-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Communications Services Corporation (0552.HK) - “Buy” Rating for Low Valuation

Monday, April 14, 2014  5954

5954

China Communications Services Corporation(552)

| Recommendation | Buy |

| Price on Recommendation Date | $3.710 |

| Target Price | $4.800 |

Weekly Special - 2333 Great Wall Motor

Company Overview

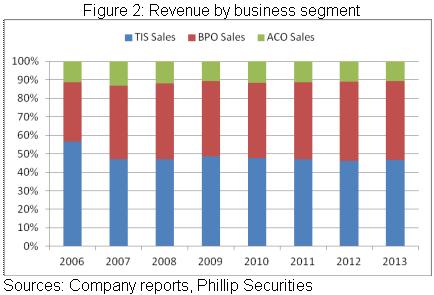

China Communication Services Corporation (CCS) is the leading integrated service supplier in the field of telecommunications, media and technologies. It mainly serves China Telecom, China Mobile, China Unicom and other major clients. The main scope of business covers Telecommunications Infrastructure Services (TIS), Business Process Outsourcing (BPO) services and Application, Content and Other (ACO) services.

Investment Summary

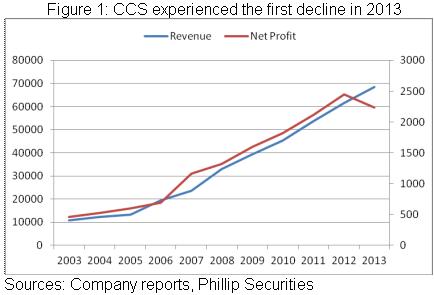

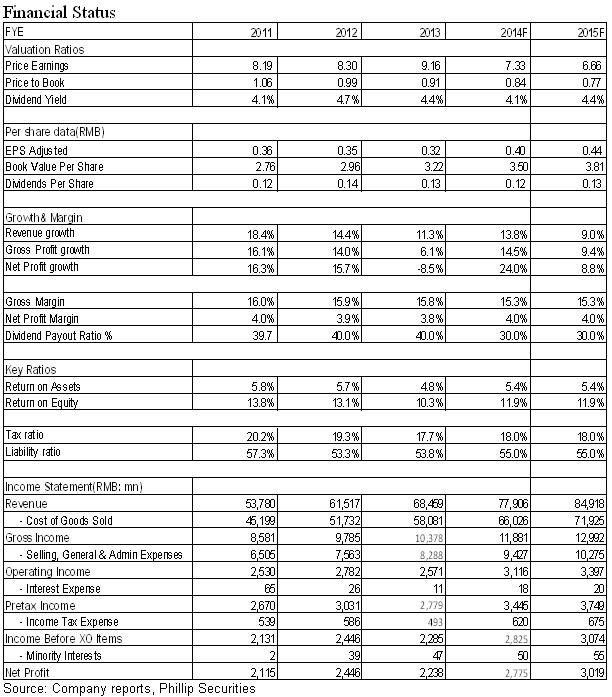

According to 2013 annual report announced by CCS, its revenue in 2013 reached RMB 68.5 billion with a year-on-year growth of 11.3%, but the net profit fell to 2.238 billion yuan with a year-on-year drop of 7%, of which the net profit in the second half of the year dropped 19.6%, the first performance decline for more than a decade since the listing.

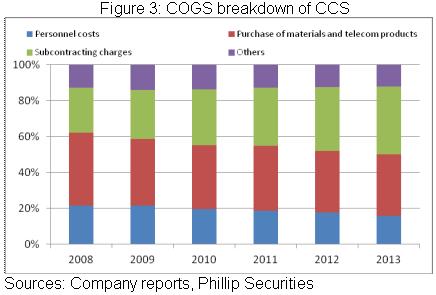

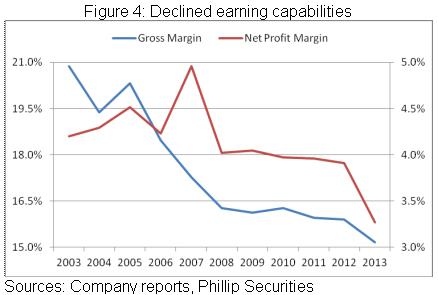

Gross margin of the Company during the period fell by 0.7 percentage points to 15.2% and net profit margin reduced by 0.6 percentage points to 3.3%. Overall speaking, the decline in profitability can be mainly attributed to: firstly, the price pressure resulting from regulatory policies of the telecommunications industry and violent market competition; secondly, the rise of material and subcontracting costs; thirdly, impact from government policies, such as VAT reform; finally, the frontloaded cost for 4G projects preparation, which also affected the profit of the Company.

Although the Company maintained a dividend policy of 40%, namely 0.1296 yuan per share in 2013, the dividend payout ratio will be expected to fall to 30% in 2014, for operators will bear the pressure of 4G capital expenditure with probably a longer payment period and less advance payment under the background of domestic tighter monetary policy.

CCS will be expected to benefit from the 4G network construction and the follow-up requirements of relevant support services. Generally speaking, the three major operators contribute two thirds of revenue to the Company. China Mobile has announced that its capital expenditure increases from 184.9 billion yuan in 2013 to 225.2 billion yuan in 2014 with a growth rate of 21.8%. A great part of China Mobile's capital expenditure in the second half of 2013 was delayed to the first half of 2014. For example, its first batch of 207,000 4G base stations were not completed until March 2014 and only 70,000 ones were completed in 2013.

The Company will face the profitability dilemma continuously in view of the following reasons: first, the price pressure from the operators; second, the probability of rise of manpower cost after the completion of population dividend; in addition, R & D cost of the Company in the 4G era will be expected to rise and the cost of expanding overseas business and marketing will also increase.

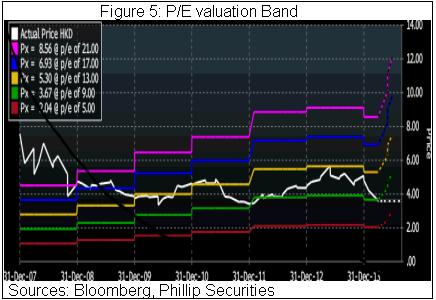

Considering the business re-expansion progress, we even conservatively give it 9.5X valuation, its target price can reach HKD4.8. We grant it "Buy" rating.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()