-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Kunlun Energy (0135.HK) - TP reached again, maintain `Accumulate` rating

Thursday, January 31, 2013  9558

9558

Kunlun Energy(135)

| Recommendation | Accumulate |

| Price on Recommendation Date | $16.480 |

| Target Price | $18.100 |

Weekly Special - 002050 Sanhua

Company profile

Kunlun Energy Company is an international energy company focusing on exploration of oil and gas field, natural gas pipeline, terminal sales and comprehensive utilization, and the development of new energy etc, whose parent company, PetroChina, is the largest manufacturer and supplier of gas and natural gas in mainland China. The company's business of gas exploration and development is distributed throughout the mainland China, The Republic of Kazakhstan, Oman, Peru, Thailand, Azerbaijan and Indonesia etc., and its business of natural gas is mainly scattered in mainland China.

Investment Summary

Natural gas in the Twelfth Five-Year Plan has been officially published and the natural gas market has gradually switched from government guidance price to the pricing methods based on market supply and demand. Once the perfect internal market mechanism is established, the company's performance will grow continually and strongly.

The proportion of upstream oil exploration and production in company's business is still declining, and such business proportion in the company's total operating revenue in 2012 is expected to be less 20%. From the long-term development strategy of the company, it doesn`t have much new funds and projects input in exploration and production segment. So the business may lack of new performance point in the future.

The company's downstream distribution businesses of natural gas currently still focus on the city gas pipeline, and will move to LNG stations in the future. The company planed to double the quantity of current LNG stations benefiting from large natural gas network and source advantages of its parent company, PetroChina.

Currently natural gas is only 4% in China's energy consumption, and it reaches to 24.1% in the world energy consumption. The market of natural gas has great potential of development in China, and it is the trend that natural gas would instead of liquefied petroleum gas in future, therefore the company would also have larger potential of expansion.

The company's performance is better than our expectation, and the target price has been achieved ahead. Currently the P/E ratio is quite high, and there is no much room for the increase of price due to the large demand of adjustments in the short run. However, the price should go up continually in the medium and long term based on strong supports coming from the company's performance and great development prospects. In summary, we continue increase the company's estimated EPS to HK$0.97 in 2013, with the latest target price of HK$18.1, maintain `Accumulate` rating.

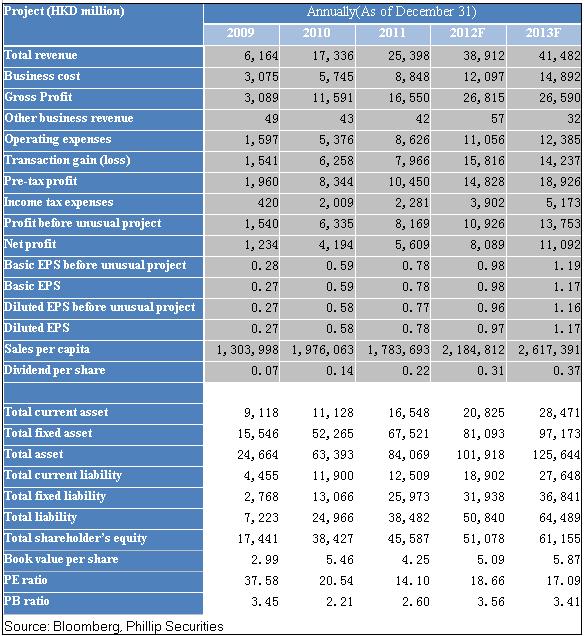

Financial Statements and Predictions

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()