-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

HASCO (600741.CH) - Continual Development of the Neutralization Strategy and Accelerated Development of New Business Layout

Wednesday, September 8, 2021  4090

4090

HASCO(600741)

| Recommendation | Accumulate |

| Price on Recommendation Date | $23.040 |

| Target Price | $27.500 |

Weekly Special - 1810 Xiaomi

Investment Summary

2021H1 Results Review

According to HASCO's 2021 semi-annual report, the Company's gross revenue for the Reporting Period was RMB66.611 billion, up 24.22% yoy, achieving a net profit attributable to the parent company of RMB2.73 billion, up 108.95% yoy, and a net profit attributable to the parent company excluding non-recurring items reaching RMB2.156 billion, up 141.28% yoy. The better-than-market-expected results were mainly due to the lower base affected by COVID-19 in the same period last year and the Company's opportunity of incremental sales from premium brands and self-owned brands. Compared to the same period in 2019, the three are still down 5.6%/18.8%/23.2% respectively.

The revenue of the Company's five major business sectors, interior and exterior trim parts/metal moulding and moulds/functional parts/electrical and electronic parts/thermal processing parts, increased by 24.8%/29.68%/14.19%/39.29%/31.29% yoy, accounting for 70%/7.4%/18%/4.3%/0.45% of the gross revenue, respectively. In terms of net profit composition, net profit of interior and exterior trim parts/metal moulding and moulds/functional parts/electrical and electronic parts/thermal processing parts increased 72.6%/29.68%/14.19%/39.29%/31.29%, respectively compared with the same period last year, accounting for 49%/6.8%/40%/2.4%/1.2%. Interior and exterior trim parts and functional parts are still the main source of the Company's profit.

YoY Increase of Gross Margin

The integrated gross margin in 2021H1 was 14.59%, compared with 13.28%/14.68% in the same period of 2020/2019, respectively. Excluding the pandemic influence last year, the Company's gross margin in H1 basically recovered to the level of the same period of 2019. By quarter, Q1/Q2 gross margin was 14.9%/14.26%, respectively, with a slight decline in Q2 qoq mainly due to chip supply tensions and raw material price increases. Net profit margin was 5.14%, an increase of 2.06 pct yoy, but was down 1.06 ppts from the same period in 2019. The Company's main customer SAIC Motor has been affected by the slowdown in the growth of fuel vehicles in recent years, while the electrification layout lagged behind, and sales volume was under pressure, causing a drag on the profitability of the Company's parts business. In order to understand the future trend of change in the automotive industry, the Company focused on the improvement of its R&D capability and continued to increase its R&D investment. The R&D expense ratio in H1 was 4.41%, an increase of 0.31 ppts yoy and 0.83 ppts compared with the same period in 2019..

Continual Development of the Neutralization Strategy and Accelerated Development of New Business Layout

The neutralization strategy aimed at reducing customer concentration will continue to advance. The Company's automotive interior trim, seats, airbags, front and rear subframes and other businesses have been part of the supporting orders for luxury brands such as Mercedes-Benz, BMW and Audi, as well as the new generation of relevant models of independent brands such as Great Wall Motors, Geely and BYD. The business of automotive interior trim parts, seats, lighting, tailgate, etc. has been partially supplied to Tesla, Nio, Xpeng and other new energy automobile brands. In 2021H1, the non-SAIC Motor revenue share of the Company's revenue increased from 46.1% in 2020 to 48% in 2021H1.

With the continuous development of the global automotive industry such as electrification and intelligent network connection, the Company is also accelerating its development in the emerging business. In the field of smart cockpit, the subsidiary Yanfeng has completed the development and matching of smart cockpit controller based on the high-performance computing for many types of mainstream operating systems, which will be provided for SAIC's own models. Some smart cockpit components have been provided for SAIC's car companies, Geely and Tesla. In the field of intelligent driving, the self-developed 4D imaging millimetre wave radar is scheduled for mass production in the fourth quarter of this year. The 77GHz forward millimetre wave radar has made a breakthrough in some projects, and the DLP digital headlights of Huayu Vision have been mass produced. In terms of intelligent power, the Company's semi-annual report disclosed the sales volume of new energy products for the first time. HASCO continues to improve the process of drive motor flat wire and round wire to ensure the supply of pure electric vehicle platform drive motors for SAIC passenger cars and Volkswagen MEB. The Company sold 97.9 thousand sets of drive motors and 30 thousand sets of drive systems in H1.Overall, the Company aims to continue to achieve its annual revenue target of RMB142 billion by expanding its premium customer markets and overseas markets and accelerating product mix restructuring and technological innovation..

Investment Thesis

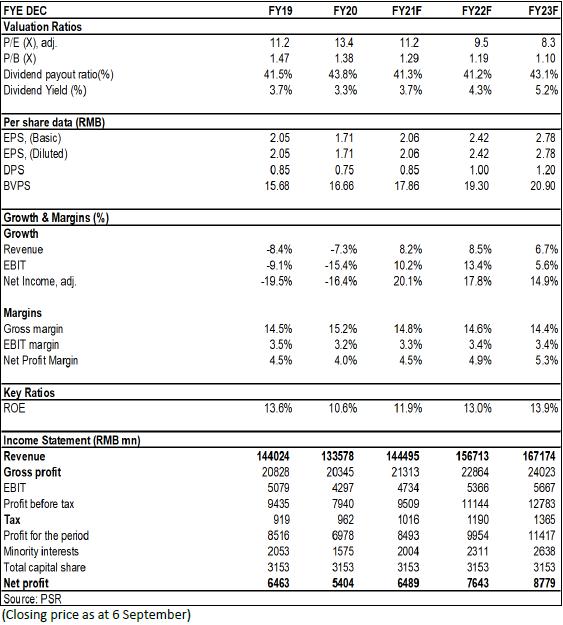

We expect the Company to continue to achieve a solid recovery by optimizing its customer structure and expanding its product layout. As analyzed above, we gave EPS expectation of the Company to RMB 2.06/2.42/2.78 of 2021/2022/2023. And we accordingly gave the target price to 27.5, respectively 13.4/11.3/9.9x P/E and 1.54/1.42/1.32x P/B for 2021/2022/2023. "Accumulate" rating. (Closing price as at 6 September)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()