-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Trigiant Group (1300.HK) - “Buy” rating for underestimated value

Monday, April 28, 2014  2546

2546

Trigiant Group(1300)

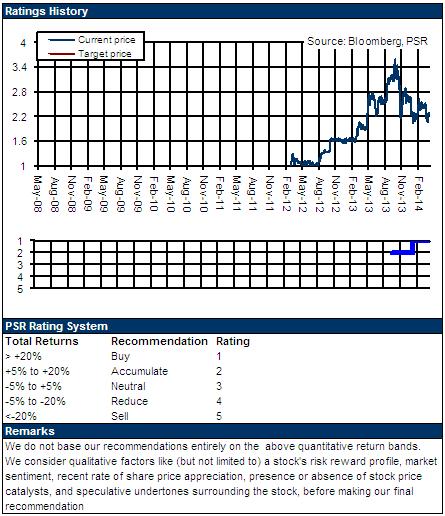

| Recommendation | Buy |

| Price on Recommendation Date | $2.430 |

| Target Price | $3.000 |

Weekly Special - 002050 Sanhua

Company Overview

Founded in 2007, Trigiant is a leading domestic vendor engaged in production of RF coaxial cable. It ranks the first place in sales volume of RF cable products with the market share of 25%. So far, the company's products have been extensively applied in telecom operators, service suppliers, and main equipment manufacturers` transmission systems. In addition to selling products to its main customers like domestic three major telecom operators and telecom equipment vendors (including ZTE and Huawei), the company also exports its products to overseas market.

Investment Summary

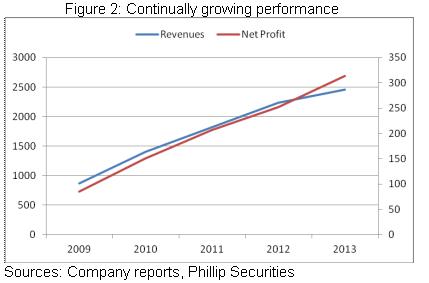

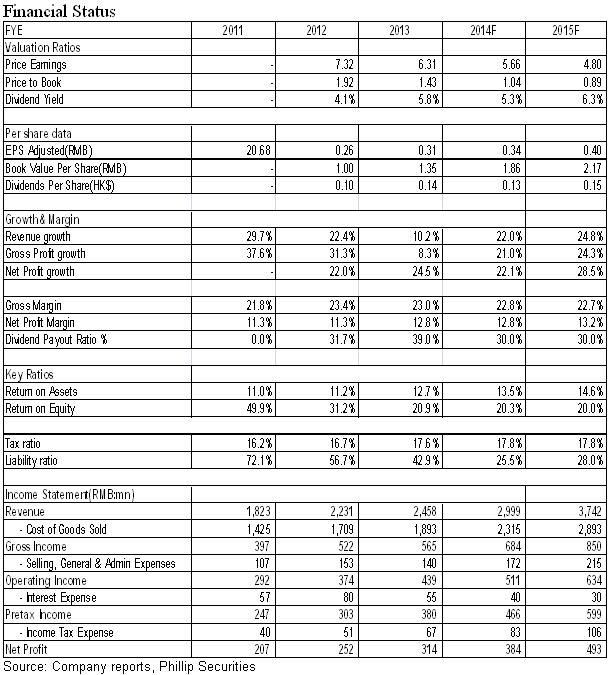

According to the financial statement of 2013, Trigiant achieved RMB 2.46 billion yuan (the same below) of turnover with 10.2% growth rate , and its net profit increased 24.3% to 0.31 billion yuan, converting into EPS of 0.31 yuan. It also declared dividend per share of HK$0.14 for 2013 with the dividend payout ratio of 39%.

