-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

OURGAME (6899.HK) - From online to offline, the new business model likely brings in loyal customers

Friday, July 11, 2014  21998

21998

OURGAME(6899)

| Recommendation | Accumulate |

| Price on Recommendation Date | $3.750 |

| Target Price | $4.100 |

Weekly Special - 2333 Great Wall Motor

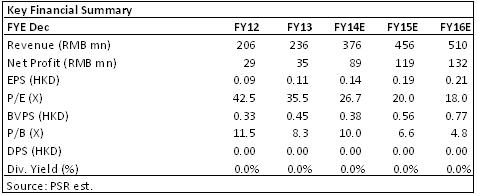

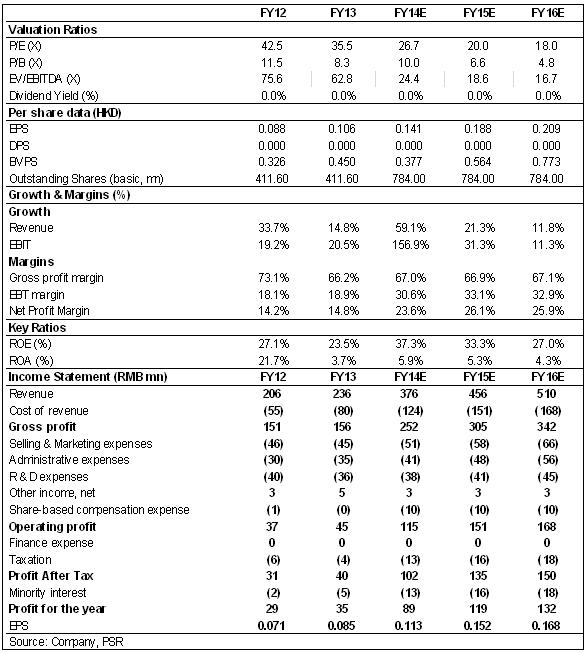

-Ourgame’s 1Q14 revenue up 101.3% yoy. Among which 71.5% was coming from the self developed PC games and RMB 17.3Mn was the mobile games revenue, which already exceeded the 2013 total of RMB 15.6Mn. Gross profit margin maintained as 66.6% and net profit surged 12 times yoy and was over 60% of the 2013 net profit.

-To capture the fast growing card game market, the company started to organize poker tournaments in 2012, and as co-organizer in the 14th World Bridge Championships in 2014. It is expected to obtain huge publicity and goodwill through this kind of activities.

-It is now trading below the initial offering price and we give it an initial rating of “Accumulate” with target price HK$ 4.10, equivalent to 28x of 2014 forecasted EPS plus cash per share HK$ 0.15.

Financial Highlights

Ourgame listed on the main board at June 30, 2014. According to its listing prospectus, the 1Q14 revenue amounted to RMB 93Mn, up 101.3% yoy. Among which RMB 66.5Mn was coming from the self developed PC games, accounted for 71.5% of the total revenue. RMB 17.3Mn was the mobile games revenue, which already exceeded the 2013 total of RMB 15.6Mn. Gross profit was RMB 61.9Mn with gross profit margin maintained as 66.6%. Profit attributable to shareholder amounted to RMB 21.6Mn, which surged 12 times yoy and was over 60% of the 2013 net profit.

How we view this

Ourgame started to operate online card and board game since 1998, which the brand name is familiar to PRC customers. Since the share on PC games showed a continuous declining while revenue from mobile game keeps on increasing, to capture the fast growing card game market, the company started to organize poker tournaments in 2012, which is authorized by the World Poker Tour, and is chosen as co-organizer in the 14th World Bridge Championships in 2014. It is expected to obtain huge publicity and goodwill through this kind of activities.

Investment Action

With the online to offline operating model, the company is likely to capture high quality potential new customers through the matches. It can also increase the existing customers’ involvement and thus their loyalty. Once the customers stay in the game, monetization becomes much easier. However, we believe Ourgame is priced a bit higher for its IPO of HK$ 4.25. It is now trading below the initial offering price and we give it an initial rating of “Accumulate” with target price HK$ 4.10, equivalent to 28x of 2014 forecasted EPS plus cash per share HK$ 0.15.

