-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

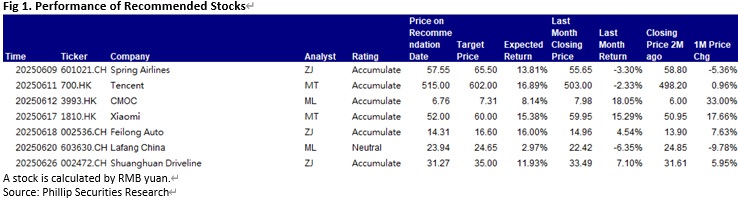

Report Review of June 2025

Friday, July 4, 2025  1380

1380

Weekly Special - 1810 Xiaomi

Sectors:

Automobile & Air (Zhang Jing)

Utilities, Commodity (Margaret Li)

TMT, Semiconductors (Megan Tao)

Automobile & Air (Zhang Jing)

This month I released 3 updated reports of Spring Air (601021.CH), Feilong Auto (002536.CH), Shuanghuan Driveline (002472.CH). Among which, we prefer Feilong Auto and Shuanghuan Driveline.

Feilong Auto Components Co., Ltd. was established in 2001 and is a leading enterprise in the domestic automotive thermal management sector, maintaining strong growth momentum in both traditional and new energy tracks. In the field of traditional thermal management, the Company continues to consolidate its market advantage with three core products: mechanical water pumps, exhaust manifolds, and turbocharger housings (abbreviated as “turbo housings”). In the field of new energy system cooling, its main products include the electronic water pump series and thermostat valve series. Currently, the Company is implementing a dual-track penetration strategy of “automotive + general industrial”, developing a second growth curve in non-automotive sectors, focusing on intelligent liquid cooling solutions for 5G base stations, AI computing centres, new energy storage, hydrogen energy equipment, and high-end agricultural machinery, thereby enabling the cross-industry application of thermal management technology.

From 2007 to 2024, the Company achieved a compound growth rate of 13.7% in total operating revenue. In 2024, revenue reached RMB4723 million, up 15.34% yoy. By business segment, revenue from engine thermal management energy-saving and emission-reduction components grew by 19.4%, while revenue from new energy-related components increased by 40.44%, becoming the primary growth driver. Although revenue in the first quarter of 2025 declined by 10.55% yoy to RMB1.11 billion, net profit rose against the trend by 3.06% to RMB123 million. Gross margin improved by 4.84 ppts yoy to 25.33%, mainly due to optimised product mix and effective cost control.

In 2024, revenue from new energy and non-automotive sectors reached RMB526 million, up 40.44% yoy. The Company’s flagship product is the electronic water pump, with power ratings ranging from 13W to 3500W and current production capacity of 5.6 million units. In 2024, the Company’s market share exceeded 10%, ranking fourth in the market. Recently, the Company signed a supply agreement with BYD for 500 thousand sets of electronic oil pumps, marking recognition of its technical strength in the new energy thermal management sector by a leading automaker.

The Company is showing strong momentum in capacity expansion within the new energy thermal management field. The commencement of phase II projects at its Zhengzhou and Wuhu plants has enabled large-scale production of thermal management integrated modules, which entered mass delivery in January 2025. The Company expects annual production capacity for new energy thermal _1461756321.docnew energy thermal management components to reach up to 8 million units, covering electronic water pumps and thermostat valve series, sufficient to support approximately 1.2 million new energy vehicles. Currently, its Thai subsidiary, Longtai Auto Parts (Thailand) Co., Ltd., is under orderly construction, with a total investment of approximately RMB500 million. Trial production is scheduled to begin by the end of June 2025, with full-scale production expected by year-end. Once fully operational, it is projected to achieve annual production capacities of 1.5 million turbo housings, 1 million exhaust manifolds, 500 thousand mechanical water pumps, and 1 million electronic water pumps. Upon reaching full capacity, the plant is expected to generate up to RMB1.5 billion in incremental revenue.

With the rising penetration of new energy vehicles and increasing demand for liquid-cooled servers, the Company’s dual-track strategy of “automotive + general industrial” is expected to continue unlocking result potential. We remain optimistic about the Company’s development prospects.

As for valuation, we expected diluted EPS of the Company to RMB 0.75/0.98/1.11 of 2025/2026/2027. And we accordingly gave the target price to RMB16.6, respectively 22/17/15x P/E for 2025/2026/2027. "Accumulate" rating.

