-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Navinfo (002405.CH) - Expected to return to a rapid growth track

Friday, March 31, 2017  23877

23877

Navinfo

| Recommendation | Buy |

| Price on Recommendation Date | $19.790 |

| Target Price | $24.750 |

Weekly Special - 002050 Sanhua

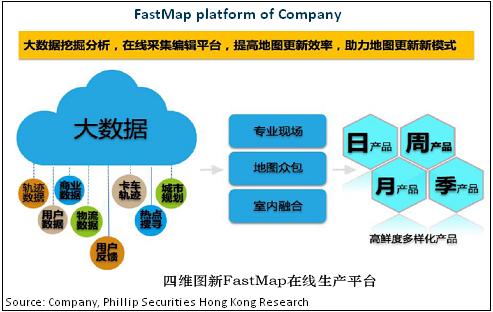

Company profile: Leading electronic map supplier in China

Established in 2002, Beijing NavInfo Co., Ltd. (hereinafter referred to NavInfo or "the company") is a leading supplier providing navigation maps and dynamic traffic information services in China. Founded by National Administration of Surveying, Mapping and Geoinformation, it is the only national company specialized in surveying and mapping affiliated to China Aerospace Science and Technology Corporation. It was listed on Shenzhen Stock Exchange in 2010. At present, the main business of NavInfo includes two categories: sale of electronic navigation maps and system technical services. NavInfo has maintained a good strategic cooperative relationship with important internet customers and clients. In the pre-installed navigation market, NavInfo's customers include a large number of international mainstream car manufacturers, such as BMW, Mercedes Benz, GM, Tesla. In China, all of the navigation maps of Tesla are provided by NavInfo. In the field of internet enterprises, Tencent, Baidu, Sogou are the important partners of NavInfo.

Significant leading role in China's pre-installed vehicle navigation

NavInfo is the China's largest, the world's third largest electronic navigation map manufacturer, and leads the market in the field of pre-installed vehicle navigation maps For eight consecutive years, the company has accounted for over 60% of the share in the vehicle navigation map market and has taken up over 50% of the share in the mobile navigation map market for four consecutive years. The company has built a nationwide navigation electronic map database and the country's largest production and update network system of navigation electronic maps. Nowadays, there are 35 field bases established in China, including 600 field collectors and 100 field operating vehicles. We have the ability of updating the data services four times annually in major cities and two times in secondary major cities.

Threshold of qualification builds the moat

NavInfo is the first company qualified for the production of navigation maps (since 2001). Presently, there are only 13 qualified suppliers in China. Because map data involves national secrets, we expect that the high threshold will continue to build a deep moat for the company.

Promote a new round of industrial chain layout. Conform to the trend of emerging industry development

In the consolidation of the existing electronic map business, the company makes vertical integration to the vehicular networking, automatic driving and other future fields, exploring business model innovation and new profit growth points actively based on our own technologies and resource advantages. In recent years, relying on the capital market, the company has increased the research and development in innovative business types and carried out a series of asset acquisitions in industry chain. In 2011, the company acquired Mapscape of Netherlands, the company obtained NDS compiler technology. Acquiring China Trans Geomatics Co., LTD., the company expanded to traffic mapping and vehicle networking. In 2013, the company cooperated with Sinomach Automobile, and become the controlling shareholder of Zhonghuan Satellite, expanding to the field of commercial vehicle networking. In 2014, holding hands with Tencent, the company put forward the whole vehicle solutions WeDrive, and launched a series of products, building a vehicle networking application ecosystem. In 2015, the company perfected the vehicle networking business group with the acquisitions of Mapbar and SmartAuto. And the cooperation with Didi Taxi brought us high quality floating car database. In 2016, we cooperated with Yanfeng Visteon, NextEV, WM Motor and JD Finance in the fields of vehicle networking, autonomous vehicles, automotive financial services, etc. The company acquired, in 2016, 100% equity of AutoChips Inc., an auto-chip manufacturer, of MediaTek, with RMB3.9 billion, becoming a player in a key aspect of vehicular networking.

Performance is expected to recover steadily

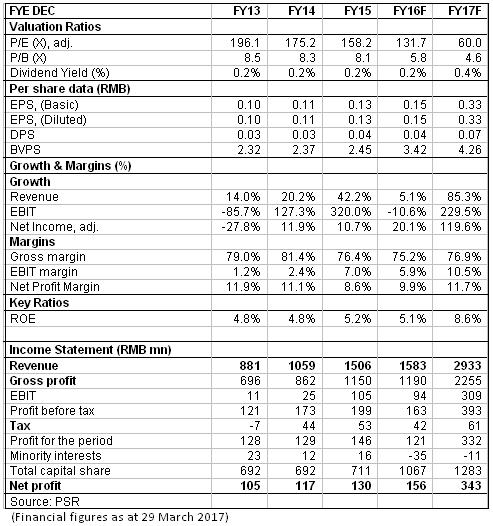

Since the company was listed in 2010, its performance saw a fall after initial improvement, and then once again witnessed a tread of steady recovery. The main reason for the low profit in 2013 was the unexpected fall in sales in Nokia mobile phones, the company's largest user in the field of mobile phone electronic map. As a result, the net profit in 2013 only recorded RMB105 million, down 27% yoy. However, with the continued efforts to expand its car electronic map, car networking and compilation service business, the company's profit rose again after bottoming out and the compound annual growth rate from 2014 to 2016 was approx. 18%. Taking up over 60% market share in the automotive IVI chip market, the leading acquired AutoChips promised to achieve a net profit of RMB187 million, RMB228 million and RMB303 million in 2016, 2017 and 2018 respectively. We expect a bright future for NavInfo after new business integration and its performance is expected to return to a rapid growth track.

Increasingly flexible and efficient corporate governance structure

In order to meet the challenges brought by the ever-changing scientific and technological innovation competition and build a more flexible and efficient corporate governance mechanism, NavInfo in recent years have made several reforms in its state-owned enterprise structure, including promoting mixed ownership, equity incentives, employee holdings and so on. In 2014, the company introduced the Tencent industry fund as a strategic investor with 9.74% stake of the company, turning the company from a state-owned and state-controlled company to a state-owned holding company without actual controller. In 2015, the company implemented its equity incentive plan, with 2.57% of the total equity for 482 management and core technology staff. At the beginning of 2017, the company subscribed 40,000 shares for executives and core staff in its plan for fixed asset acquisition. The company's general manager has 14.8% of the voting rights of the company, more than the largest shareholder, which helps to establish a more flexible and efficient decision-making management system and core talent incentive mechanism.

Valuation

As analyzed above, we expected diluted EPS of the Company to RMB 0.15 and 0.33 of 2016/2017. And we accordingly gave the target price to 24.75, respectively 75x P/E for 2017. "Buy" rating. (Closing price as at 29 March 2017)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()