-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Foryou Group (002906.CH) - Second Growth Curve Gradually Becoming Clear

Monday, June 15, 2026  1407

1407

Foryou Group(2906)

Weekly Special - 002050 Sanhua

Company profile

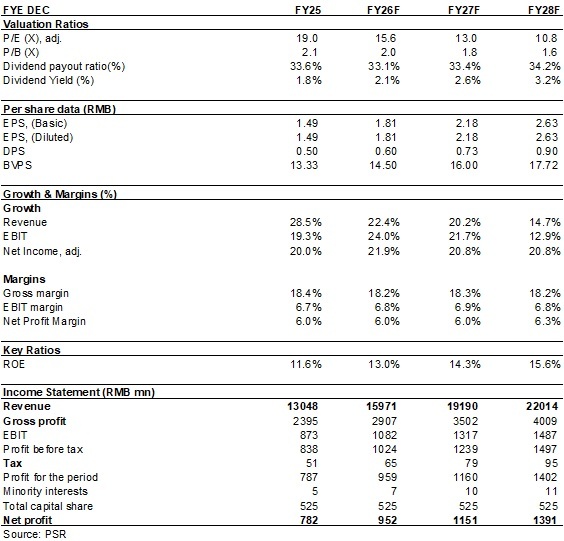

Foryou Corporation was established in 1993 and is mainly engaged in the R&D, production and sales of automotive electronics and precision die-casting businesses. The Company's automotive electronics business mainly covers two core sectors, namely smart cockpit and advanced driver-assistance systems. Its precision die-casting business is centred on precision mould design and manufacturing technology, covering aluminium alloy, magnesium alloy and zinc alloy product lines. In addition, it actively explores and develops AI, robotics and other related businesses, including optical communication modules, AI high-speed connectors, robotics and other related component businesses. In 2025, the Company reported revenue of RMB13,048 million, up 28.46% yoy; net profit attributable to the parent company was RMB782 million, up 20.00% yoy.

Investment Summary

Q1 Revenue Maintained High Growth

In Q1 2026, the Company reported revenue/net profit attributable to the parent company/net profit excluding non-recurring items of RMB3,096 million/RMB166 million/RMB159 million, respectively (RMB, the same below), up 24.37%/6.61%/5.89% yoy, respectively. Gross margin was 16.5%, down 1.7 ppts yoy. The slower profit growth compared with revenue growth was mainly due to factors such as price competition and rising raw material prices. The Company has established a raw material price linkage mechanism with most of its customers, and its operating results are expected to improve significantly from Q2.

Automotive Electronics Business Continued to Grow, With Its Leading Position in Smart Cockpit Firmly Established

The Company's automotive electronics business reported revenue of RMB9,675 million in 2025, up 27.25% yoy, accounting for 74.15% of total revenue. CAGR reached 35.66% from 2020 to 2025, maintaining high-quality growth. The Company has built a comprehensive product matrix and solution capabilities in the smart cockpit field. The market shares of HUD, in-vehicle wireless charging and other products continued to rank first in China, while the market shares of LCD instrument panels and central control screens rapidly rose to the forefront of the industry.

The Company's customer structure continued to optimise, with a low dependence on any single customer, and the revenue contribution from some new energy vehicle makers and international automotive brands increased. Revenue from customers including Changan, BAIC, Xiaomi, Dongfeng, STELLANTIS, SAIC Volkswagen, BYD, Xpeng, NIO and Leapmotor increased significantly. Leveraging the ADAYO Automotive Open Platform (AAOP), the Company provides customers with "one-stop" overall smart cockpit solutions based on its implementation capabilities in cockpit domain controllers across multiple platforms including Qualcomm, SemiDrive and MediaTek, as well as mainstream large models, demonstrating significant platform-based competitive advantages.

Precision Die-Casting Business Improved Its Process Technologies, Enhancing Overall Competitiveness

The Company overcame a number of difficult technical challenges in mould design and manufacturing, expanded the application of highly flame-retardant magnesium alloy materials, and promoted the deep integration of 3D vision guidance with AI and robotics to improve the flexible changeover capability of automated manufacturing cells. Its capabilities in complex and difficult production processes, including high-vacuum combined extrusion, friction stir welding of aluminium-magnesium alloys, profiling spraying, multi-spindle machining and vacuum adsorption, continued to improve. The precision die-casting business delivered particularly impressive performance in 2025, reporting revenue of RMB2,859 million, up 38.47% yoy, with growth exceeding that of the automotive electronics business. CAGR reached 35.08% from 2020 to 2025.

Second Growth Curve Gradually Becoming Clear, with Capacity Expansion Releasing Growth Momentum

The Company actively explores non-automotive businesses such as AI and robotics:

1) In the AI infrastructure field, optical communication modules, high-speed connectors and data centre cooling system components have secured project nominations;

2) In the robotics field, the Company has received orders for robotics display screens and joint module components, and jointly developed robotics main and auxiliary controllers, with brand momentum surging and sales increasing exponentially.

Following a record-high scale of capacity construction in 2025, capital expenditure is expected to remain at a high level in 2026, focusing on the Thailand Production Base, the expansion of the Automotive Electronics Huizhou Base, the expansion of the zinc alloy die-casting business in the AI field, and Phase III of the Precision Die-Casting Changxing Project. Capacity expansion is being carried out based on orders on hand, providing solid support for sustained business growth going forward. Among them, the Thailand Production Base is expected to commence production in Q4 2026, providing strong support for overseas business expansion.

Investment Thesis

The Company's traditional automotive business is growing steadily and rapidly, while its non-automotive business offers enormous growth potential. We are optimistic about the long-term development of the Company and expect EPS to be 1.81/2.18/2.63 yuan respectively for 2026/2027/2028, a yoy increase of 22%/21%/21%. We offer a target price of 36.3 yuan, respectively 20/16.6/13.8x P/E for 2026/2027/2028, and an "Buy" rating. (Closing price as at 5 June)

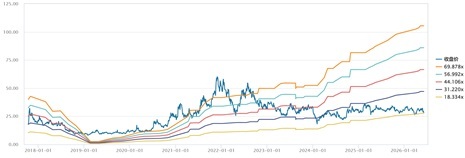

Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

(Closing price as at 5 June)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()