-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Kingsoft(3888.HK) - Strong growth in cloud services; New mobile games may resume the growth in gaming

Friday, July 5, 2019  18658

18658

Kingsoft(3888)

| Recommendation | Buy |

| Price on Recommendation Date | $17.300 |

| Target Price | $21.240 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

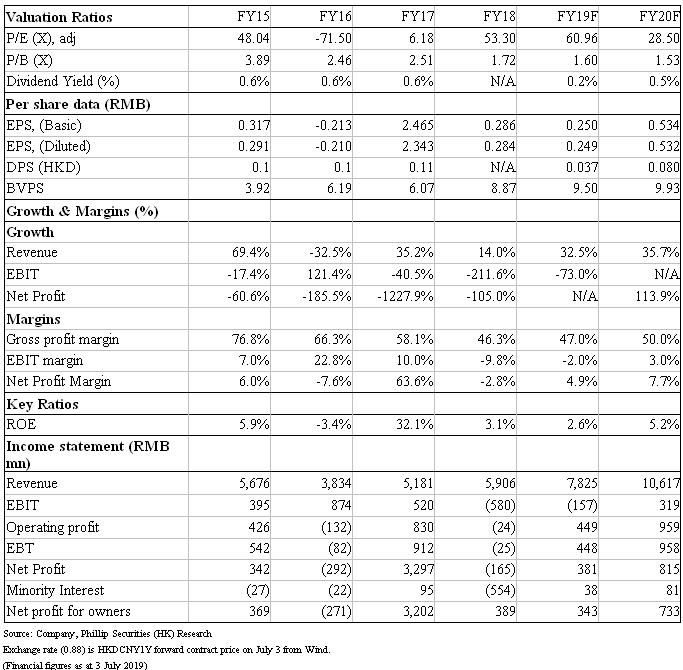

Kingsoft is a leading Internet company in China, engaging into three major business segments: games, cloud computing and office software. The new mobile games are launched, which could help resume the growth in gaming revenue. Besides, the growth in cloud services was stronger than expected, becoming the major growth driver for the Group. We derived a TP of HK$21.24, and maintain a “Buy” rating, with a potential upside of 22.8%.(Closing price at 3 Jul 2019)

First quarter results

The Group announced its first quarter results for 2019, where revenue was RMB 1.73 billion, a YoY increase of 37%, but a QoQ decline of 2%. Among them, the gaming revenue was RMB 600 million, down 5.2%; cloud service revenue was RMB 840 million, doubled YoY; while Office software and services and others were 290 million yuan, an increase of 35%. Gross profit margin decreased by 10.6% to 38.1%, mainly due to the increase in the proportion of businesses with lower gross profit margins.

New mobile games launched, resuming the growth in gaming

JX Online III mobile game was officially launched in June. According to七麥數據, as of July 3, the cumulative download volume of IOS and Android platforms has reached 7 million. Although the ranking of the game on each platform has fallen, we believe that it is normal for the ranking to fall after the player's introduction period in the first week. We believe that with the huge number of players in JX Online III PC, we believe that the performance of the JX Online III mobile game will also be good. In addition, the JX Online II mobile game is also expected to be launched in the third or fourth quarter of 2019, which will drive the revenue of mobile gaming in the second half. In relation to PC gaming, the group introduced the professional league club for JX Online III PC to enhance the attribution of an e-sport and the group also began to enter Tencent wegame. We estimate that the revenue of PC gaming will remain stable. Due to the influence of the gaming industry policy, the Group's gaming revenue has declined in 2018 and the first quarter of 2019, but we believe that under the launch of new mobile games, gaming revenue is expected to rebound slightly in 2019.

Stronger than expected growth in cloud services

With the rapid growth of mobile video and the government customers, cloud services have grown strongly, surpassing the annual growth guidance from management, indicating that the new annual growth guidance has been raised from 60% to 70%. In addition, the management also indicated that the net loss of the cloud business has been improved better than expected, and the operating profit margin in the first quarter has risen. Kingsoft Cloud has also cooperated with China Construction Bank and China Merchants Bank to develop financial services. We expect cloud business to maintain rapid growth and become the major growth driver of the Group.

WPS may be listed on STAR board

WPS revenue fell by 23% QoQ, but management explained that this was mainly due to seasonal factors and it is believed that the growth will resume in the next quarter. The Group launched WPS Office 2019 for Linux Professional and WPS office for Mac in March and April respectively, which is expected to further target more users. At present, WPS has successfully transformed into subscription model, and about 75% of its revenue comes from subscription. We believe that this model will bring stable cash flow. The Group is also preparing to list WPS on Sci-Tech innovation board (STAR), which will help to reflect the value of this business more realistically.

Valuation

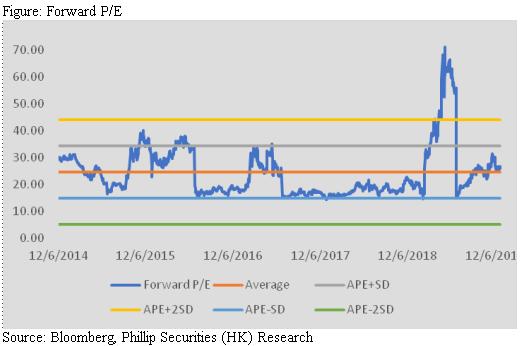

Based on a P/E ratio of 35x (the average of the past forward P/E plus a standard deviation) in 2020, we derived a TP of HK$21.24 and maintain a “Buy” rating , with a potential upside of 22.8%. (HKD/CNY=0.88)

Risk

1.Bad response from new mobile games

2.Lower than expected growth in cloud services

3.Lower than expected growth in the number of user in WPS

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()