-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

LI NING (2331.HK) - Profit alert for 1H21, revenue and profit beat

Wednesday, July 14, 2021  4771

4771

LI NING(2331)

| Recommendation | Neutral |

| Price on Recommendation Date | $87.500 |

| Target Price | $91.820 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

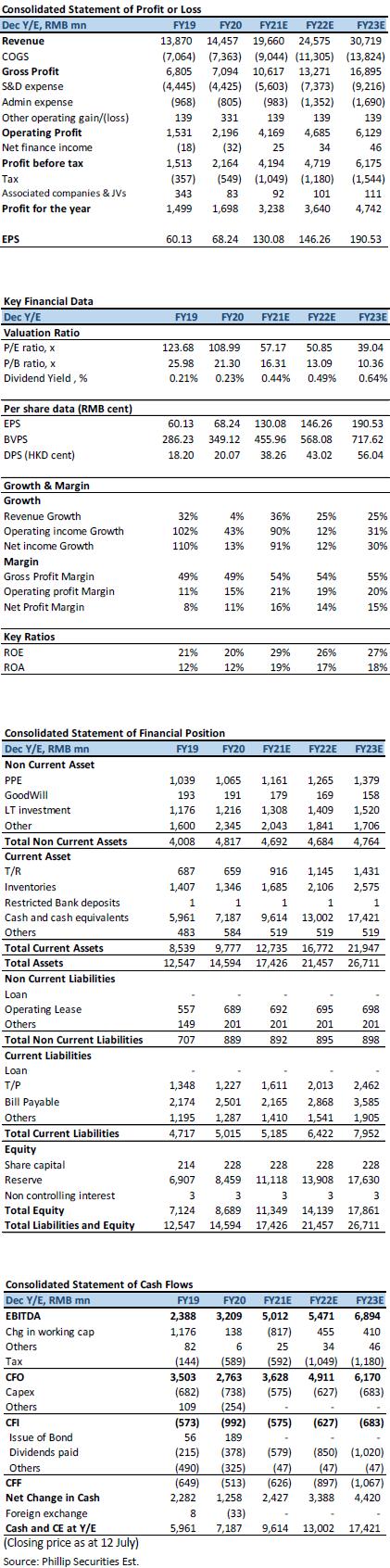

Li Ning announced on June 25 that the company expects to record a net profit of no less than RMB 1.8 billion for the six months ending June 30, 2021, an increase of 163% Yoy, mainly due to the company's revenue growth of more than 60% in 1H and the OPM continues to improve. The Xinjiang cotton incident stimulated the company's sales growth in 1H. The overall revenue slightly beat our expectations, and the net profit beat our expectations, mainly due to better profitability than we expected.

OPM improved significantly, and profit in 1H was better than expected

The company's revenue in 1H21 recorded a growth of no less than 60% over the same period last year. The company's revenue in 1H20 recorded approximately RMB 6.18 billion. Based on this, the company's revenue in 1H should be no less than RMB 9.89 billion, mainly due to low base in the same period last year, and the company was stimulated by events such as Xinjiang cotton in 1H. In terms of net profit, the company expects to be no less than RMB 1.8 billion, an Yoy increase of approximately 163.4%. The NPM is estimated to be approximately 18.2%, an increase of approximately 7.1 ppts over the same period last year.

The company's profitability performance is better than we expected. We believe that the main reasons can be divided into three aspects. First is the improvement of the company's retail discounts. The company was affected by the epidemic in the same period last year. With the improvement of terminal discounts, profitability has also improved. On the other hand, after the Xinjiang cotton incident, the sales of Li-Ning products are hot. Among them, the sales of China Li-Ning have recorded a significant increase. According to Ali data, during March to May 2021, the sales of China Li-Ning flagship store recorded up to 312%/813%/192% Yoy increase. As China Li Ning's unit price and GPM are higher than other products, the change in income structure is expected to increase the company's overall GPM during the period. In the third aspect, the Xinjiang cotton incident has brought a one-time sales stimulus and organic traffic to the company. Distribution expenses and administrative expenses can be converted more effectively, and the expense of period ratio is expected to be improved.

Good performance in 1H21, adjust the company's valuation model

The company's profit performance in 1H was better than we expected, but we believe that the advantageous performance in 1H would not last till the second half of the year. As the company's performance during the period was affected by a one-off event. In the long run, the company needs to invest additional resources in marketing, in order to further enhance the brand image. For the FY21, the company had expected sales growth of 20%-25% at the beginning of the year; on the profit side, it is expected to increase the NPM by 1 ppts in 2021. Based on the company's performance in 1H, we believe that the company's guidance is relatively conservative. In 1H, the company seized the opportunity to upgrade its brand, providing room for product price increases. In summary, we have adjusted the valuation model and raised the company's revenue in FY21/FY22/FY23 to RMB 196.6/245.8/30.72 billion (previously: RMB 182.0/227.6/28.44 billion); FY21/FY22/FY23 GPM Adjusted to 54%/54%/55% (previously 51%/51%/52%). FY21/FY22/FY23 net profit was revised up to RMB 32.4/36.4/47.4 billion (previously RMB 23.3/30.4/3.77 billion).

Valuation and investment advice

The company's revenue and profit side in 1H were better than our expectations. The Xinjiang cotton incident brought opportunities to the company, brought short-term stimulus to product sales, and also brought opportunities for the company to upgrade its brand. In 1H, due to the company's revenue growth and improved OPM, the company recorded a high percentage increase in the profit side. We believe that although the profitability in 1H would not last for the whole year, the profitability for the whole year will also be improved compared to last year. It is expected that the company will also raise the new performance guidance during the interim results meeting. As the company's revenue structure changes and brand image is established, the company's GPM is expected to further improve. The GPM in FY21/FY22/FY23 is forecast to be 54%/54%/55%. We raise the company's FY21/FY22 EPS forecast to RMB 130.08/146.26 cent (previously: RMB 93.66/122.28 cent). Maintain the target P/E to 60x in 2021, and raise the target price to HK$91.82, which corresponds to 60.00/53.36 times the expected P/E in FY21/FY22, corresponding to the current price, downgrades to a Neutral rating.

(Current price as of July 12)

Risk

1) A small increase in performance guidance

2) Weak consumer demand

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()