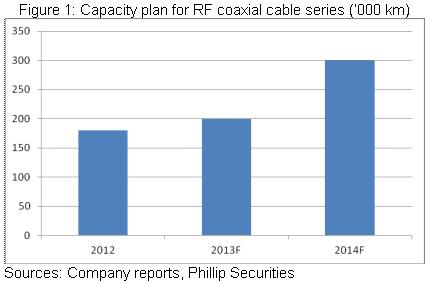

Turnover expanding gently is mainly because the licensing of 4G was later than expected, and the sales volume of radio-frequency coaxial cable was about 128 thousand kilometers, an increase by 11.5% on year-on-year basis. Meanwhile, the average price of copper, the main raw material, decreased by 6.8%, and the pricing of the company was cost-plus mode. In addition, in order to expand the market share, the company also strategically decreased the order price of flame-retardant flexible cables.

The net profit growth greatly exceeded the gross profit, which mainly benefited from the effective cost management and the decrease of financing cost. Although the R&D cost greatly increased by about 65.5% due to 4G network construction, the Group implemented internal cost management to make the sales cost and distribution cost decrease by about 12.4%. In addition, with the benefits from share allotment financing, the financing cost also greatly decreased by 31.2%. Finally, the net profit margin increased by 1.5 percent points to 12.8%.

The radio-frequency coaxial cable, the core product of the company, is the essential component to transport mobile signals in the base stations, and the optical cables can`t be replaced. It is worth mentioning that every 2G and 3G base station requires using about 0.5 kilometer of cables, while every 4G base station requires using at least 0.5 kilometer of cables, even 0.6 kilometer of cables. Therefore, 4G investment speeding up will bring practical demand expansion to the company. Currently, 40% of radio-frequency coaxial cables are used in base station construction.

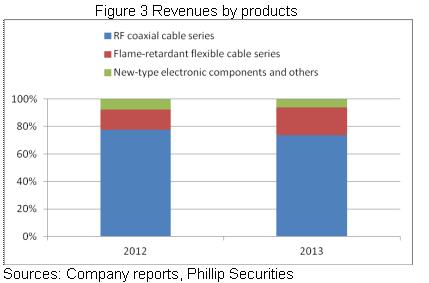

In addition, the main clients of the company's flame-retardant flexible cables business are China Unicom and China Telecom, respectively accounting for 80% and 20% of the sales proportion of the company. In 2014, the company expects to introduce China Mobile to be the downstream customer of this business, and it is likely to further promote the growth certainty of this business. In 2013, the turnover of flame-retardant flexible cables business greatly increased by 58%, which was far higher than radio-frequency coaxial cables (4%), and increased by 6.1 percent points to 20.4% of the total revenue.

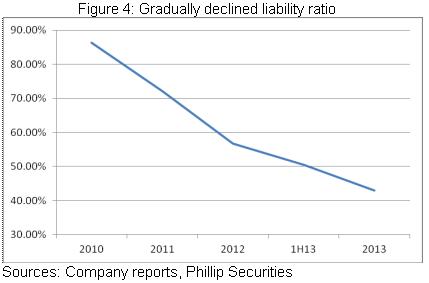

After the last allotment, the asset-liability ratio of the company decreased by 8 percent points. If 0.2 billion warrant shares allotment accomplishes successfully this time, the asset-liability ratio is expected to decrease by over 15 percent points again and the capital structure will be improved obviously. Meanwhile, the finance burden will also fall off obviously.

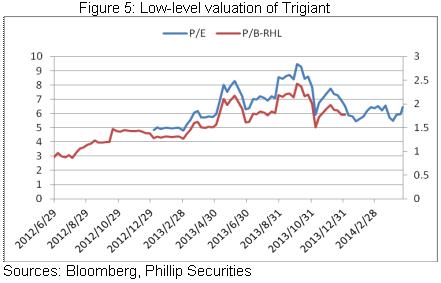

Currently the valuation of the company is just about 6-7 times compared with EPS of 2013, which doesn`t correspond with its growth. Even we assume that the PE ratio valuation is 7 times that of EPS in 2014, the target price can reach 3 HKD , which is "Buy" rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()