-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

陶然女士 (Megan Tao)

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

| Phone: | 22776515 | Email: | megantao@phillip.com.hk | |

Pop Mart (09992.HK) - Labubu Drives Explosive Growth in Overseas Markets

Tuesday, August 12, 2025  936

936

POP MART(9992)

| Recommendation | Accumulate |

| Price on Recommendation Date | $278.800 |

| Target Price | $316.000 |

Weekly Special - 358 JIANGXI COPPER

Company Background

POP MART is a leading Chinese trend culture entertainment company, founded in 2010 and headquartered in Beijing. Centered around designer toys, the company has built an integrated operation platform spanning the entire industry chain—covering IP incubation and operation, trendy toy retail, theme parks and experiences, and digital entertainment. POP MART boasts a portfolio of popular IP characters such as Molly, DIMOO, and SKULLPANDA, distributing products through both online and offline channels with a strong following among young consumers.

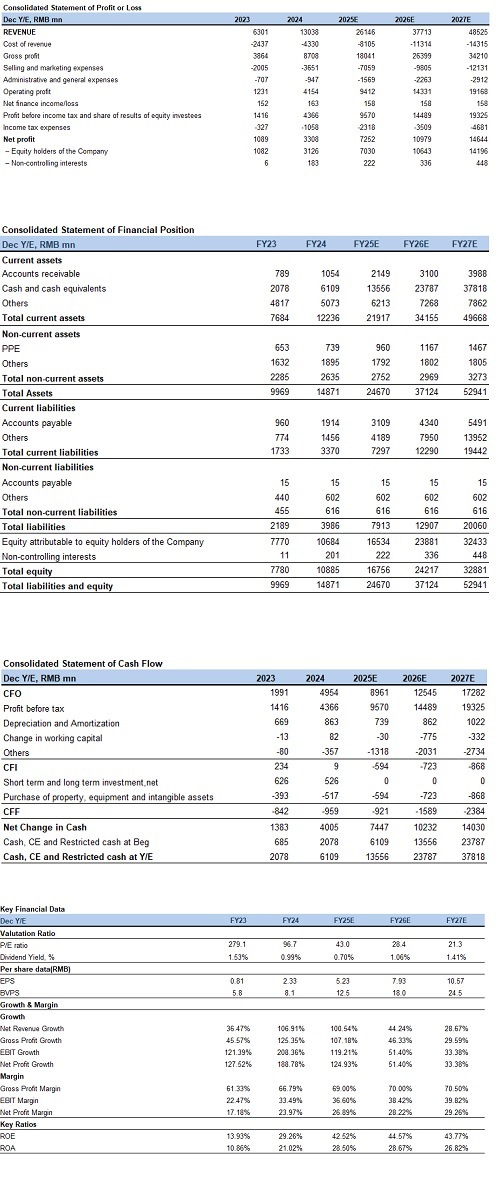

Financial Performance

In 2024, the company achieved total revenue of RMB 13.0 billion, representing a 106.9% year-over-year increase. Operating profit surged 237.6% to RMB 4.2 billion, while net profit attributable to shareholders rose 188.8% to RMB 3.1 billion. Gross profit margin expanded by 5.5 percentage points to 66.8%, primarily driven by optimized product mix and higher contribution from overseas high-margin businesses. Geographically, mainland China revenue grew 52.3% to RMB 8.0 billion, with retail stores (RMB 3.8 billion, +43.8%), online sales (RMB 2.7 billion, +76.9%), and robot stores (RMB 700 million, +26.4%) all posting strong growth. Revenue from Hong Kong, Macau, Taiwan and overseas markets soared 375.2% to RMB 5.1 billion, fueled by explosive expansion in retail stores (RMB 2.9 billion, +404.0%) and online channels (RMB 1.5 billion, +834.0%).

For the first half of 2025, the company projects revenue growth of no less than 200.0% (implying RMB 13.7 billion) and operating profit growth exceeding 350.0% (RMB 4.3 billion), with net profit margin expected to surpass 30.0%, a historical high. This accelerated performance stems from heightened recognition of the company's IP portfolio, increasing overseas revenue contribution, and sustained cost optimization efforts.

Core New IP Launches Propel Explosive Overseas Growth

Following the market frenzy driven by its Monster series in Q4 2024, POP MART launched the Labubu 3.0 designer toy series in April 2025. Throughout Q2, Labubu 3.0 continued fueling explosive overseas growth—maintaining Q1's 475%-480% YoY surge—as celebrity endorsements and social media buzz amplified IP popularity, sustaining rapid international revenue expansion. In Q1 2025, North American sales skyrocketed nearly ninefold (895%-900% YoY), while European revenue jumped over sixfold (600%-605% YoY), significantly outpacing Southeast Asia's 345%-350% growth. This validates the company's Western-focused strategy, with management projecting North American sales to match 2020 group-wide levels (RMB 2.5 billion) by year-end. Despite implementing 12%-27% price hikes in North America since mid-April 2025 to offset tariffs, sales momentum remains robust, demonstrating both low consumer price sensitivity and strong pricing power. We believe rising contributions from premium-priced overseas markets will further enhance overall profitability.

Accelerated Offline Store Expansion

On physical retail expansion, 39 new stores opened in H1 2025, with the US (17 stores), Indonesia (6), and Thailand (5) leading the rollout—accelerating POP MART's strategic shift toward offline growth.

Strong Online Channel Performance

Digitally, FastMoss data shows TikTok channel GMV reached RMB 498 million in H1 2025, dominated by the US (RMB 336 million), Thailand (RMB 67 million), and Philippines (RMB 29 million).

Overseas Success Fuels Domestic Growth Acceleration

Leveraging the global buzz around Labubu 3.0, we project POP MART's domestic sales growth will further accelerate from May-June 2025 (versus April levels), driving Q2 China revenue growth to outpace Q1 (+95%-100% YoY).

Investment Recommendation

While POP MART's flagship IPs typically experience short-term spikes (~2 years) followed by deceleration, we believe the company's integrated operational capabilities—spanning channel management, content development, and product innovation—can sustain value release during IP traffic peaks, transforming "blockbusters" into enduring icons. As a pioneer and leader in trendsetting toys and commercialization, the company leverages its full-industry-chain advantages to develop and monetize IPs across multiple dimensions. Its product category expansion has shown significant results, while overseas business has entered a new phase of accelerated growth. Accordingly, we forecast the company's 2025-2027 revenue at RMB 26.1/37.7/48.5 billion, with net profit attributable to shareholders at RMB 7.0/10.6/14.2 billion, translating to EPS of RMB 5.23/7.93/10.57. Given its high growth potential, we apply a 55x P/E multiple to our 2025 earnings estimate, arriving at a target price of HKD 316. The current share price implies 2025-2027 P/E multiples of 48x/32x/24x, and we assign an "Accumulate" rating.

Risk Factors

1) Intensifying competition;

2) Slower-than-expected overseas expansion;

3) Deteriorated market demand.

Financial Data

(Closing price as of: Aug 7)

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()