-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

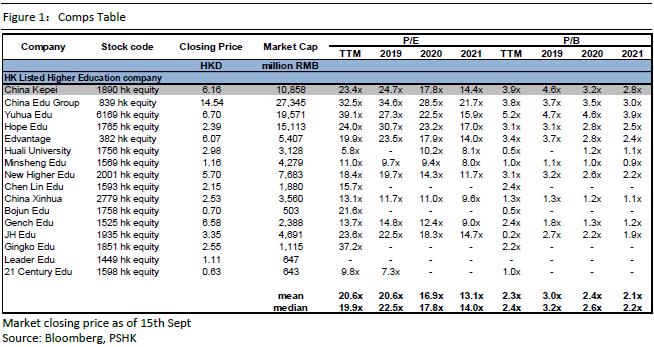

China Kepei (1890.HK) - Margin Higher than Expected, Huge Increase in 20/21 Student Enrollment

Friday, September 18, 2020  17926

17926

China Kepei(1890)

| Recommendation | Buy |

| Price on Recommendation Date | $6.160 |

| Target Price | $7.670 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

1H20 interim result overview

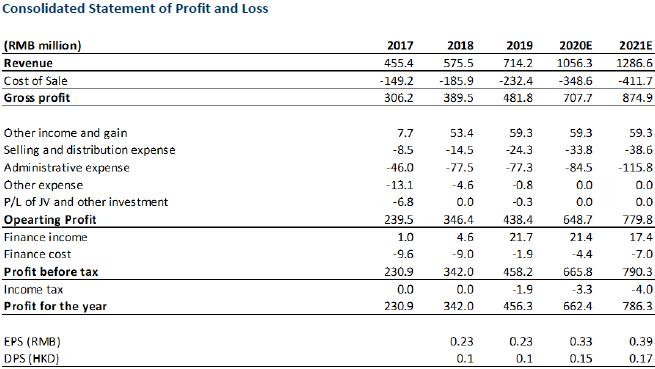

The company's 1H20 revenue was RMB 419 million (+16.7% yoy), GP was RMB 309 million (+22.6% yoy), NP was RMB 321 million (+31% yoy). The NP of Harbin Institute of Petroleum acquired in 1H20 was consolidated in the company's interim report as other income. Hence, the NP of the company was higher than the GP for the interim. If the revenue and cost of Harbin Institute of Petroleum is simulated to be consolidated into the company's interim report, the company's revenue/GP for 1H20 were RMB 478 million/RMB 353 million, with corresponding GPM at 73.8%. This simulated GPM was far higher than our previous expectation, which has fully demonstrated the company's strong post investment management and resource integration abilities. Further, as affected the COVID epidemic, the boarding fee refund of the company's self-built schools/ Harbin Institute of Petroleum were RMB 26 million/ RMB 6.1 million respectively. The 1H20 revenue would be RMB 445 million (+23.8% yoy) if excluding the effect of the boarding fee refund. Although the company saw a huge decrease in boarding fee in 1H20, but it was partly offset by the decrease in administrative expense ratio as the suspension of classes in 1H20 due to COVID. The administrative expense ratio was down by 2.8 ppt yoy.

Enrollment in 20/21 academic year has increased significantly yoy, we are expecting a huge organic growth in future

The number of enrollment for the company's undergraduate program in 20/21 academic year increased by 38% yoy to 11,213, ranking 1st in Guangdong Province. Within it, the number of enrollment for “junior college graduate into undergraduate program” was 3600, up by 11 times yoy. Since there are still no graduates from “junior college graduate into undergraduate program” yet, hence, the number of newly admitted students will be the net increase in the number of undergraduate students for 20/21 academic year. Further, the number of enrollment for junior college program in 20/21 academic year is 6572, up by 143% yoy. In terms of Adult college program and secondary vocational education program, the number of enrollment also increased year on year. As for tuition fee, the undergraduate fees of Guangdong Polytechnic College and Harbin Institute of Petroleum in 20/21 academic year will increase by 12% and 10% respectively yoy. The tuition fee of junior college program, Adult college program and secondary vocational education program will also increase by 5%,10% and 10% respectively. On the other hand, the company will expand 52,000 and 60,000 beds for boarding purposes respectively this year and next, laying a solid foundation for future enrollment expansion.

The “change in organizer” progress for Harbin Institute of Petroleum is going smooth, the company is expected to continue its M&A expansion in future

The NP of Harbin Institute of Petroleum has been consolidated into the company's interim report. The “change in organizer” progress for Harbin Institute of Petroleum is going smooth, we expect that revenue of Harbin Institute of Petroleum can be consolidated into the company's financial statement by the end of the year. On the other hand, the revenue/ GP for Harbin Institute of Petroleum from March to end of May were RMB 59 million/RMB 43 million, with corresponding GPM at 73.8% (+3.8ppt yoy), fully demonstrated the company's strong post investment management and resource integration abilities. We forecast the 2020E GPM of Harbin Institute of Petroleum would drop to 59% because of the industry seasonality effect, but it is still significantly higher than the GPM of 55% in 2019. At present, the tuition fee of Harbin Institute of Petroleum is lower than the average higher education tuition fee in the province, which doesn`t match with the company's leading employment rate and postgraduate entrance examination rate in the province. We believe the tuition fee of Harbin Institute of Petroleum still have much room to increase in future. Looking forward, the company currently has RMB 860 million in cash, plus the RMB 2.3 billion credit line from Shanghai Pudong Development Bank, the company has sufficient cash to make acquisitions in future. The company is expected to make 1-2 acquisition per year.

