-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Desay SV (002920 CH) - Deepening Deployment in Automotive Intelligence

Tuesday, March 31, 2026  2795

2795

Desay SV(2920)

| Recommendation | Accumulate (Downgrade) |

| Price on Recommendation Date | $105.000 |

| Target Price | $121.000 |

Weekly Special - 2333 Great Wall Motor

Company Profile

Desay SV, established in 1986, is a leading company in the automotive electronics field, with its main products including intelligent cockpits, intelligent driving, and connected services.

Investment Summary

Sequential Improvement in Q4, Full-Year Results Up by Over 20%

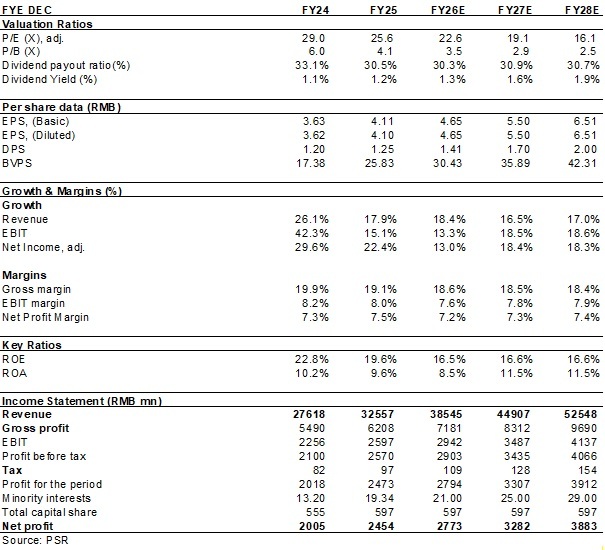

In 2025, the Company reported revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB32,557 million/RMB2,454 million/RMB2,414 million (RMB, the same below), respectively, up 17.88%/22.38%/24.05% yoy. Gross margin was 19.07%, down 0.81 ppts yoy. Net cash flow generated from operating activities reached RMB2.88 billion, up +93.1% yoy. In 2025 Q4, the Company reported quarterly revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB10,221 million/RMB666 million/RMB690 million, respectively, up 18.25%/11.34%/38.71% yoy and 32.87%/17.82%/20.72% qoq. The sequential recovery in Q4 results was mainly driven by qoq growth in sales volume from key customers such as Geely, Xiaomi and Li Auto.

Deepening Deployment in Automotive Intelligence

Benefiting from the continued increase in penetration of automotive intelligent products and the significant rise in intelligent value per vehicle, the core business segments achieved strong growth in results. 1) Smart cockpit: Full-year revenue reached RMB20,585 million. Annualised sales of new project orders exceeded RMB20 billion. The Company continued to secure new project orders from major domestic and international OEMs, including Chery Automobile, Geely Auto, GAC Toyota, Li Auto, Great Wall Motor, Xiaomi Auto, XPeng Motors, Changan Automobile, VOLKSWAGEN, MERCEDES-BENZ and SKODA. 2) Intelligent driving: Full-year revenue reached RMB9.7 billion, up 32.63% yoy. Annualised sales of new project orders exceeded RMB13 billion. With the rapid adoption of intelligent driving technologies, the accelerated commercialisation of advanced functions such as urban NOA is expected to further drive high-speed growth in the Company's intelligent driving business. 3) Connected services: The Company's self-developed "Blue Whale" ecosystem achieved major breakthroughs during the reporting period. Based on AIOS, the Company comprehensively upgraded the cockpit intelligent software foundation, enabling full-stack decoupling of software and hardware and flexible adaptation across different hardware platforms and large models. It possesses full-stack AI capabilities ranging from large-model algorithms and AIOS middleware to Agent development, providing a robust full-stack software solution for the development of the AI cockpit software ecosystem.

Focus on R&D, Expansion into Innovative Businesses

The Company has consistently maintained a high level of R&D investment. In 2025, R&D expenditure reached RMB2,637 million, accounting for 8.10% of revenue. R&D personnel represented 42.40% of the Company's total workforce. The Company has established R&D centres in Singapore, Germany, Japan, and across China in Nanjing, Chengdu, Shanghai, Shenzhen, Guangzhou, Beijing, Taiwan and Changsha, ensuring sustained technological leadership and a leading position in the industry.

In terms of innovative businesses, the Company officially launched the "Chuanxing Zhiyuan" low-speed autonomous vehicle brand, expanding into a new track in last-mile logistics. Meanwhile, the Company continues to deepen industrial synergy in frontier intelligent fields, advancing in-depth cooperation and implementation with multiple embodied intelligence enterprises. It has also successfully secured designated orders for robot domain controller projects, with related products planned to achieve mass production and delivery in 2026.

Steady Progress in Internationalisation Strategy

In 2025, the Company's overseas revenue increased by 41.12% to RMB2.41 billion, with its contribution rising to 7.40%, up 1.22 ppts yoy. The gross margin of overseas business was higher than that of the domestic market. In 2025, overseas gross margin reached 27.28%, up 1.34 ppts yoy and approximately 9 ppts higher than the domestic gross margin in the same period. As the internationalisation strategy continues to advance steadily, the Mexico and Indonesia plants commenced operations in 2025, while the Spain plant is expected to begin operations this year. The expansion of overseas production capacity will provide strong support for profit growth.

Investment Thesis

The Company is a leader in the automotive electronics sector. Benefiting from ongoing industry development and sustained R&D investment, it maintains a technological leadership advantage while actively exploring new business opportunities. We remain firmly optimistic about the Company's long-term development prospects.

As for valuation, we expected diluted EPS of the Company to RMB 4.65/5.50/6.51 of 2026/2027/2028. And we accordingly gave the target price to RMB121, respectively 26/22/19x P/E for 2026/2027/2028. "Accumulate" rating. (Closing price as at 30 December 2026)

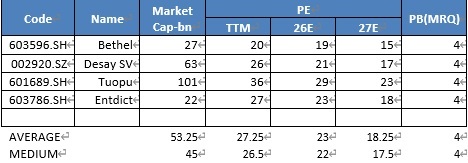

Peer Comparison

Source: Wind, Phillip Securities Hong Kong Research

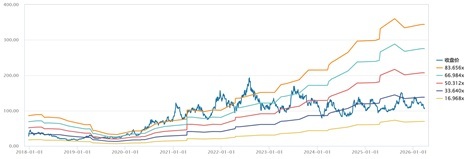

PE BAND

Source: Wind, Phillip Securities Hong Kong Research

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

(Closing price as at 30 March 2026)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()