-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of March. 2020

Wednesday, April 1, 2020  10219

10219

Report Review of March. 2020

Weekly Special - 002472.CH Shuanghuan Driveline

Sectors:

Air & Automobiles (Zhang Jing),

Environment (Leon Duan)

Automobile & Air (ZhangJing)

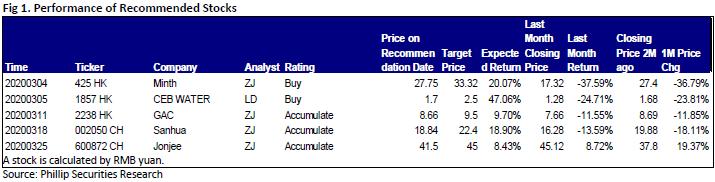

This month I released 4 updated reports of Minth (425.HK), GAC (2238.HK), Sanhua (002050.CH), and Jonjee (600872.CH), which got success by their unique Competitive edge. Among them, we highly recommend Jonjee (600872.CH).

Jonjee Hi-Tech reported revenues of RMB4675 million in 2019, an increase of 12.20% yoy; a net profit attributable to the shareholders of the listed company of RMB718 million, an increase of 18.19% yoy, and an EPS of RMB0.9 compared with an EPS of RMB0.76 last year. The result was basically in line with our expectations at the beginning of last year. The result of company's condiment sector maintained a fast growth, the annual revenue of Meiweixian in 2019 was RMB4468 million, up by 15.98% yoy, an 6% increase in growth rate compared with last year; the company reported a net profit of RMB796 million, up 27.6% yoy.

The Company mentioned the 5-Year Goal of Double Hundred, which was to reach 1 million tons of output and RMB10 billion in revenue by 2023. In order to achieve this objective, the Company has not only steadily promoted the second-phase expansion project of the Yangxi Plant, but also planned to invest RMB1275 million to upgrade and expand the Zhongshan Plant to increase the production capacity from the current 314,300 tons to 584,200 tons. It is estimated that the project will bring in a revenue increase of RMB1575 million and net profit of RMB355 million. On the other hand, channel sinking and employee incentives will be enhanced. The development rate of prefecture-level cities will be increased to 87.83%, and the development rate at district and county level will reach 46.23%. We-Media and online advertising will continue to be strengthened.

After Baoneng taking over the company, the improvement of the incentive mechanism and management efficiency will lay a foundation for the Company's long-term development. The narrowing of the gap with the first-tier companies is also expected to open up space for the company's growth.

Environment (Leon Duan)

I released update reports on CEB WATER (1857.HK). In 2019, the company recorded revenue of HKD 5.55 billion, a year-on-year increase of 16%, an increase of 2.4 percentage points from the first three quarters of 2019. The increase in revenue was mainly due to an increase of HKD 300 million in construction revenue, an increase of HKD 300 million in operating income, an increase of HKD 76 million in financial revenue, and an increase of HKD 99 million in technical services revenue, representing year-on-year growth of 11%, 25%, 10% and 98%. The above-mentioned increase in revenue was mainly due to the increase in new projects, the operation of some new projects and the increase in water prices of some projects. The company's gross profit was HKD 1.89 billion, a year-on-year increase of 17%, which was 2.1 percentage points lower than the growth rate of gross profit in the first three quarters of 2019. The gross profit margin was maintained at 34% because the revenue share of construction business (about 24% gross profit margin) and operating services (about 47% gross profit margin) was similar to the previous year. Among them, construction revenue, construction contract revenue and technical service revenue totaled approximately 58%.

Profit attributable to equity holders of the company was HKD 830 million, an increase of 23% year-on-year, and an increase of 5.9 percentage points from the first three quarters of 2019. The company's various operating indicators exceeded our expectations, reflecting the company's good project growth and cost management capabilities.

We believe that the impact of the new pneumonia epidemic on the company is relatively limited. Although the shutdown of some industrial enterprises has affected the wastewater treatment capacity of the company's industrial park, a slight increase in municipal domestic sewage offsets this impact, and the industrial wastewater treatment capacity is expected to gradually recover in the near future, and I believe that it will soon return to normal levels. In terms of construction projects, the company's resumption of work after the holiday this year has been delayed compared to previous years, but it has gradually resumed work. I believe the government's encouragement of resumption of production will gradually ease the shutdown happening. In addition, the company's liability ratio increased slightly in 2019, an increase of 2.1 percentage points from last year to 57.9%. However, the return on shareholders` equity also increased by 1.4 percentage points to 9.9%, reflecting the improvement of the company's profitability. The dividend payout ratio increased slightly by 2 percentage points to 25%. The company's management believes that there is still room for improvement in the future dividend payout ratio. In addition, the company expects capital expenditure of approximately HKD 3 billion in 2020, which will maintain approximately the same growth rate as in 2019.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()