-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Travelsky Technology (696.HK) - United States trade war resumed, Airline industry will suffer in the short term

Friday, May 24, 2019  12933

12933

Travelsky Technology(696)

| Recommendation | Buy |

| Price on Recommendation Date | $16.620 |

| Target Price | $23.740 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

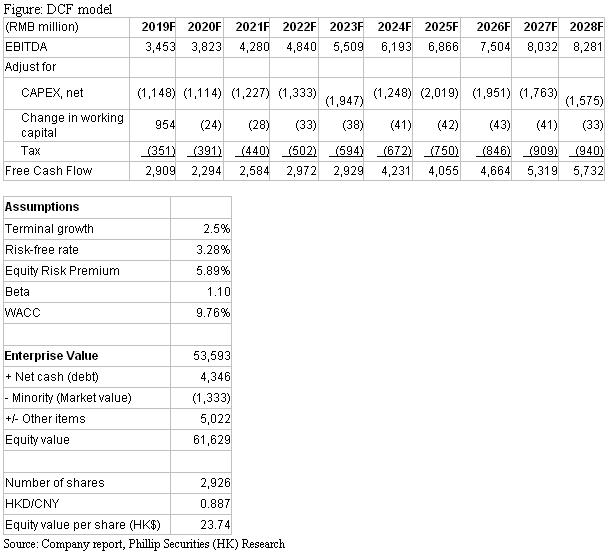

Travelsky Technology is the largest provider of the aviation information systems in China, which developed systems, such as flight control, air ticket distribution, check-in, boarding and load planning, accounting, settlement and clearing system, and aviation logistic. Based on DCF valuation, we derived a TP of HK$23.74, implied a P/E of 24.5x and 22x in 2019/20F. We maintain a “Buy” rating with a potential upside of 42.8%. (Closing price at 20 May 2019)

The pessimistic outlook on economy and depreciation on RMB reduce the number of tourists and freight transport volume in China in the short term

As the China - United States trade war resumed, the number of tourists and freight transport volume in China may reduce due to the pessimistic outlook on economy and depreciation on RMB. The China - United States trade war was reignited, after the US urged to raise the tax rate from 10% to 25% for goods from China worth USD 200 bn on 6 May and officially came into effect on 10 May. China also retaliated by imposing a tax rise on goods from US worth USD 60bn. If the intensity of conflict between US and China remains or goes up, it will definitely drive down their economic growth, or even the global economic growth. Besides, the depreciation on RMB could somehow alleviate the effect of tax rise from US side, which could maintain the competitiveness of the Chinese export. The RMB has depreciated by 2.7% in since May, reaching the previous bottom in 2017.

As the pessimistic outlook on economy and depreciation on RMB, the willingness to travel for Chinese may reduce. First, traveling is attributed to the discretionary spending, implying that it is vulnerable to the economic cycle. If the economy is heading into a recession, the number of travelling may reduce. Second, the depreciation on RMB lowers the purchasing power of Chinese travelers in foreign countries, which may eventually reduce their willingness to travel.

If the number of tourists drops, it would reduce the bookings through the Group's systems, thereby lowering the revenue of Group. The recession may also reduce the freight transport volume, which will affect the revenue from Accounting, Settlement and Cleaning Services.

However, we believe the number of traveling will remain its uptrend in the long term despite the shocks in the short term , thanks to the increase in GDP per capita. Once the monopoly due to the protection from the Civil Aviation Administration remains, the Group will be the only company that benefits from this uptrend in number of travelling.

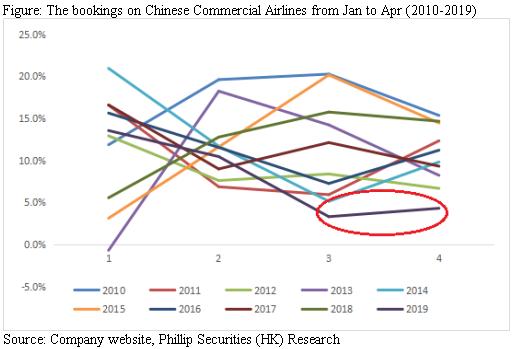

At present, some of the impacts can be seen from the operational data released by the group. Although the number of bookings for Chinese commercial airlines increased by 7.74% YoY from January to April, and the number of foreign and regional commercial airlines` bookings increased by 8.95% YoY. However, the growth rate of bookings for Chinese commercial airlines in March and April were the lowest in nine years, only 3.3% and 4.3%. The trade war was reignited in May, so the operating data for the next few months may remain low.

Spring Airlines adopted Travelsky's computer reservation system (CRS)

The Group released on May 15 that Spring Airlines has adopted their computer reservation system (CRS) - eTerm, implying that the travel agents will be able to purchase the air ticket of Spring Airlines via the Group's CRS.

Previously, Spring Airlines mainly sold their ticket through their own website. However, as its size became larger and the increase in international flights, direct sales will not be able to cope with the volume. As a result, Spring Airlines decided to adopt the Group's CRS.

Although Spring Airlines did not adopt the Group's Inventory Control System (ICS), the system we believe creates the greatest competitive advantage, the cooperation still could enhance the competitiveness of the Group's Global Distribution System (GDS).

Earnings Forecast

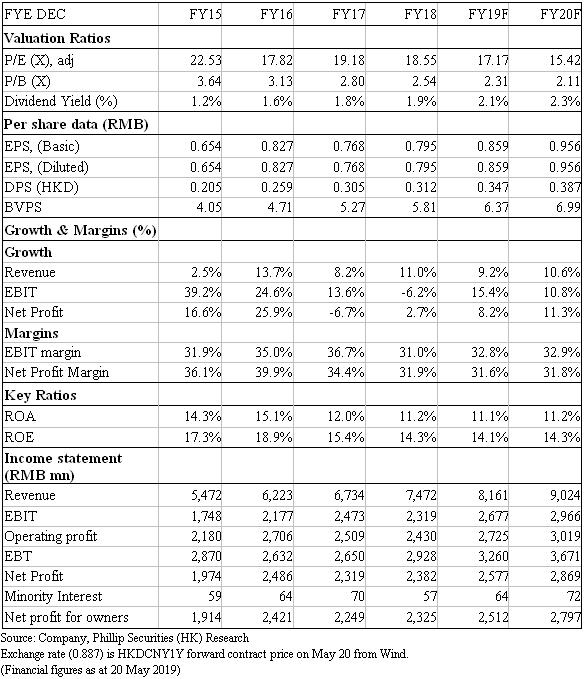

We lower our revenue growth forecast in 2019/20F by 1.1%/0.46%, to 9.2%/10.6%, reflecting the pessimistic outlook on Chinese economy and depreciation on RMB, but we should see the growth resume to normal in the long term.

Valuation

We adopted the DCF model for valuation, where we assume the discount rate to be 9.76%, and terminal growth to be 2.5%, with FCFF forecast to 2028F. We derived a TP of HK$23.75, implied a P/E of 24.5x and 22x in 2019/20F, 6.8% lower than our previous TP, due to the pessimistic outlook on Chinese economy and depreciation on RMB. We believe the investment ground in the long term still remains, but may suffer in the short term due to the intensified trade war. In view of the plunge in stock price, we maintain a “Buy” rating with a potential upside of 42.8%. (HKD/CNY=0.887)

Risk

1. Economic downturn

2. Aviation system market opening up

3. Airlines develop their own systems

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()