-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Tianyi Holdings Ltd (756.HK) - Stable profit growth with the strong profitability

Wednesday, May 7, 2014  4818

4818

China Tianyi Holdings Ltd(756)

| Recommendation | Buy |

| Price on Recommendation Date | $1.100 |

| Target Price | $1.450 |

Weekly Special - 002050 Sanhua

Company Introduction

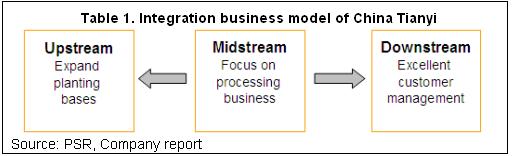

China Tianyi (or “the Group”) is the first domestic agricultural products manufacturer and grower listed in H Shares, which is principally engaged in processing and selling of frozen concentrated orange juice (“FCOJ”) and the related products. The Group becomes the leader in the market with 19 years of experience in the concentrated juice processing industry, and has established as well as invested in production plants in the three major citrus growing areas of Chongqing, Hunan and Fujian. It has also set up its own orange cultivation bases of tens of thousands Mu in aggregate. The Group has been supplying raw material to large beverage products manufacturers, including Coca-Cola in China, Japan-based Suntory and Wahaha in recent years, and also exports its products to the UK and the Asian region.

Summary

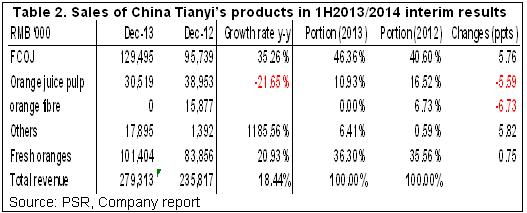

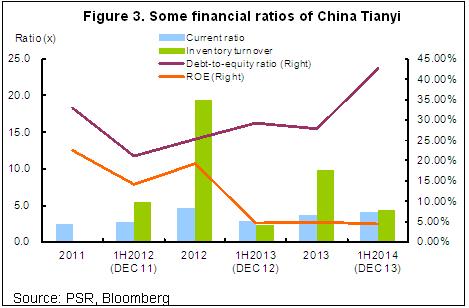

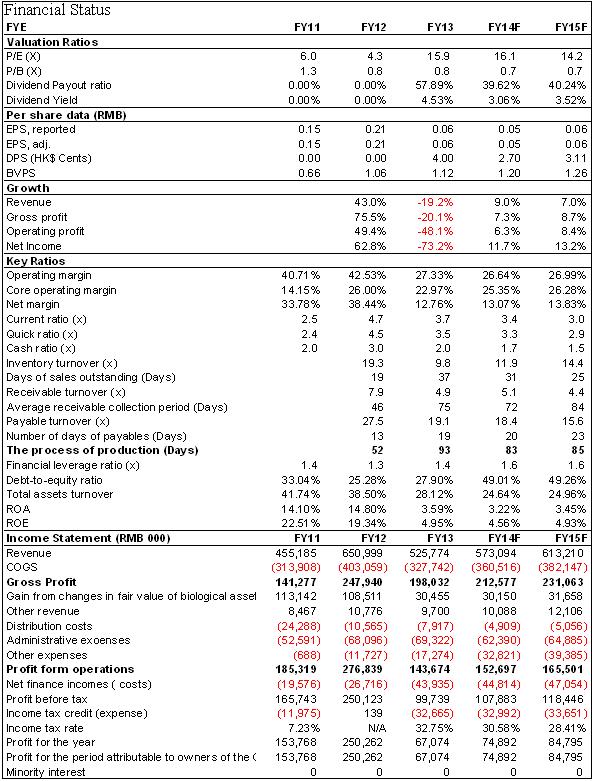

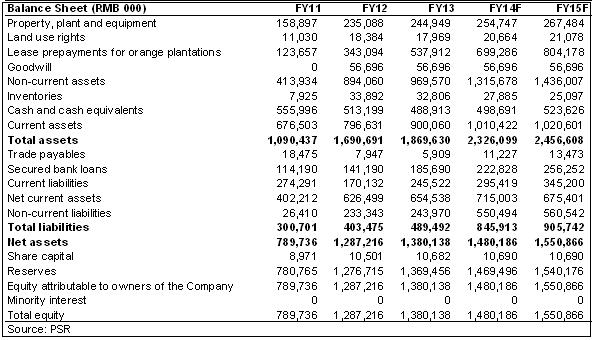

-China Tianyi is the largest products manufacturer who is principally engaged in processing and selling of FCOJ in China. By the end of Dec 2013, the Group`s revenue increased by 18.4% y-y to RMB 279 million. Net profit amounted to RMB69.028 million with the year-on-year growth rate of 12.6%, equivalent to the EPS of RMB0.06; better than our previous expectation;

-China Tianyi owns quite strong anti-risk ability from upstream production to downstream sales benefited from the unique integration business model, and therefore gains the strong profitability. In 1H2013/2014 (Dec 2013), its gross margin and net margin still maintained quite high level as 32.70% and 25.00% respectively;

-China Tianyi still owns quite rich cash flow to ensure there are enough liquid assets to meet the matured liabilities in future, but total cash flow decreased compared with the previous year. Additionally, the Group`s capital expenditure increased sharply, and the bank loans raised significantly, which caused the debt ratio went up obviously, representing the deterioration of the financial condition. As at the end of 2013, the Group`s cash and cash equivalents recorded to RMB424 million. Current ratio increased from 3.7x in the fiscal year of 2013(Jun 2013) to 4.1x, but D/E ratio grew from 27.9% to 42.71%;

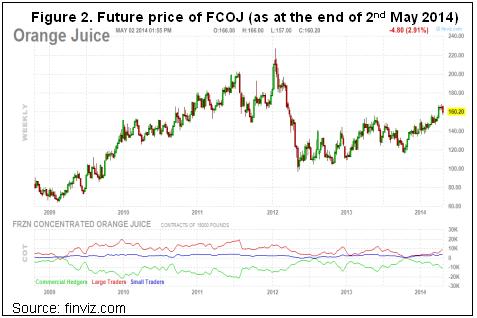

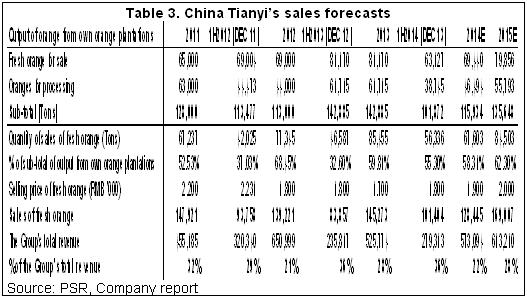

-Considering the Group`s quite strong profitability, and the increase of the orange selling price under the improvement of the market in future, we believe the Group`s sales will go up stably. However, it is worth noting that China Tianyi`s net profit margin only recorded 13% approximately in the fiscal year of 2013(Jun 2013), huge difference compared with that in Dec 2013, which was mainly because of the adjustment of income tax. We believe such adjustment will have a large impact for the net profit, and it is unstable for the profit estimation. However, even based on the conservative view, including the impact of adding income tax, we expect China Tianyi`s net margin will maintain increase slowly with the level of 14% approximately in the next two years, and the net profit may achieve to RMB85 million in 2015;

-Based on the bright market prospect, and the Group`s leading position in the industry with the moderate operating strategy, we have quite strong confidence in China Tianyi`s profit growth in future, increase the 12-month target price to HK$1.45, around 32% higher than the latest closing price, equivalent to 18.8xP/E and 0.9xP/B 2015E respectively, and recommend Buy.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()