-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Pingduoduo (PDD) - Year-on-year revenue growth in 2Q24 increased, intensifying support for high-quality merchants

Friday, November 15, 2024  5347

5347

Pingduoduo

| Recommendation | Buy |

| Price on Recommendation Date | $117.000 |

| Target Price | $163.000 |

Weekly Special - 002050 Sanhua

Company profile

Pinduoduo (PDD) was founded in 2015, starting as an agricultural product retail platform. By eliminating intermediaries and connecting factories directly to users and surplus manufacturing capacity, it significantly reduces product prices. It has gradually evolved into a full-category e-commerce platform focusing on low-priced popular products and social group-buying. In terms of customer acquisition, Pinduoduo leverages the social traffic ecosystem of WeChat, utilizing group purchases among acquaintances to rapidly increase user numbers. Positioned as a platform for "low-priced popular products", Pinduoduo attracts a large number of low-tier and low-income groups with its high cost-effectiveness and free shipping. In September 2022, the company's cross-border e-commerce platform, Temu, was launched in the United States and has since expanded its presence to 53 overseas countries and regions across Asia, Europe, North America, Latin America, Africa, and Oceania. By December 2023, Temu had reached 470 million independent visitors and became the most downloaded iPhone app in the United States in 2023.

2Q24 YoY revenue increased, with plans to invest 1 billion yuan to support high-quality merchants

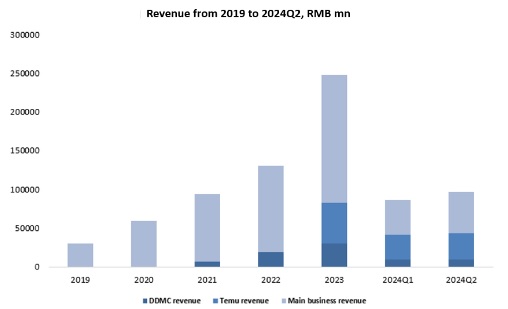

In the second quarter of 2024, the company achieved a total revenue of 97.1 billion yuan. Comparing to the same period last year, this represents an 85.7% increase. In terms of profitability, operating profit was 32.6 billion yuan, up by 156.0% year-on-year, and Non-GAAP net profit reached 34.4 billion yuan, a 125.5% increase year-on-year. Regarding segment revenues, online marketing revenue was 49.1 billion yuan, a 29.5% increase, primarily due to the improvement in the monetization rate of marketing products. Transaction service revenue was 47.9 billion yuan, showing a significant 234.2% increase driven by the growth in platform order volume and GMV. Management plans to waive 10 billion yuan in transaction fees over the next year, and it is anticipated that the growth rate of transaction service revenue will slow down. On the expense side, the company's total operating expenses for the quarter were 30.8 billion yuan, up by 47.5% year-on-year, mainly attributed to the increase in sales and marketing expenses. During the reporting period, sales and marketing expenses amounted to 26.0 billion yuan, a 48.5% increase year-on-year, primarily due to increased spending on promotional and advertising activities.

Main Business: marketing products continue to exert strong efforts, and revenue has significantly increased

According to data from the National Bureau of Statistics, in the second quarter of 2024, the national online retail sales amounted to 3.7909 trillion yuan, showing a year-on-year decrease. Among these figures, the online retail sales of physical goods reached 315.4 billion yuan, also experiencing a year-on-year decline. Contrasting this with the company's 2Q24 online marketing revenue growth of 29.5%, it highlights the strong development momentum of Pinduoduo's main business. Pinduoduo mainly focuses on white-label products and agricultural produce, characterized by highly standardized products without much differentiation in functionality. Price is considered the core competitive advantage, and both are seen as insulated from advertising placements. Therefore, in 2022, Pinduoduo launched the "Full-Site Promotion" marketing product for the first time, leveraging search and contextual traffic to drive a comprehensive increase in store transaction volume. This initiative supported bidding based on target investment ratios and transaction prices, swiftly activating sellers` willingness to invest. Additionally, during the 2019 618 shopping festival, Pinduoduo introduced the "Ten Billion Subsidy" program for the first time, attracting brands like Apple, Moutai, and Mystery of the Blue to swiftly join the platform, addressing brand participation concerns while enhancing the stickiness of high-spending customer groups.

With the main business continuing to expand its market share and maintain a leading position in terms of price perception, we hold an optimistic view on the continuous improvement of its monetization capabilities. It is projected that the main business's monetization rate could reach 4.5% by 2024. The platform is expected to attract ongoing advertising investments from merchants to achieve further growth.

Duoduo Maicai: include more high-margin products for profitability

Starting in 2023, Duoduo Maicai has shifted its focus from Gross Merchandise Volume (GMV) to optimizing profit margins by reducing personnel and lowering commission rates. Additionally, Duoduo Maicai has concentrated its operations on 78 self-operated units in 30 cities, requiring these units to minimize operational losses and achieve profitability as soon as possible. At the same time, Duoduo Maicai is continuously expanding its product range to include more high-margin products, aiming to increase user purchase frequency.