Product mix shifts to self developed games

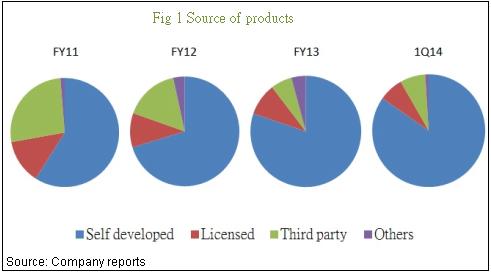

Ourgame operated over 200 PC games through its own online platform and the client portal Ourgame Hall. In 2011, only 59% of revenue was coming from self developed games, the figure increased to 80.2% in 2013 and further to 84.7% in 1Q14. However, the company did not rely on any single game category on the customer base or the revenue generated. No any single game category accounted for more than one-third of the total revenue.

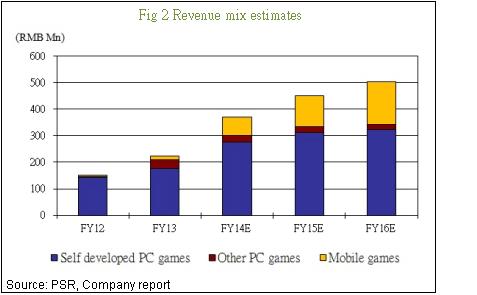

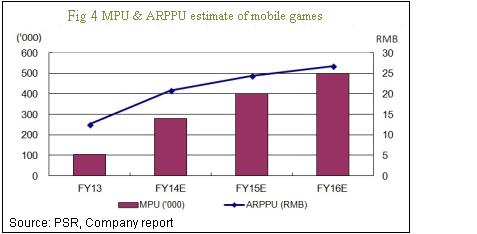

Revenue from mobile games ramp up

According to its listing prospectus, among the 1Q14 revenue, RMB 17.3Mn was obtained from mobile games, accounted for 18.6% of the total revenue, which already exceeded the 2013 total of RMB 15.6Mn. It is expected the share will keep going up since the company is actively shifting the existing PC games to the mobile market.

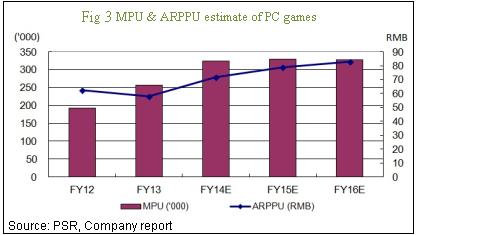

Both the MPU and ARPPU increased for PC games and mobile games in 2013. However, the MPU for PC games is expected to stay in 2015 and start to drop in 2016. Mobile games are believed as the future growth momentum which MPU and ARPPU are forecasted to ramp up in the coming years.

From online gaming to offline matching

In order to capture the fast growing card game market, the company started to organize poker tournaments in 2012, which is authorized by the World Poker Tour, and is chosen as co-organizer in the 14th World Bridge Championships in 2014. Meanwhile, it has also produced a game show which has been broadcasted in several PRC TV channels. It is expected to obtain huge publicity and goodwill through this kind of activities. With the online to offline operating model, the company is likely to capture high quality potential new customers through the matches. It can also increase the existing customers’ involvement and thus their loyalty. Once the customers stay in the game, monetization becomes much easier.

Cost soars and expenses go reversely

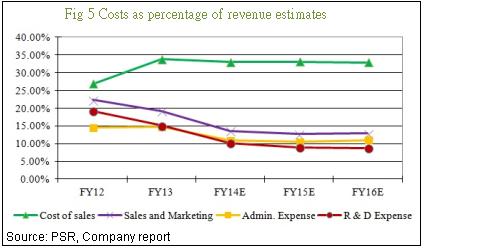

The 2013 cost of sales soared 44.4% to RMB 79.8Mn which represented 33.8% of revenue, up from 26.9% in 2012. The expenses dropped, compared to the revenue in 2013. We estimate the cost to stay at current level and the expenses to further drop a bit since we expect the revenue will grow at the rate faster than the expenses.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()