-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Hua Hong Semiconductor (1347.HK) - Leading manufacturer of semiconductors on 8-inch wafers

Friday, July 10, 2015  18899

18899

Hua Hong Semiconductor(1347)

| Recommendation | Buy |

| Price on Recommendation Date | $7.670 |

| Target Price | $11.580 |

Weekly Special - 002050 Sanhua

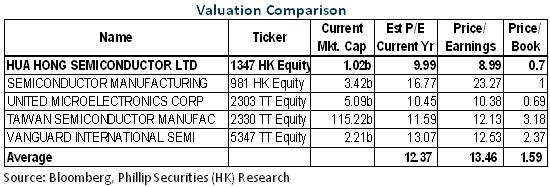

Hua Hong Semiconductor Limited is a pure-play wafer foundry. Based on the revenue in 2014, it ranked the ninth largest semiconductor foundry worldwide, with a market share of 1.4%. Meanwhile, the Company ranked the second among semiconductor foundries in China, right after Semiconductor Manufacturing International Corporation which has a market share of 4.2%. It is worth to note that the Company specializes on manufacturing of semiconductors on 8-inches wafers for specialty applications and it ranks the second among the manufacturers of such wafers worldwide.

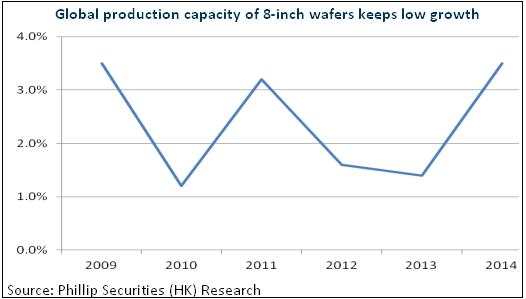

Currently, the global production capacity of 8-inch wafers is relatively tight. According to the information provided by Gartner, the annual growth of global production capacity of 8-inch wafer foundries merely increased 2.5% annually from 2008 to 2014. In 2015, even though companies including United Microelectronics Corporation, Semiconductor Manufacturing International Corporation, Vanguard International Semiconductor Corporation and Hua Hong announced to expand the production capacity of 8-inch wafers, the increased capacity can only account for 3% of the 2015 annual global capacity based on statistics. Overall speaking, the market demand and supply of 8-inch wafers has demonstrated significant improvement. We think the demand and supply situation in the industry would still be tight, while the Company's profitability could keep on a high level.

In the context of economic restructuring, China has pinpointed “localization of the production of wafers” and “Made in China 2025” as the long term development strategies. Internet of things (IoT), wearable devices and automotive electronics etc will bring long term stable demand to Chinese suppliers. Hua Hong's major market is in Mainland China with revenue contribution over 50% (2015Q1 recorded 56.5%). We believe the Company would be benefitted from the boost of demand for semiconductors in China market. Moreover, Hua Hong still enjoys the support from preferential policies, huge amount of grants and subsidies would still be one of the main profit sources.

Positive prospect on profit

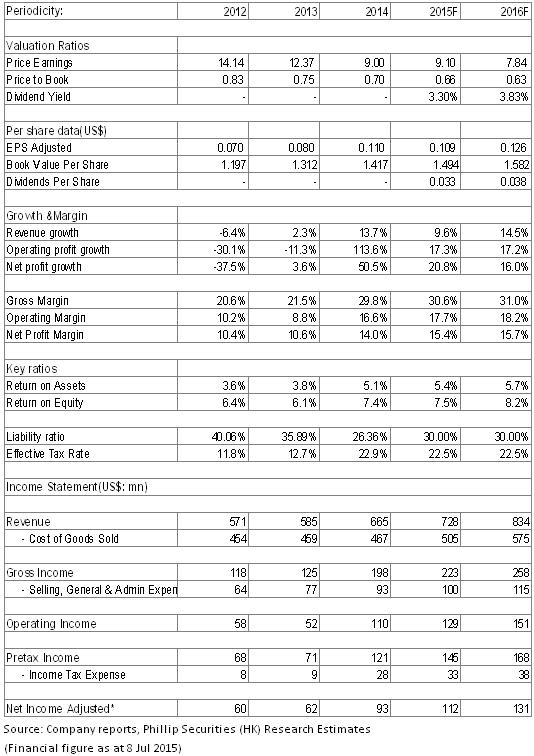

Even though Hua Hong specializes on the production of 8-inch wafers which are comparatively backward, the Company enjoys a leading position in this field. Moreover, the segment of 8-inch wafer production brings solid and steady growth to the Company. Market demand is improving, particularly the Chinese domestic market. Localization of the production of wafers also supports the release of demand. We expect the Company would still maintain high level of utility rate on capacity, as well as profitability. We give the Company a valuation level corresponding to 1x of book value per share in 2015. Target price is set as HK$11.58, with the “Buy” rating initially. (Closing price as at 8 July 2015)