Temu: semi-consignment model launched in March while fully consignment business continues to reduce losses

2Q24, Temu's global sales continued to grow on a month-on-month basis, with significant improvements in the profitability of its fully hosted business. Considering the potential geopolitical impacts on Temu's operations in the United States, including plans by former President Trump to impose tariffs of 60% or higher on Chinese goods and congressional threats to include Temu in the Uyghur Forced Labor Prevention Act (UFLPA) entity list, the company has ceased advertising in the U.S. market since the Super Bowl. Future growth will primarily rely on organic traffic due to these factors, allowing for cost compression and ongoing reduction of annual losses.

Furthermore, in mid-March 2024, Temu introduced a semi-hosted business model where the company continues to procure from merchants, price products for consumers, conduct marketing, customer acquisition, and customer service, while merchants handle shipping from overseas warehouses and arrange end fulfillment. From Temu's perspective, the semi-hosted model offers several advantages, including shorter delivery times from local overseas warehouses, lower exposure to long-distance logistics cost fluctuations, and mitigation of fulfillment costs impact, along with the ability to expand SKU numbers and increase product prices.

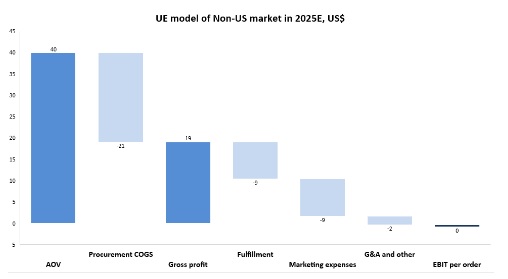

Due to the unclear prospects of Temu's operations in the U.S., the company is estimating its value using transaction data from non-U.S. regions. It is anticipated that under the semi-hosted model, the platform will increase the average order value, gradually reducing fulfillment costs, and by 2025, the UE model is expected to achieve pre-tax breakeven.

Investment thesis

Considering the current macroeconomic environment in China, global geopolitical uncertainties, and the company's continued focus on high-quality development while providing significant transaction fee reductions, short-term profits may fluctuate. However, in the long term, this can help promote the formation of a positive platform ecosystem.

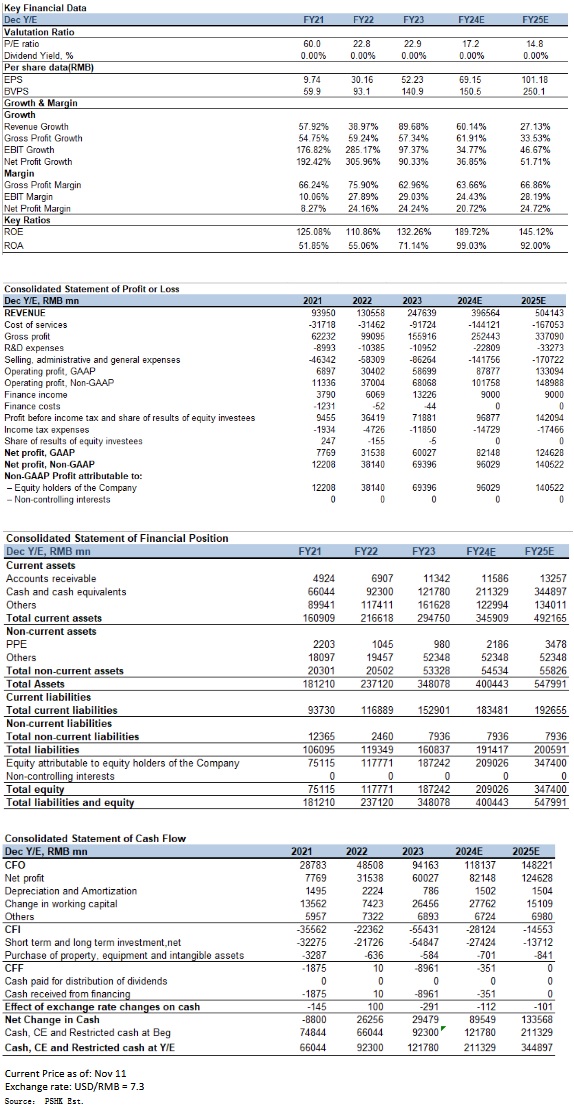

We forecast the company's operating revenue for 2024 and 2025 to be 396.6 billion yuan and 504.1 billion yuan respectively, with Non-GAAP net profits of 96 billion yuan and 140.5 billion yuan, corresponding to EPS of 69 yuan and 101 yuan, and PEs of 17.2x and 14.8x.

According to the SOTP valuation method, the total target market value for Pinduoduo in 2024 is estimated at 225.8 billion USD, with a target price of 163 USD, corresponding to a Non-GAAP PE ratio of 17.2x for 2024 and a rating of "Buy." The segmented values are as follows:

1. Pinduoduo Main Platform: 124 USD, based on a Non-GAAP PE ratio of 13x for 2024, considering potential higher profit growth with a premium of around 30% compared to the current average valuation of comparable companies in the e-commerce industry.

2. Duo Duo Mai Cai: 6 USD, based on a Non-GAAP PE ratio of 15x for 2024, matching the valuation assigned to other companies with similar business models.

3. Temu: 12 USD, based on a Non-GAAP PE ratio of 15x for 2025, considering the support of its rapid revenue growth.

4. Net Cash: 21 USD.

Risk factors

1) Overseas business performance below expectations; 2) Intensified competition in the e-commerce industries; 3) Impact of geopolitical issues on business development.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()