-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ZTE Corporation (763.HK) - Colorful hotspots in new business

Thursday, October 16, 2014  22894

22894

ZTE Corporation(763)

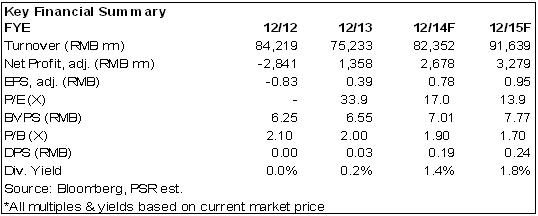

| Recommendation | Buy |

| Price on Recommendation Date | $16.680 |

| Target Price | $21.580 |

Weekly Special - 002050 Sanhua

In the first half year, ZTE Corporation only recorded a growth rate of 0.5% in its revenue, which reached RMB37.6 billion. It is mainly due to the hedge of the carriers` network income growth against the decline of revenue from mobile phone terminal, telecom software system and service, etc. However, benefiting from the improvement of overseas contract’s gross margin, higher contribution from IDC business, the company`s profitability went up continuously with the gross margin increasing by 4 percent points to 29.5% on year-to-year basis. Therefore, the company recorded a net profit of RMB1.13 billion in the first half year with a growth of 263.9%. ZTE Corporation also predicted that the net profit in the first three quarters could reach RMB1.70 to RMB1.90 billion, that is, the net profit in the third quarter will be between RMB570 million to RMB770 million.

In 4G era, the company elevated its investment in research and development constantly, which also brought the promotion of competitiveness. The company is taking the lead in the inland 4G market. The second half year till 2015 will be the CAPEX peak in Mainland telecom industry. The company is expected to be the main beneficiary. Meanwhile, the gross margin of mainland network devices reached 45%, so the profitability of the company will retain stable, even record an increase.

ZTE Corporation has for the first time entered in large scale into the high-end router market of China Mobile, ranking No. 2 in market share, while the previous high-end router suppliers such as Cisco and Juniper were out. The elimination of overseas suppliers indicates that operators are paying more attention to information safety, and it is expected that the domestic high-end router market in future will create the duopoly structure of ZTE and Huawei. In addition, the market has the features of high technology threshold and strong profitability. Therefore, this bidding-winning indicates that ZTE will continue to improve its market share in mainland and its gross margin.

At present, the commercially available high-power wireless charging system can be supplied only by three overseas suppliers including Qualcomm and only ZTE in Mainland. Its high-power electromagnetic induction wireless charging system has passed the identification of scientific and technological achievements and can realize 90% of charging efficiency under the 30KW high-power system. It has the leading technology globally, and has applied for more than 20 patents. As the wireless charging has many advantages such as convenience, no need for land requisition, safety and reliability, it is hoped to solve the main obstacle of the inconvenience of the charging of electric cars and gain a further wide popularization. At present, in the 40 domestic new energy demonstration cities there is a market volume of more than 400 thousand public buses, and in future the market scale for their wireless charging system is expected to reach hundreds of billions.

Investment Action

Under the big background of the transformation of China economy, the tendency of more information infrastructure investment is irresistible, and the government also carried out the supporting policies for stimulating information consumption and broadband construction successively. Thus, ZTE Corporation and other local comprehensive suppliers of information devices are expected to welcome a medium and long term spring. Moreover, the company policy is focused on profitability instead of production scale, resulting in the high level of the profitability in the future.

Viewing from the historical valuation, the company`s valuation once reached 37 times during the peak period of 3G capital expenditure in 2009, and its average price earnings ratio has also achieved 22 to 23 times in downturn period since 2011. Even if we conservatively give the company 22 times corresponding to the price earnings ratio valuation of EPS in 2014, the target price can still reach 21.58 HKD. We maintain it "Buy" rating.

Continuous improvement of profitability

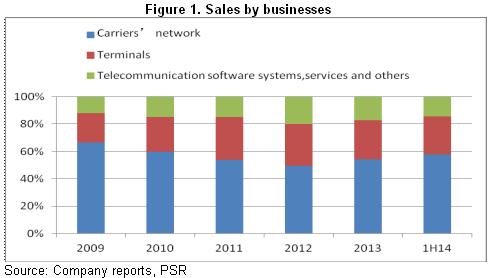

According to the interim report, ZTE Corporation in the first half year only recorded a growth rate of 0.5% in its revenue, which reached RMB37.6 billion. To be specific, although the company`s carriers` network income increased 14.6% benefiting from the increase of revenue from TD-LTE and FDD-LTE system device, the company`s revenue from the mobile phone terminal, telecom software system and service decreased by 16.5% and 9% respectively due to the decrease in the operation revenue from inland 3G mobile phone, video, network terminal and international service.