Leading manufacturer of semiconductors on 8-inch wafers

Hua Hong Semiconductor Limited is a pure-play wafer foundry. Based on the Company's revenue in 2014, Hua Hong ranked the ninth largest semiconductor foundry worldwide, with a market share of 1.4%. Meanwhile, the Company ranked the second among semiconductor foundries in China, right after Semiconductor Manufacturing International Corporation which has a market share of 4.2%. It is worth to note that the Company specializes on manufacturing of semiconductors on 8-inches wafers for specialty applications and it ranks the second among the manufacturers of such wafers worldwide. 8-inches wafers are mainly applied on smart cards, MUC, automotive, smart grids, LED lightings, wearable devices and inter-connected sensors. The Company currently provides process technology platform which incorporates technical applications from 1.0μm to 90nm.

The Company is the leading manufacturer of embedded nonvolatile memory device and also the only wafer foundry which applies ESF2 SuperFlash process technology onto commercial production. Such memory device can bear a wider range of temperature and have advantages of high level of persistence and data retention ability.

Moreover, the Company has leading position in SIM card segment, with a market share exceeding 50%. Smart cards are adopted on identity cards, health insurance cards, as well as credit cards and debit cards issued by banks. The Company is the largest foundry of Chinese identity cards, and it is expected to be the major foundry of the next generation of social security cards. Currently, among the six authorized providers of smart cards in China, five companies provide outsourcing to Hua Hong, including Tongfang Microelectronics, Fudan Microelectronics, CEC Huada Electronic, Nationz Technologies and Hua Hong IC.

Situation of market demand and supply improved, profitability keeps robust

Currently, the global production capacity of 8-inch wafers is relatively tight. According to the information provided by Gartner, the annual growth of global production capacity of 8-inch wafer foundries merely increased 2.5% annually from 2008 to 2014. Among such capacity worldwide, Taiwan and Mainland China accounted for 47% and 18% respectively. In 2015, even though companies including United Microelectronics Corporation, Semiconductor Manufacturing International Corporation, Vanguard International Semiconductor Corporation and Hua Hong announced to expand the production capacity of 8-inch wafers, the increased capacity can only account for 3% of the 2015 annual global capacity based on statistics.

From the demand side, the market sale of 8-inch wafer foundries improved in the past few years. It is mainly benefitted from the IC demand from smart phones/4K2K and the upgrading of wafers from the 6 inches to 8 inches installed in analog/power management IC etc. In addition, the number of applications which do not need advanced 12-inch process has increased, mainly cover MCU and smart cards (can be manufactured by existing technology).

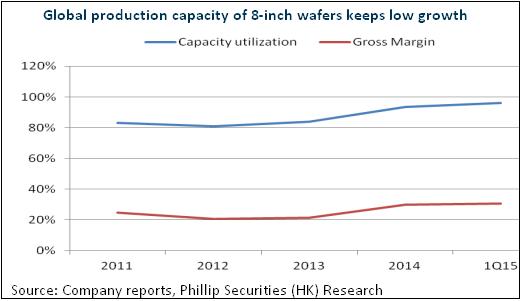

Therefore, the market demand and supply of 8-inch wafers has demonstrated significant improvement. The utility rate of capacity of Hua Hong was also raised significantly to 93.5% in 2014 and 96.1% in 2015Q1 from the previous figures of about 80%. It in turn boosted the profitability of the Company. For example, the gross profit margin increased to higher than 30% from the previous figures of about 20%. We think the demand and supply situation in the industry would still be tight, while the Company's profitability could keep on a high level.

Continual launch of supportive policies

In 2014, the overall self-sufficiency rate of the semiconductor manufacturing industry in China only amounted to 37%, which is far too low to satisfy the overall domestic demand in China, and it brought a vast need of importing substitutes. Especially in the context of economic restructuring, China has pinpointed “localization of the production of wafers” and “Made in China 2025” as the long term development strategies. Internet of things (IoT), wearable devices and automotive electronics etc will bring long term stable demand to Chinese suppliers. Hua Hong's major market is in Mainland China with revenue contribution over 50% (2015Q1 recorded 56.5%). We believe the Company would be benefitted from the boost of demand for semiconductors in China market.

Moreover, Hua Hong still enjoys the support from preferential policies. The Company has received a sum of grants and subsidies of more than USD0.11 billion in past few years, accounted for about 45% of the pretax profit. We consider the semiconductor manufacturing industry as a capital and technological intensive industry and it needs support from government policies in particular. With the strong support from the central and regional authorities on developmental strategies of semiconductor industry and the great effort spent on building up the IC industrial investment fund, huge amount of grants and subsidies would still be one of the main profit sources of the Company.

Catalyst

Consistent preferential policies;

Higher-than-expected demand on imported substitutes.

Risk Factor

Lower utility rate of capacity;

Unsatisfactory progress on new technological innovation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()