-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Jinjiang Hotels (2006.HK) - All the way to the sail route!

Friday, July 8, 2016  20347

20347

Jinjiang Hotels(2006)

| Recommendation | Accumulate |

| Price on Recommendation Date | $2.490 |

| Target Price | $2.980 |

Weekly Special - 2333 Great Wall Motor

Company Profile:

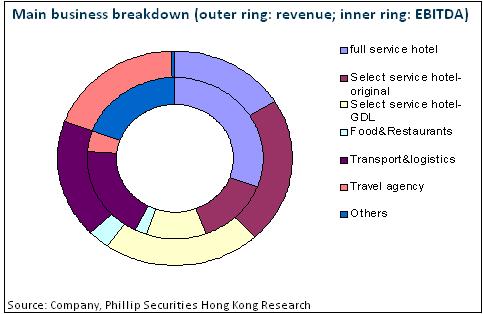

Jin Jiang Hotels is a leading hotel group in China and mainly engaged in 1) the operation and management of high star-rating hotels, 2) franchising of budget hotels & operation of restaurants, 3) passenger transportation logistics and 4) travel agency business. To be specific, hotel business accounts for 60% of the company's total revenue and 50% of total EBITDA. The later three businesses are operated by holding subsidiaries which have been listed on A share market, including Jin Jiang Hotels Development (600754.SH/900934.SH), Jin Jiang Investment (600650.sh /900914.SH) and Jin Jiang Travel (900929.SH). Jin Jiang International Group holds 75% of equity in the company and the de facto controller is the State-Owned Assets Supervision and Administration Commission of Shanghai Municipal Government ("Shanghai SASAC").

M&A

In 2015, the company acquired Louvre Hotels Group (GDL) and Keystone Lodging Holdings Limited with a consideration of nearly RMB 20 billion. After the completion of the acquisition, the company's total number of hotels doubled to more than 6000 as compared with the previous hotels, and the total number of rooms exceeded 650,000. Based on the number of rooms, Jinjiang Hotels is among the world's top five hotel groups and takes the first spot in China.

Currently, the company's brands encompass J. Hotel, Jin Jiang, Metropolo, Jin Jiang Inn and other series, series brands under the acquired Louvre Hotels Group, 7 Days Inn and Portofino Hotels & Resorts, Lavande Hotels and James Joyce Coffete, and other high-end hotels of Keystone Lodging.

SWOT Analyst

Strengths

-The company has devoted itself to the hotel industry for many years and its brands are renowned in China with a huge business network and abundant management experience;-It is well-established in Shanghai with the domestic hotels located in the prime areas within Shanghai. After the acquisition of Keystone Lodging, geographically, it further expands to South China, Central China and other regions;

-The company owns a multi-level and diversified hotel asset portfolio and hence can satisfy a wide range of market demand;

-It employs advanced scientific information direct sales and management systems and CRS, CRM, PMS and other central information systems to guarantee the customer experience;

Weakness

-In terms of brand awareness and customer experience, there is a gap between the company and international hotel giants (such as Intercontinental, Hilton and Shangri-la). Also, the business profitability of the company's high-end hotel is far lower than that of the latter;

-The medium and high end hotels of Keystone Lodging are in the transition period and recorded slight loss in 2015;

Opportunities

-By means of continuous M&A, the company rapidly expands its scale. If its brand management, channel marketing, integration of back office management and other aspects can be smoothly advanced, it is expected to form scale advantage;

-The transportation, accommodation, catering and tourism demand brought by the opening of Shanghai Disneyland Resort and the establishment of the Shanghai Free Trade Zone will promote the development of the company's business in the long run;

-Chinese outbound tourism demand is continuously exploding;

-Potential SOE reform expectation contributes to large room for improving operational efficiency;

Threat

-Macroeconomic slowdown and decrease in demand growth caused by restrictions on "spending on official visits, official vehicles, and official hospitality" exceed expectation;

-The Internet+ sharing business model with the representatives of Airbnb and Bed & Breakfast may squeeze the market share of the traditional hotel industry;

-Continuous major acquisitions may increase the financing costs and the surge in financial expenses reduces profits;

-Uncertainties in the subsequent asset integration process;

-Exchange rate risk resulting from the expansion of overseas business;

Investment Thesis

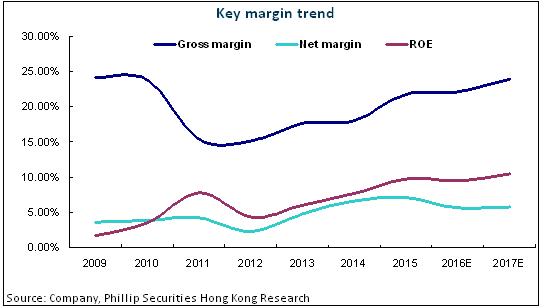

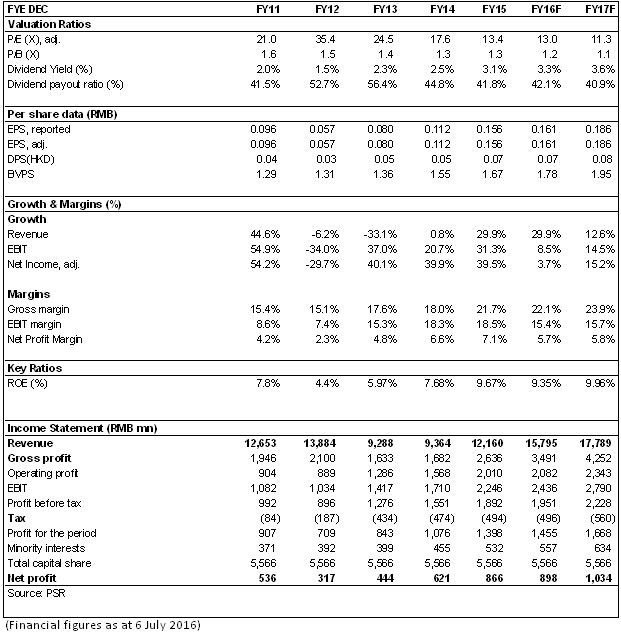

We cover Jinjiang Hotels initially and expect the company's EPS in 2016/2017 will reach RMB 0.161 / 0.186, respectively. The target price is HK$2.98, equivalent to 15.5x/13.5x P/E ratio in 2016/2017. Also, the "Accumulate" rating is given. (Closing price as at 6 July 2016)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()