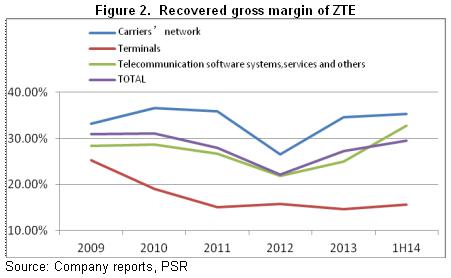

Notably, the company`s profitability picked up continuously with the gross margin increasing by 4 percent points to 29.5% on year-on-year basis. Among that, carrier network business’s gross margin increased by 2.9 percent points to 35.3% due to the increase from overseas contract’s gross margin and the proportion of 4G system devices. Moreover, the gross margin of telecom software system and service increased significantly by 5.6 percent points to 32.7%, which mainly benefited from the IDC business of high gross profit and the increase from government and enterprise customers` income contribution.

Benefiting from the improvement of profitability, the company recorded a net profit of 1.13 billion in the first half year with a growth of 263.9%. ZTE also predicted that the net profit in the first three quarters could reach 1.70 to 1.90 billion, that is, the net profit in the third quarter will be between 570 to 770 million.

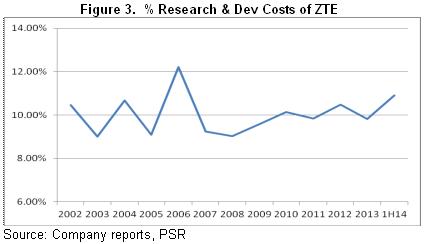

The contribution of 4G will improve

In the 3G age, limited by the factors including the lagging behind of 3G process in Mainland and contracts of low gross margin, the company`s competitiveness was weakened and the performance was in a downturn. However, in 4G Age, the company continuously improved its investment in research and development, and the proportion of expenditure in research and development in income even increased to 10.9% in 1H14, the highest level since 2007, which brought the great improvement of competitiveness to the company as well.The company has gained 34% market shares in the second phase bidding of China Mobile TDD-LTE master device, and gained 42% market shares in the first phase bidding of China Telecom FDD-LTE master device, and 25% market shares in the first phase bidding of China Unicom FDD-LTE master device. In general, the company takes a leading position in domestic 4G market.

Benefiting from the accelerated construction of 4G networks, the period from the second half year till 2015 will be the peak of the capital charges in mainland telecom industry. The company is expected to be the main beneficiary. Recently, China Mobile has increased the goal of 500 thousand 4G base stations by the end of 2014 to 700 thousand, and it is expected to increase to 1 million for the next year. The number of the FDD trial operation cities of China Telecom and China Unicom will increase to 40, the national commercial license is expected to be released within one year, and the numbers of 4G base stations of them are all expected to reach the goal of 300 thousand to 400 thousand. It is also worth mentioning that, the gross profit margin of domestic network equipment sales reaches as high as 45%, therefore, the profitability of the company should be able to maintain stable or even to increase.

In overseas market, the company`s technology is also ahead of that of other international equipment suppliers such as Ericsson, Nokia and Alcatel-Lucent. In the first half of the year, though the overseas income slightly declined by 1.7%, the revenue from the developed markets of Europe and North America has achieved an increase of 10.3%, which highlights the improvement of the company`s competitiveness. Therefore, the company is expected to continue to grasp global market shares and realize the improvement of profitability.

Colorful hotspots in new business

Recently, the notice of centralized procurement of routers and switchboards for the period of 2014-2015 published by China Mobile shows that, ZTE Corporation has for the first time entered in large scale into the high-end router market of China Mobile, ranking No. 2 in market share, while the previous high-end router suppliers such as Cisco and Juniper were out. We believe, the elimination of overseas suppliers indicates that operators are paying more attention to information safety, and it is expected that the domestic high-end router market in future will create the duopoly structure of ZTE and Huawei. In addition, the market has the features of high technology threshold and strong profitability. Therefore, this bidding-winning indicates that ZTE will continue to improve its market share in mainland and its gross margin.

Apart from communication industry, ZTE also positively expands into new areas, and the ZTE new energy car subsidiary has been established in July. On September 17, the company announced that it would cooperate with Dongfeng Motor to start up the world first bus commercial model line that adopts the new energy vehicles high-power wireless charging system in Xiangyang, Hubei Province. At present, the commercially available high-power wireless charging system can be supplied only by three overseas suppliers including Qualcomm and only ZTE in Mainland. The high-power electromagnetic induction wireless charging system has passed the identification of scientific and technological achievements and can realize 90% of charging efficiency under the 30KW high-power system. ZTE has the leading technology globally, and has applied for more than 20 patents.

It is worth noting that, as the wireless charging has many advantages such as convenience, no need for land requisition, safety and reliability, it is hoped to solve the main obstacle of the inconvenience of the charging of electric cars and gain a further wide popularization. So far, ZTE has signed strategic cooperation agreements with many domestic automobile companies (including commercial vehicles and passenger vehicles), and started the loading commissioning of electric vehicles` wireless charging system. At present, in the 40 domestic new energy demonstration cities there is a market volume of more than 400 thousand public buses, and in future the market scale for their wireless charging system is expected to reach hundreds of billions.

Catalyst

The advances of the bidding of China Mobile LTE network;

The national release of commercial FDD-LTE license;

The possibility of diversified ownership reform.

Risks

Slow-down of 4G investment;

Price pressure higher than expected.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()