Shuanghuan Driveline specializes in the manufacturing of gear transmission products, with the gear business accounting for about 80% of the Company's total business. The Company has gradually shifted from traditional gear products to high-precision gears and parts. Its main products span gear products (gears for passenger vehicles, commercial vehicles, engineering machinery, motorcycles and electric tools), reducers and other products, which are mainly applied in the electric drive systems, gearboxes and axles of vehicles, as well as electric tools, rail transit, wind power, industrial robots and other sectors.

In 2024, the Company recorded revenue of RMB8,781 million (RMB, the same below), up 8.76% yoy; net profit attributable to the parent company amounted to RMB1,024 million, up 25.42% yoy; net profit attributable to the parent company excluding non-recurring items was RMB1,001 million, up 24.64% yoy. EPS was RMB1.22, with a dividend per share of RMB0.226, representing a dividend payout ratio of 18.5%.

In Q1 2025, the Company reported revenue of RMB2,065 million, down 0.47% yoy, mainly due to the contraction of the steel trading business. Excluding this impact, core business revenue grew 12.5% yoy; net profit attributable to the parent company reached RMB276 million, up 24.70% yoy; and net profit attributable to the parent company excluding non-recurring items was RMB269 million, up 28.27% yoy.

Among the various business segments, the new energy vehicle (NEV) gear business delivered standout performance. In 2024, this segment generated revenue of RMB3.37 billion, accounting for 38.38% of the Company’s total revenue, up 51.21% yoy, showing a strong upward trend. In Q1 2025, this segment continued to grow at a pace exceeding that of downstream NEV sales, further increasing its share of total revenue and becoming a key driver of performance growth.

The Company’s net profit margin reached 11.66% in 2024, up 1.55ppts yoy; and rose further to 13.37% in Q1 2025, up 2.7ppts yoy, indicating continued improvement in profitability.

In the high-profile NEV gear field, the Company had established an annual production capacity of 6,500 thousand sets for NEV transmission gear shafts by the end of 2024, with full capacity utilisation. The production base for NEV transmission components in Hungary is currently in the equipment commissioning phase, with capacity to be gradually released based on existing orders. As construction of the Hungary plant progresses, delivery lead times and logistics costs will be reduced, laying a solid foundation for further global market expansion.

Centred on gear technology, the Company continues to advance its diversified product layout. Looking ahead to the next two to three years, development across business segments includes: first, driven by growing sales of domestic B-class and above models, demand for high-precision, low-noise gear products is surging. As a leading player in China’s NEV gear market, the Company is expected to further increase its market share by leveraging its technological advantages and optimising its sales structure. Additionally, the coaxial reducer gear (used in industrial robots) and intelligent actuator (used in robotic vacuum cleaners) segments offer vast market potential and are likely to become new growth drivers. Other segments, including commercial vehicles and construction machinery, are expected to remain generally stable over the next two years.

Shuanghuan Driveline is a pacesetter in the domestic automotive gear industry and robotic RV reducer industry. By leveraging its advantages in capacity, management, R&D and customer base, the Company has seized the opportunities for upgrading brought by gear outsourcing and high industry barriers as a result of the booming new energy vehicle industry. Looking forward, the Company is expected to continuously benefit from the boom of new energy passenger vehicles, expansion of the industrial chains of automatic gearboxes of commercial vehicles, and rapid development of robotic reducers and gears for daily use.

As for valuation, we expected diluted EPS of the Company to RMB 1.48/1.72/2.07 of 2025/2026/2027. And we accordingly gave the target price to RMB35 respectively 24/20/17x P/E for 2025/2026/2027. "Accumulate" rating.

Utilities, Commodity (Margaret Li)

This month I released 1 update report of CMOC Group Limited (3993.HK) & 1 initiation report of Lafang China (603630.CH).

Acquisition of the gold company promotes business diversification. In April, the company announced that it would acquire all issued and outstanding common shares of Lumina Gold Corp at the price of C$581 million. Lumina Gold is a precious metal and base metals exploration company listed on the Toronto Stock Exchange. The company owns 100% interest of the Cangrejos gold-copper project in El Oro Province, southwest Ecuador. Cangrejos is a large-scale primary gold-copper project in Ecuador, and the pre-feasibility study was completed in 2023. The pre-feasibility study report highlighted that the project had measured and indicated resources of 1.376 billion tonnes at 0.46 g/t gold, totaling 638 tonnes of gold; proven and probable reserves of 659 million tonnes at 0.55 g/t gold, equating to 359 tonnes of gold. The mine life was expected to be 26 years. Characterized as a large-scale porphyry deposit, Cangrejos features low stripping ratios, favorable open-pit mining conditions, and strong existing infrastructure including access to power, water, roads, and ports, so the mining cost will be competitive. Continued exploration is underway both within the current concession and at depth. This acquisition indicated that CMOC had begun to enter the gold field and promote the diversification of its businesses. Coupled with the high gold prices, it is expected to bring growth to the company's revenue in the future.

