-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Amazon (AMZN) - Year-on-year revenue growth in 2Q24 increased, 2025 capital expenditure exceeds expectations

Wednesday, March 5, 2025  3887

3887

Amazon

| Recommendation | Accumulate |

| Price on Recommendation Date | $214.000 |

| Target Price | $238.000 |

Weekly Special - 2333 Great Wall Motor

Company profile

Amazon was founded in 1995 and is an American multinational technology company engaged in providing online retail shopping services. It operates through the following segments: North America, International, and Amazon Web Services (AWS). The North America segment involves the retail sale of consumer products, including sales from sellers and subscriptions through online and physical stores focused on North America. It also includes export sales from online stores. The International segment focuses on consumer product retail revenue, including revenue from sellers and subscriptions through international online stores. The AWS segment includes the global sales of computing, storage, databases, and other services for startups, enterprises, government agencies, and academic institutions.

4Q24 revenue grew year-over-year, but Q1 guidance fell short of expectations

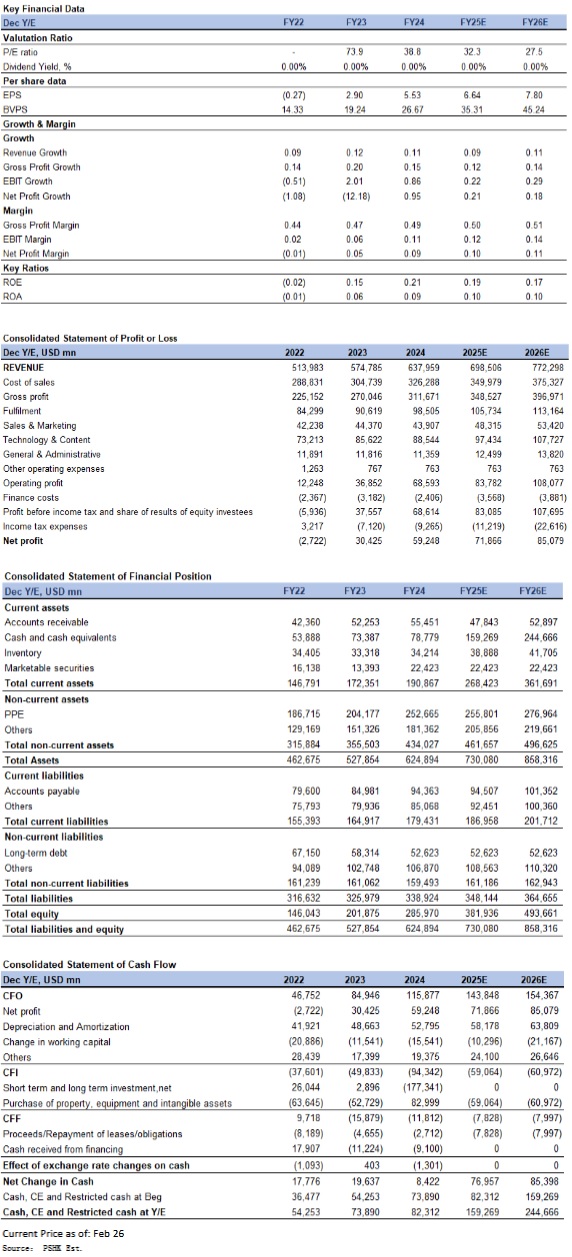

In the fourth quarter of 2024, the company achieved net revenue of $187.8 billion, representing a 10.0% YoY growth. Operating profit rose to $21.2 billion (up 61.0% YoY), while net profit surged 88.0% YoY to $20.0 billion. By business segment, online stores generated $75.6 billion in net revenue (up 7.1% YoY), physical stores $5.6 billion (up 8.3% YoY), third-party retail $47.5 billion (up 9.0% YoY), advertising $17.3 billion (up 18.0% YoY), subscription services $11.5 billion (up 9.7% YoY), and AWS $28.8 billion (up 19.0% YoY). Regionally, international markets contributed $43.4 billion in net revenue (up 7.9% YoY), while North America accounted for $115.6 billion (up 9.5% YoY), with global paid units increasing 11.0% YoY due to competitive pricing, wide product selection, and fast shipping. Logistics efficiency improved significantly in Q4 due to better inventory management, increased units per package, and shorter shipping distances. Looking ahead to Q1 2025, the company forecasts net revenue between $151.0 billion and $155.5 billion and operating profit between $14.0 billion and $18.0 billion, both falling short of expectations due to unfavorable exchange rate fluctuations. Management also indicated that Q4's capital expenditure of $26.3 billion would be representative of 2025, with total capital expenditures projected to reach $105.0 billion for the year.

