-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Mobile (941.HK) - Solid Growth Maintained, Digital Transformation Unlocks Further Value

Tuesday, May 20, 2025  16593

16593

China Mobile(941)

| Recommendation | Neutral |

| Price on Recommendation Date | $85.800 |

| Target Price | $81.660 |

Weekly Special - 2333 Great Wall Motor

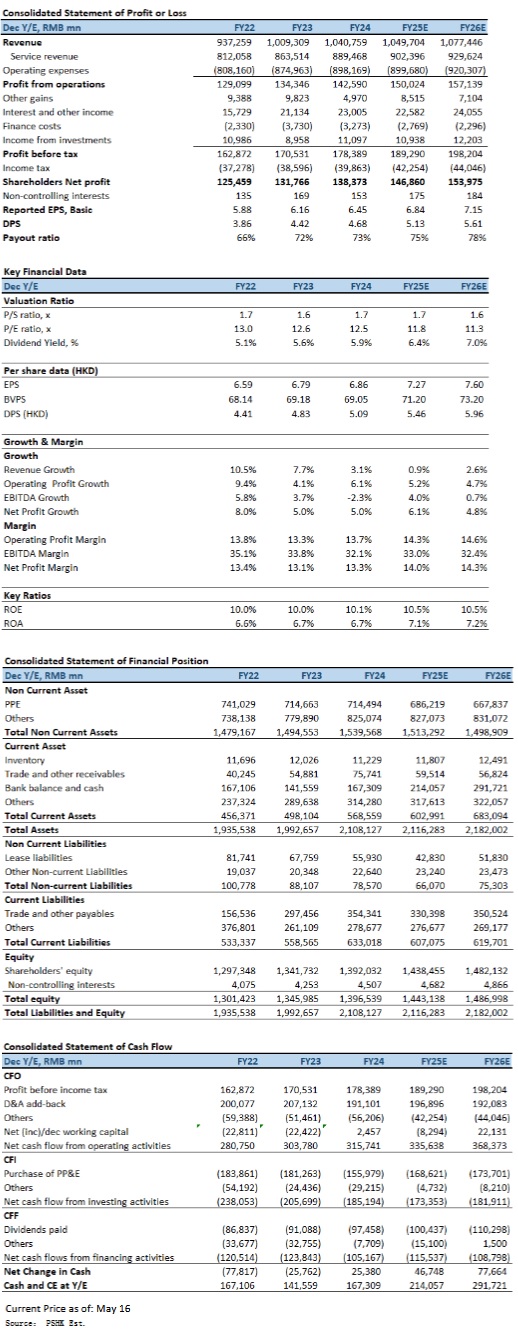

China Mobile (941 HK) announced its FY2024 full-year results on March 20, 2025, and its 1Q2025 results on April 22, 2025. Overall, the company delivered stable and improving performance, with sustained profitability and continued momentum in its digital transformation strategy. Key growth drivers include expanding DICT and cloud services, along with AI-led innovation.

Revenue and Profitability: Core Services Remain Resilient, Digital Business Accelerates

In FY2024, China Mobile recorded operating revenue of RMB 1,040.8 billion, up 3.1% YoY. telecommunications services revenue grew 3.0% YoY to RMB 889.5 billion, maintaining a stable contribution ratio of over 85%. Notably, digital transformation revenue reached RMB 278.8 billion, a YoY increase of 9.9%, accounting for 31.3% of communication service revenue—up from 29.4% in 2023—highlighting the growing importance of emerging businesses.

In 1Q2025, the company reported operating revenue of RMB 263.8 billion, virtually flat YoY (+0.02%). Telecommunications services revenue amounted to RMB 222.4 billion, rising 1.4% YoY. While overall revenue growth moderated, the core business remained resilient, supported by targeted value management and customer segmentation strategies.

Profit Expansion: Operating Efficiency and Depreciation Policy Drive Margin Gains

Full-year 2024 net profit attributable to shareholders rose 5.0% YoY to RMB 138.4 billion. Basic EPS was RMB 6.45. EBITDA reached RMB 333.7 billion, with an EBITDA margin of 37.5% on communication service revenue. A key factor behind the margin improvement was the change in depreciation policy—beginning in 2024, the depreciation period for 5G wireless and transmission equipment was extended from 7 to 10 years. This adjustment reduced annual depreciation and amortization by around RMB 19.07 billion, releasing pressure on operating margins.

