-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Medical System (867.HK) - Introducing Six Injection Products and Acquiring Elcitonin Rights

Monday, July 30, 2018  12525

12525

China Medical System(867)

| Recommendation | BUY |

| Price on Recommendation Date | $13.900 |

| Target Price | $21.000 |

Weekly Special - 1810 Xiaomi

Investment Summary

We see stock price decreasing during recent market fluctuation. Expect for market factors, we partly attribute price volatility to unfavorable test results of one key pipeline product (Traumakine). However, we emphasize that R&D will not affect the growth momentum of current portfolio and introduction of new drugs. We maintain previous EPS forecast of RMB0.77/0.86 and TP HKD21, and suggest buying around price bottom. (Closing price at 26 July 2018)

Introducing of Six Injection Products

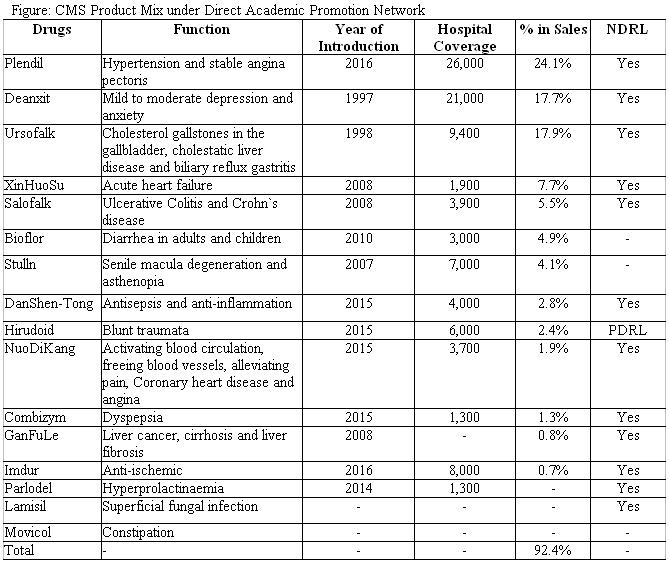

On 20 July, CMS entered into an agreement with Venus Pharma to acquire d all assets of Venus Pharma's current product portfolio related to China market (involving know-how, all intellectual property or the right of application for the intellectual property, and other rights to commercialize the products in China). There are six main products and all included in Class B content of NDRL, commonly used drugs for clinical anti-tumor therapy and recommended by guidelines. Other two drugs belong to carbapenem antibiotics, having a wide range of antibacterial effects and being used to treat a variety of infections. We know from our checks that these drugs may attain drug import registration certificate within 1 to 1.5 years, and we regard these mid-term drivers for company development.

Acquiring Promotion Rights of Elcitonin

CMS gained exclusive promotion rights of Elcitonin (Elcatonin Injection, an original synthetic calcitonin derivative), dated from Aug 2018. Elcitonin, originally developed by a Japanese pharmaceutical firm Asahi Kasei Pharma, is commonly used anti-osteoporosis drug and also recommended by “Primary Osteoporosis Diagnose and Treatment Guideline (2017)”. It has been marketed in China for several years and categorized as Class B of NDRL. Now the number of osteoporosis patients in China exceeds 70mn which means great market potential for development. Asahi Kasei Pharma, headquartered in Tokyo, is a research-based healthcare innovator that discovers, develops, manufactures, and markets pharmaceuticals and diagnostic products that address unmet medical needs. We highlight this cooperation will underpin way for further collaboration between CMS and Asahi Kasei.

FY17 Results

In 2017, excluding Two-invoice System effect, CMS reported revenue of RMB5578.6mn, +21.2% YoY, GPM saw 1ppt decrease due to ASP down by 1.9pp. We highlight efficient cost control measures, given EBITDA margin increased by 0.7ppt, with percentage of selling/administrative expenses in revenue dropping by 0.8pp. And NPM kept stable. Its payout ratio maintained around 40% intact.

Investment Thesis, Valuation & Risk

Our valuation model gives target price of HK$21.0. We highlight future growth momentum coming from increasing penetration of current hospital coverage and introduction of new drugs. Excluding possible pipeline contribution and new introduction, we assume relatively stable expenses ratios and predict 18E/19E EPS to be RMB0.77/0.86, based on current product mix potential. Thus we give target price of HKD21.0, BUY recommendation. (Exchange rate= 0.8706 RMB/HKD)

Risks include: R&D fails expectations; Policy risks; Exchange risk; New introduction fails expectation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()