Retail Business: low-price strategy continues to drive gains

The company's online retail business remains focused on its low-price strategy, maintaining the lowest online prices for the eighth consecutive year, averaging 14% lower than other major U.S. retailers. Regionalization has improved cost management and delivery efficiency, with same-day delivery site volumes growing by more than 60.0% year-over-year. As a result, the operating profit margin for the online retail business increased by 1.9% YoY, reaching 8.0% in Q4 2024. The company operates over 750,000 robots in its retail network and highlighted that innovations in AI and robotics helped reduce fulfillment center service costs by 25.0% during the holiday season. Currently, the company is leveraging generative AI to create new shopping experiences, including Rufus (a generative AI shopping assistant), enhancements/reconstruction of Alexa, Amazon Lens (which allows users to upload images to find products), enhancements to Prime Video, and Fit Review Highlights.

Advertising Business: achieving high double-digit growth

The company employs a full-funnel advertising approach, offering differentiated audience targeting capabilities by leveraging billions of customer signals from both its stores and media platforms. This enables precise audience targeting for advertisers. Advertising revenue has achieved high double-digit growth, driven by improved relevance in international regions and the U.S. market (excluding foreign exchange impacts). This growth is attributed to the continued expansion of sponsored listing ads and above-industry-average GMV growth during the holiday season.

AWS: 2025 capital expenditure exceeds expectations

In the fourth quarter of 2024, AWS reported an operating profit of $10.6 billion, a year-on-year increase of 48.3%, with an operating profit margin of 36.9%, up significantly from 30.0% in the same period last year. This improvement was primarily due to efficiency gains from software and infrastructure innovations, as well as ongoing cost control efforts. Management expects AWS operating profit margins to fluctuate with capital investments but anticipates that 2025 capital expenditure will remain stable compared to the fourth quarter of 2024. As a result, we expect minimal fluctuations in AWS operating profit margins in 2025. Amazon Bedrock continues to iterate rapidly, adding over 100 new and popular models. Additionally, the company's management announced the launch of its own cutting-edge model family, Nova, which integrates key Bedrock features while offering high efficiency and low cost. The company has now established a competitive advantage across the entire AI industry chain, with a comprehensive layout spanning cloud infrastructure, model ecosystems, computing power, and application scenarios. This positions AWS to meet diverse customer needs and is expected to drive new growth opportunities for the business.

Investment thesis

Given Amazon's strong position in both e-commerce and public cloud sectors, which are still in the early stages of long-term transformation, the company is well-positioned for future growth. Amazon has provided a significant competitive advantage to its retail business by enhancing the flexibility of its first-party and third-party inventory. Additionally, its first-mover advantage in cloud computing has enabled AWS to capture over 30% of the global market share. As a result, we forecast the company's operating revenue for 2025-2027 to be $698.5 billion, $772.3 billion, and $850.6 billion, respectively, with net profits of $71.9 billion, $85.1 billion, and $106.4 billion. This translates to EPS of $6.64, $7.80, and $9.66, respectively. The current stock price corresponds to a PE ratio of 32.3x, 27.5x, and 22.2x for the respective years.

Based on the DCF valuation method, we apply a 15x EV/EBITDA multiple for 2030 and assume a 10% discount rate, estimating the company's total target market capitalization at $2.58 trillion for 2025. This corresponds to a target price of $238, with a "Accumulate" rating.

Risk factors

1) Slower-than-expected progress in AI; 2) Intensified competition in the e-commerce industries; 3) Reduction in global cloud computing spending.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()