-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Feilong Auto (002536 CH) - Short-term fluctuations do not alter long-term trends

Friday, October 31, 2025  672

672

Feilong Auto(2536)

| Recommendation | Neutral (Downgrade) |

| Price on Recommendation Date | $22.400 |

| Target Price | $23.200 |

Weekly Special - 3750 CATL

Investment Summary

Stable Q3 Results with Continued Improvement in Gross Margin

According to the recently released Q3 2025 report, the Company recorded revenue of RMB32.37 million (RMB, the same below) for the first three quarters, down 7.38% yoy. Net profit attributable to the parent company reached RMB287 million, up 7.54% yoy, and net profit attributable to the parent company excluding non-recurring items was RMB304 million, up 16.66% yoy.

Operating costs for the first three quarters dropped 12.78% yoy to RMB24.03 million, a steeper decline than the drop in revenue, mainly driven by optimisation of product mix and cost control. This contributed to a 4.6 ppts increase in gross margin to 25.8%. The overall period expense ratio rose by 2.06 ppts to 14.94%, with the selling expense ratio up 0.64 ppts yoy and the administration expenses ratio up 1.11 ppts yoy. Financial expenses decreased by 31.2% yoy, benefiting from increased exchange gains. The R&D expense ratio rose slightly by 0.55 ppts to 6.7%. Asset impairment losses narrowed by 38.1% yoy, mainly due to a reduction in provision for inventory write-down. Profit growth was primarily driven by continued cost optimisation, partly offset by the rise in period expense ratio. Net profit margin attributable to the parent company increased by 1.23 ppts yoy to 8.86%.

Looking at the quarterly data, Q3 revenue was RMB10.76 million, down 4.68% yoy. Net profit attributable to the parent company was RMB76,301.6 thousand, down 7.9% yoy. Net profit attributable to the parent company excluding non-recurring items was RMB86 million, up 0.38% yoy. Compared to Q2, revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items were up 2.28%, down 13.09%, down 9.34% qoq, respectively. Profitability continued to improve in Q3, with gross margin up 0.84 ppts yoy to 26.28%. The period expense ratio rose slightly by 0.45 ppts yoy, and operating profit margin increased by 1 ppt yoy to 8.9%. However, a sharp increase in non-operating expenses due to losses on disposal of fixed assets, along with a higher effective tax rate, significantly impacted profitability, resulting in a 0.25 ppts yoy decline in net profit margin attributable to the parent company to 7.09%.

Overseas Business and Capacity Adjustment

In terms of market layout, the Company continues to deepen its presence in the domestic market while enhancing its share in international markets through optimisation of overseas channels. The increase in exchange gains indirectly reflects the scale of overseas business settlements. Notably, construction in progress at the end of the reporting period decreased by 50.21% compared with the beginning of the period, mainly due to the transfer of Longtai Auto Parts's project to fixed assets, suggesting that capacity restructuring may provide support for future market expansion.

Breakthrough in Liquid Cooling Technology and Entry into the Humanoid Robot Supply Chain

During the period, the Company achieved significant technological breakthroughs. Its liquid cooling pipeline system gained strong market recognition driven by surging AI computing power demand, further reinforcing its leading technological advantage. The Company successfully introduced its joint module into the supply chain of humanoid robots, marking a substantive advancement in the application of thermal management technology in frontier industries. In addition, the Company continues to promote the integration of its thermal management technology with emerging fields such as robotics, accelerating its deployment in the humanoid robot market and striving to establish a long-term growth engine aimed at fostering new productive forces.

Investment Thesis

With the rising penetration of new energy vehicles and increasing demand for liquid-cooled servers, the Company's dual-track strategy of "automotive + general industrial" is expected to continue unlocking result potential. The increase in expense ratio during the market development phase, does not undermine its long-term growth potential.

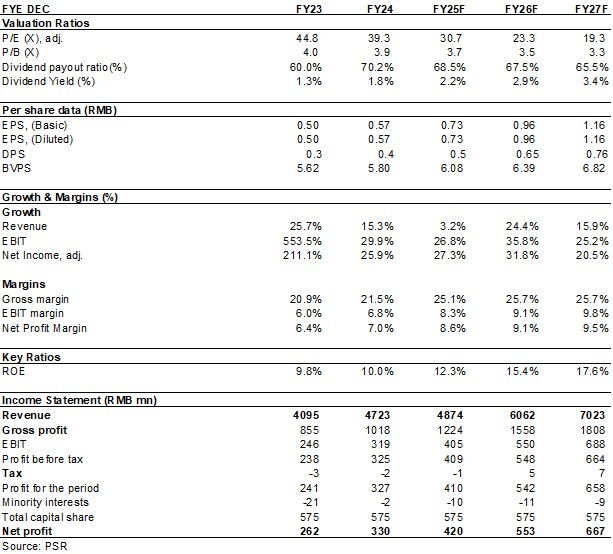

As for valuation, we revised diluted EPS of the Company to RMB 0.73/0.96/1.16 of 2025/2026/2027. And we accordingly gave the target price to RMB23.2, respectively 31.8/24.1/20x P/E for 2025/2026/2027. "Neutral" rating. (Closing price as at 30 October)

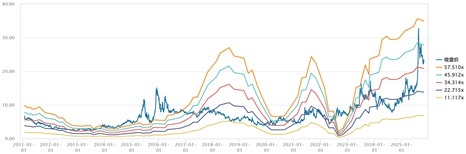

Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research

Risk

1) Progress of new production line is below expectations;

2) Electric vehicle sales fall short of expectations;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices.

Financials

(Closing price as at 30 October 2025)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()