The company had made guidance for the annual output of its main products in 2025, among which copper would be 600,000-660,000 tons; cobalt would be 100,000-120,000 tons; molybdenum would be 12,000-15,000 tons; tungsten would be 6,500-7,500 tons; niobium would be 9,500-10,500 tons; phosphate fertilizer would be 1.05-1.25 million tons, and the physical trade volume would be 4-4.5 million tons. The overall guidance output was higher than last year. Combined with our forecast that copper price will be at a high level and cobalt price will rise, the company's volume and price resonance is expected to achieve sustained growth in operating income. We also look forward to the development of the company's new business after the completion of the acquisition of the gold company and the changes brought to the company by the management adjustment. We raise our revenue forecast for the company, we predict that the company's revenue will be 219.4 billion yuan, 225.9 billion yuan and 233.8 billion yuan respectively in 2025-2027. EPS will be 0.72/0.85/0.99 yuan. BVPS will be 3.47/3.72/3.91, corresponding to the P/B of 1.79x/1.67x/1.59x. The company is given a P/B of 1.93 times in 2025 (Similar to the average price-to-book ratio over the past year), with a target price of HK$7.31, and we keep the investment rating of " Accumulate ". (Current price as of June 09)

TMT, Semiconductors (Megan Tao)

In this month, I published two research reports on Tencent (700.HK) and Xiaomi (1810.HK).

In the first quarter of 2025, the company recorded total revenue of RMB 180 billion, representing a 12.9% year-on-year increase. In terms of profitability, non-IFRS operating profit reached RMB 57.6 billion, up 9.5% year-on-year, with the operating profit margin slightly decreasing to 32.0% from 33.0% in the same period last year. Non-IFRS net profit for the period amounted to RMB 49.7 billion, increasing by 16.6% year-on-year. By segment, value-added services revenue in 1Q25 grew robustly by 17.1% year-on-year to RMB 92.1 billion, primarily driven by contributions from the domestic games business against a low base effect in the prior year. Online advertising revenue rose 20.2% year-on-year to RMB 31.9 billion, benefiting from increased user engagement, continuous AI-powered upgrades to the advertising platform, and enhancements to the Weixin transaction ecosystem. FinTech and Business Services revenue increased by 5.0% year-on-year to RMB 54.9 billion, mainly due to growth in consumer loan services and wealth management services, as well as increased revenue from cloud services and merchant service fees.

Overall, we remain optimistic about AI-driven medium-to-long-term growth. We raise our 2025-2027 revenue forecasts to RMB 737.9/809.9/885.9 billion and non-IFRS net profit estimates to RMB 295.0/315.3/346.7 billion, translating to EPS of RMB 28/30/33. The current share price implies a PE of 17/16/14x. Based on SOTP valuation—applying a 10% discount to the latest market values/valuations of subsidiaries and invested companies—we derive a 2025 target market cap of RMB 5.1 trillion for Tencent, equivalent to a target price of HKD 602. We upgrade our rating to "Accumulate".

In the first quarter of 2025, the company achieved total revenue of 111.3 billion yuan (RMB, same below), representing a 47.4% year-on-year increase; in terms of profitability, operating profit reached 13.1 billion yuan, up 256.4% year-on-year, while adjusted net profit hit 10.7 billion yuan, reaching a historic high with a 64.5% year-on-year growth. For segment revenue, 1Q25 smartphone × AIoT revenue amounted to 92.7 billion yuan, growing 22.8% year-on-year, primarily driven by increased smartphone shipments; innovative businesses including smart electric vehicles generated revenue of 18.6 billion yuan, with a gross margin of 23.2%.

For non-automotive businesses, the smartphone market uptrend will continue into 2025, while China's stimulus policies are expected to drive consumption recovery. The company will benefit from its premiumization strategy, progressively upgrading product AI capabilities. For automotive business, the company's revenue is poised to maintain rapid growth alongside steady gross margin improvement. Overall, we remain positive about the company's medium-to-long-term growth prospects, valuing it at 35x 2025 PE with a target price of HK$60 per share. We forecast 2025-2027 revenue at RMB490.6/600.4/704.0 billion and net profit at RMB39.7/49.5/59.2 billion, translating to EPS of RMB1.59/1.98/2.37. Current share price implies 30/24/20x PE from 2025 to 2027. Consequently, we upgrade our rating to "Accumulate".

Want to learn more about related option strategies? Click here.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()