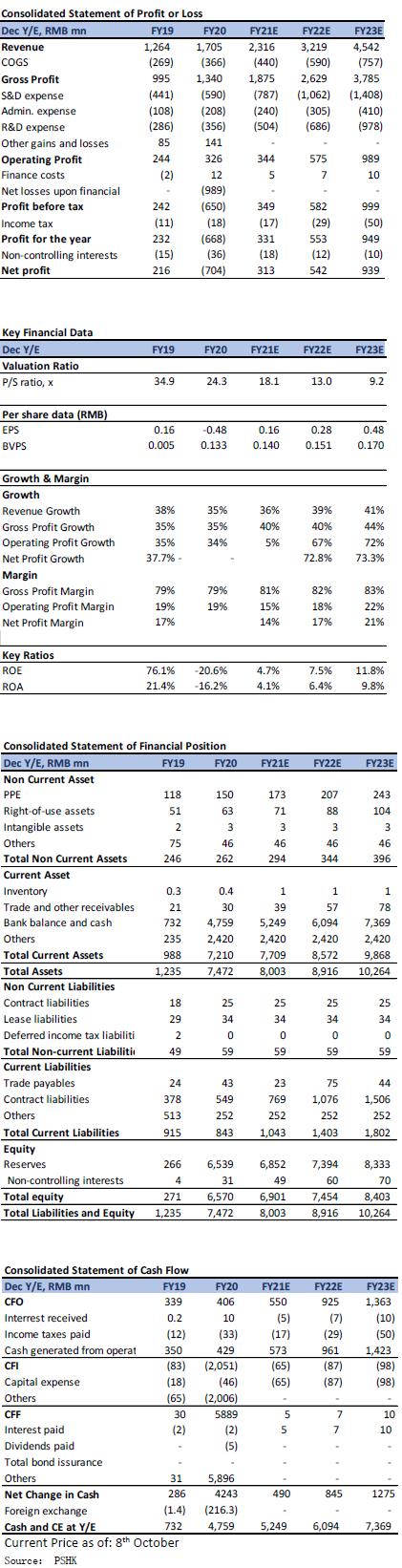

Ming Yuan Cloud announced the company's interim results as of June 30, 2021, benefiting from the steady development of real estate industry in the first half of the year and the rapid growth of the company's SaaS product revenue, the company's revenue reached RMB 970 million (+45% yoy) and its adjusted net profit reached RMB 193.5 million (+32.7% yoy). Among them, SaaS product revenue reached RMB 550 million (+66% yoy), accounting for about 57% of total revenue. The revenue of ERP solutions was RMB 420 million (+25% yoy), accounting for about 43% of total revenue.

CRM Cloud ARPU still has room to increase, Construction Cloud becomes the second largest growth engine

In 1H21, CRM Cloud's revenue reached RMB 430 million (+82% yoy), accounting for 78% of the total revenue of the SaaS business. In 1H21, CRM Cloud's achieved rapid growth in Average Revenue Per User (ARPU) while maintaining a high market penetration rate. The number of property sales offices in China equipped with CRM Cloud 16,200 (+8% yoy), while the ARPU increased from approximately RMB 19,000 to RMB 26,000 (+37% yoy). In the past, CRM Cloud mainly focused on solving the management and process problems of real estate marketing. Since last year, it has developed in the direction of business integration and gradually transitioned to helping developers improve their marketing capabilities. Affected by the government policy and supervision on real estate industry, in addition to reducing expenditure, acquiring customers is a major challenge for real estate industry in the future. Therefore, it is expected that CRM Cloud's will still have a room to increase as helping developers build private traffic. It is expected that with the gradual slowdown of penetration rate growth in the future, there are still room for increase in ARPU which can provide momentum for CRM Cloud's revenue growth.

In 1H21, Construction Cloud's revenue was RMB 79 million (+14% yoy), accounting for 14% of the total revenue of the SaaS business. In 1H21, the number of Construction Cloud's serving construction sites in China was approximately 6,000 (+ 46% yoy). At present, the real estate supply chain industry is still more traditional, with generally low efficiency and information asymmetries, including weak digital empowerment. Therefore, the Construction Cloud focus on the quality of supply and creates entire chain application scenario. It is expected that the Construction chain will break the industry in the next 1-2 years and become a major engine of the company's revenue growth.

In terms of Procurement Cloud, in 1H21, its revenue was RMB 20 million (+ 77% yoy), accounting for 4% if the total revenue of the SaaS business. There were approximately 3,100 property developers and 83,000 suppliers with access to Procurement Cloud respectively. The Existing Market's revenue in 1H21 was RMB 22 million (+ 25% yoy), accounting for 4% of the total revenue of the SaaS business. It is composed of Asset Management Cloud, Property Management Cloud and Commercial Management Cloud. Among them, the total area under management of Asset Management Cloud and Property Management Cloud increased by 113.5% and reached approximately 190 million square meters. Besides, the Company completed its investment in Shenzhen Woxiang Technology Co., Ltd. and the number of Commercial Management Cloud's serving shopping malls increased by 56% to 114.

ERP Solution maintain steady growth

In 1H21, the ERP Solutions revenue reached RMB 421.9 million (+25% yoy). Among it, software licensing and value-added services revenue accounted for 33% and 36% of the total revenue, reaching RMB 140 million and 150 million (+ 38% and 18% yoy). The company further strengthened the development of industry-leading enterprises and sinking markets, as well as enhanced product support service capabilities, strengthened centralized management and provided more value-added service products. Therefore, it is expected that the ERP solutions` revenue will increase steadily.

Company valuation

We maintain our forecasts for the company's revenue and net profit for 2021/ 2022/ 2023, and use the sum of the parts (SOTP) valuation to evaluate the company's two businesses separately. Taking into account the recent SaaS sector valuation callback, we lower the target price-earnings ratio (P/E) for the ERP solution to 20x in 2022 and the target price-sales ratio (P/S) in 2022. The target price given is HKD 42.40, corresponds to a P/S of 30.6x/ 22.0x/ 15.6x, corresponding to 2021/ 2022/ 2023 and the “BUY” rating is maintained.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()