In 1Q2025, EBITDA stood at RMB 80.7 billion, up 3.4% YoY, with an EBITDA margin of 30.6%, compared to 29.6% in the same period last year. Net profit attributable to shareholders was RMB 30.6 billion, up 3.45% YoY. The profit growth was mainly due to improved operating efficiency and stable contribution from non-recurring income.

A full-year dividend of HK$5.09 per share for 2024, representing a 5.4% YoY increase and a payout ratio of 73%. China Mobile reiterated its commitment to raise the cash dividend payout to over 75% of net profit within three years starting 2024, underscoring strong confidence in future earnings and cash flow.

In the “Customer” market, total mobile subscribers reached 1,004 million by end-2024, with 5G network customers rising to 552 million, representing a 55% penetration rate. Mobile ARPU remained industry-leading at RMB 48.5. The company's value-added services saw robust growth—Personal China Mobile Cloud Drive revenue reached RMB 8.9 billion (+12.6% YoY), while revenue from integrated-benefit products generated RMB 26.8 billion (+19.7% YoY). Monthly active users of 5G New Calling across all platforms reached 150 million, with 34.75 million smart application subscribers.

In the home market, broadband customers totaled 315 million, with 278 million being household users. ARPU for household customers increased 1.6% YoY to RMB 43.8. Gigabit broadband users grew 25% YoY, and FTTR users surged by 376% YoY, reflecting strong demand for premium broadband and smart home upgrades.

The "Business" Market saw strong expansion driven by “AI+DICT” integrated solutions. Revenue grew 8.8% YoY to RMB 209.1 billion. Corporate customers reached 32.6 million (+4.2 million net adds). China Mobile Cloud revenue exceeded RMB 100.4 billion (+20.4% YoY), maintaining its top-five industry position in IaaS+PaaS. The company completed over 700 large-scale 5G DICT projects and grew 5G dedicated network revenue by 61% YoY to RMB 8.7 billion.

In "New" Markets, revenue rose 8.7% YoY to RMB 53.6 billion. International business contributed RMB 22.8 billion (+10.2% YoY), digital content reached RMB 30.3 billion (+8.2% YoY), and fintech revenue soared to RMB 116.5 billion (+52%). Notably, MIGU Video monthly active users exceeded 520 million, and and-Wallet monthly actives reached 124 million.

Innovation and Infrastructure: AI+ and BASIC6 Strategy Gathers Momentum

China Mobile accelerated the rollout of its “Three Major Programs” of “Two New Elements”. The “AI+” initiative saw meaningful progress, with the debut of the company's proprietary Jiutian large language model, which was included in the 2024 list of “Top 10 National Strategic Tools” by central SOEs. The AI+DICT integrated service model signed over 500 projects and reached 190 million users for AI-based products.

On the infrastructure side, total general-purpose computing power reached 8.5 EFLOPS, with intelligent computing at 29.2 EFLOPS, with the intelligent computility center nodes commencing operation in regions including Beijing-Tianjin-Hebei. The 400G backbone and AIDC upgrades were recognized as industry benchmarks.

Investment Thesis

China Mobile's FY2024 and 1Q2025 results demonstrate stable revenue and profit growth, underpinned by resilient core businesses and accelerating contributions from digital transformation, and innovative businesses such as AI and DICT are expected to become core growth engines in the future. The depreciation policy change provided a short-term margin boost, while the company's commitment to strong and growing dividends reinforces its focus on shareholder value. Looking ahead, China Mobile is well-positioned to benefit from the “AI+” era. The company's leadership in computing infrastructure, cloud, and intelligent applications offers strong potential for value creation. We expect FY2025E-FY2026E EPS to be RMB 6.84 and RMB 7.15 respectively, with PT of HK$81.66, implies a FY2025E P/E of 11.2x (~0.5-yrs historical average plus 1 standard deviation). Our investment rating is “Neutral”.

Risk factors

1) The weak economic recovery affects user ARPU and government and enterprise demand; 2) The industry competition landscape worsens; 3) Policy or data compliance risks.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()