-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

BYD (1211.HK) - New Platform Is Introduced Again

Friday, July 16, 2021  7792

7792

BYD(1211)

| Recommendation | Accumulate |

| Price on Recommendation Date | $221.000 |

| Target Price | $248.500 |

Weekly Special - 002050 Sanhua

Investment Summary

Sales Volume of Electric Vehicles Hit a Record High in June

According to data, BYD sold 51,015 vehicles in June, up 51% yoy and up 10% mom. Specifically, 41,366 new energy vehicles were sold, up 192% yoy and up 26% mom, and 9,649 traditional fuel vehicles were sold, down 50.6% yoy and down 28.5% mom. The sales volume of new energy vehicles hit the Company's record high, exceeding the sales volume of new energy vehicles of rivals Tesla and SGM-Wuling in China. Passenger vehicles and commercial vehicles made a contribution of 49,765 units and 1,250 units, respectively. In H1, the Company sold 246,700 vehicles accumulatively, up 55.5% yoy.

In terms of the sales volume of new energy passenger vehicles in June, the sales volume of EVs reached 20,016 units, up 102% yoy and up 7% mom, and that of HEVs reached 20,100 units, up 537% yoy and up 55% mom. Benefited from the whopping sales figures of DM-i models, HEVs have displayed an outstanding performance.

BYD's three new DM-i models (Qin PLUS DM-i, Song PLUS DM-i, and Tang DM-i) have been launched successively since March this year. They are equipped with the self-developed "DM-i super plug-in hybrid" system, which are highly competitive. In June, the total sales volume of the three new DM-i models was expected to be approximately 17,000 units, with the cumulative order exceeding 120,000 units. Limited by the bottleneck of the blade battery production capacity, the supply exceeded the demand for the products. The average delivery cycle took approximately three months. In H2, Qin Pro DMi, Song Pro DMi, and Han DMi will also be launched. As the blade battery production capacity increases, the sales volume of DM-i series models is expected to continue to grow.

In addition, as BYD's first e platform 3.0-based model, Dolphin will be launched in the third quarter. It targets younger customers, aiming to fully tap the entry-level electric vehicles and travel markets.

Semiconductor's Spin-off Listing Activates a New Round of Positive Feedback Mechanism for Capital and Company Value

Recently, BYD's proposal to spin off its semiconductor business and to list it on the A-share GEM has been accepted, officially opening the way for multiple businesses to obtain value revaluation through the capital market. We believe that with the acceleration of the neutralization strategy, the spin-off listing of other sectors such as blade batteries, commercial vehicles, and photovoltaic energy storage may be successively achieved in the future. The improvement in operational efficiency and value reshaping brought about by the spin-off will push up the Company's potential value. The Company is expected to fully benefit from the dividend of the positive feedback mechanism for capital and company value.

Investment Thesis

Therefore, although there are various challenges in the future, we believe that the Company is entering into a growth period with more stability and sustainability.

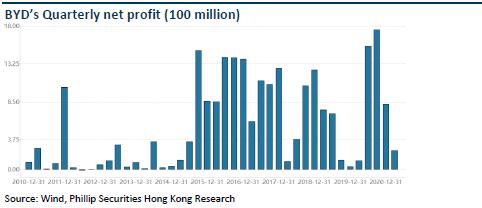

In terms of STOP valuation adopt, we give the original business (automobile, mobile phone, rechargeable battery and photovoltaic business) 138/84 HK$/per share, power battery business and semiconductor business from two assumptions of optimistic expectation and cautious expectation. 176/90 and 12/4.4 HK$/per share, the overall valuation is respectively 321/176 HK$/per share, implying 45% and -20% upside respectively. For comprehensive consideration, we given the target price of 248.5 HK$, corresponding to 2021/2022/2023 110/83/60x P/E, 7.6/7.0/6.3x P/B, Accumulate rating.

(Closing price as at 14 July)

Risk

Sales of NEVs is not as good as expected

New business risk

Slow-down of Hand-set components business

Financials

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

E-Check

Login

![]()

![]()

![]()

![]()