The new policies on the education industry mainly affects the Compulsory Education Sector and has tiny effect on Higher Education Sector

During the fifteenth meeting of the Central Committee for Comprehensively Deepening Reform (中央全面深化改革委員會第十五次會議) on the 1st of September, President Xi Jinping has presided over the guideline of vitalizing higher education in the country's central and western regions《關於新時代振興中西部高等教育的若干意見》and the guideline of standardizing private schools for compulsory education《關於規範民辦義務教育發展的實施意見》. The guideline of standardizing private schools for compulsory education 《關於規範民辦義務教育發展的實施意見》is in line with the Implementing Regulations for the Law for Promoting Private Education of the PRC (Revised Draft) (Draft for Review) 《民促法實施條例(修訂草案)(送審稿)》 issued in 2018. It restated the public welfare attributes of compulsory education (primary and junior high school).Further, the opinions on further strengthening and standardizing the management of education fees 《關於進一步加強和規範教育收費管理的意見》published by Ministry of Education and other four departments at the end of August is also consistent with the Implementing Regulations for the Law for Promoting Private Education of the PRC (Revised Draft) (Draft for Review) 《民促法實施條例(修訂草案)(送審稿)》, stating that the individual school fees can only be adjusted by the provincial Government for Non-Profitable Schools and for Profitable-Schools, school fees can be freely adjusted according to the market conditions.

In conclusion, the newly announced policies stated above only affect compulsory education. The guideline of standardizing private schools for compulsory education《關於規範民辦義務教育發展的實施意見》 once again emphasized that compulsory education can only be held on a non-profit basis, which has a negative impact on the future growth of compulsory education schools. In addition, standardizing private schools for compulsory education may potentially increase the capital investments on compulsory schools and hence extending the investment return cycle. However, we believe that for China Kepei, the contents of the above-mentioned new policies are consistent with those from the Implementing Regulations for the Law for Promoting Private Education of the PRC (Revised Draft) (Draft for Review) 《民促法實施條例(修訂草案)(送審稿)》. Since the schools of China Kepei will choose to operate as profitable schools and the schools of China Kepei are located in Guangdong and Heilongjiang provinces, where higher education can set prices independently and without the interference of the Government. Hence, future tuition fee increases and M&A of the company will not be limited by these policies.

Valuation

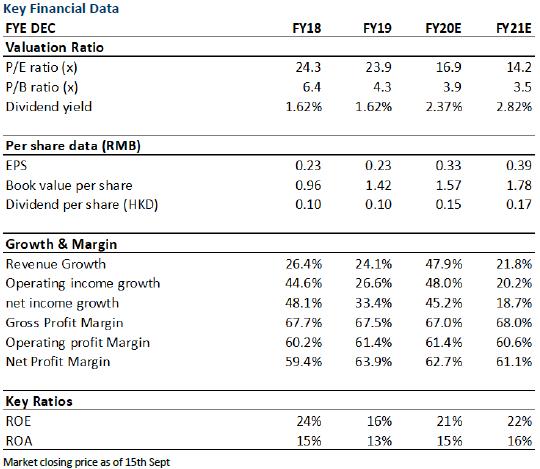

Overall, the company's 1H20 results were generally in line with our previous expectations. Taking into account of the refund of boarding fees during the period, the increase in the company's overall gross profit margin as well as the decrease of the admin expenses ratio in 2020H1, we have raised the 2020/2021 EPS to RMB 0.33/0.39. We raise the TP to HKD 7.67 (+6.5%), which implies 2020/2021 P/E ratio of 21.0x/17.7x. We upgrade the rating to “Buy”.

Risk:

acquisition not as effective as expected, teaching quality diminished, change of related law policies, the number of students increased less than expected

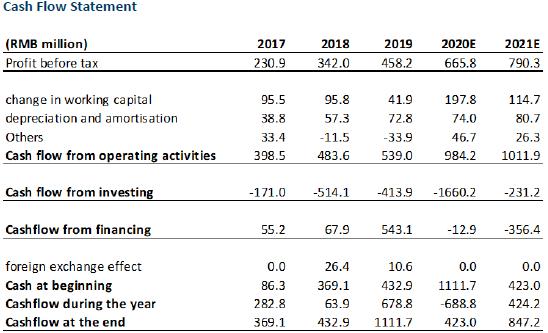

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()