-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

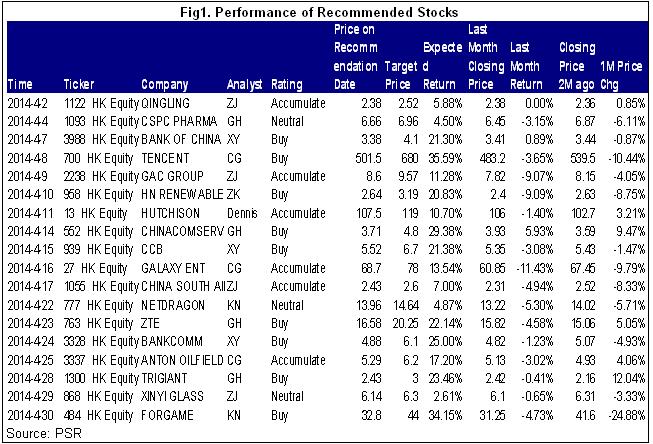

Report Review of April 2014

Friday, May 2, 2014  4489

4489

Report Review of April 2014

Weekly Special - 002050 Sanhua

Industry:

Software(Kay Ng), Mainland financial, Utilities (Xingyu Chen), Mainland Telecom (Fanguohe),Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing), New energy & Environmental Goods (Zhang Kun)

Software(Kay Ng)

Overall share price of the Software and Internet service sector reached a record high in the 1Q FY14 and a callback later on. The drop continued in April which share price declined 10% to 20% in general during the month. The industry leader Tencent fell below $ 500 at the last trading day of April. However, back to fundamentals, companies were generally recorded good earnings growth for the FY13. We remain optimistic about the long-term performance of the industry and believe the valuation can reasonably reflect companies` profitability in the long run.

This month our report initially covered two software stocks - NetDragon (777.HK) and Forgame (484.HK).

NetDragon (777.HK) disposed its entire 51% stake of 91 Wireless to Baidu in August 2013, for a total consideration of RMB 6.7 billion, which resulted in substantial growth in net profit of 157 times to RMB 61.41 billion. After giving up the 91 Wireless, NetDragon planed to find another blue ocean, to develop the online education platform. Through enriching the content of its "open educational cloud platform" and connecting to various terminal devices, thereby expanding its market share and thus revenue. NetDragon had set up two joint venture companies to jointly develop and operate online education applications. Althoughthe income from online education was not yet predictable, the company held over RMB 44 billion, which provide sufficient capital for the potential merger and acquisition opportunities. Based on the highly competitive online gaming environment faced by the company, the concurrent users even dropped for the 4Q FY13 yoy and qoq, and doubt for time when its online education business can provide contribution, we initially give the rating as "neutral", target price of HK $ 14.64.

Forgame's (484.HK) FY13 revenue grew by 52.3% to RMB 1.183 billion. However, net profit turned from profit to loss, recorded a RMB 469 million loss, which mainly due to a RMB 741 million of fair value loss of converting all its existing preference shares to ordinary shares.

This was a one-off loss, and will not produce any expected future costs. In fact, revenue from game development rose 47.8% to RMB 799 million, with monthly paying user (MPU) increased by 37.1%. Revenue from game publishing increased 62.6%, and monthly paid users (MPU) increased 53.5%. All these reflected Forgame's operating activities are performing well. Company acquired 21% stake of Magic Feature Inc. and indirectly operated its popular mobile game “Tower of Saviors”. The company on one hand used this game as a flagship product to enter the mobile gaming industry in PRC, and on the other hand increased capital investment in mobile gaming, reflected that it was implementing the product transformation. The share price dropped more than 55% from its high but we expected mobile gaming could bring considerable growth in the future. We initially give a target price of HK $ 44, relative to 14/14.2/11.2 times PE for the year 2014/2015/2016, rating as "buy."

Mainland Financial (Xingyu Chen)

The market was quite stable in April, HSI moved between 22,200 and 23,200. Most of Chinese banks` prices went down. Domestic banks announced 2013 Annual Results and first quarterly reports of 2014 this month, according to the data, the banks` profits increased stably, but growth rates declined, in line with our expectation. The major reasons include the low level of NIM, and the slow-down of the growth of interest incomes, especially, impairment losses increased significantly due to the obvious deterioration of the asset quality. According to the current data, as at the end of 1Q2014, the amount of NPLs of BOC, CMB, BoCom increased by 8.7%, 7.7% and 5.1% respectively compared with the end of 2013. We believe the banks` asset quality will continue to deteriorate, and the impairment losses will increase strongly, which may affect the banks` performance in the next few years.

However, CITIC Bank still recorded the better performance among the peers this month, the price increased from HK$4.45 at the beginning to HK$4.8 currently, up 6.7% approximately. Overall, the banks` operating performance meets the expectation, and therefore we maintain Accumulate rating to the sector.

Mainland Telecom (Fanguohe)

In April, the three carriers published first quarter report one after another. The traditional performance such as messages continued to wither, China Mobile's ARPU (the average income per family monthly) decreased by 1 yuan to 62 yuan, and the efficiency of 4G business and iPhone 5s was not good, which both let its net profit decrease by 9.4% on year-on-year basis, which didn`t fulfill market expectation. With benefits from interconnection settlement cost saving up, China Unicom's net profit increased by 73.9% on year-on-year basis to 3.3 billion RMB. However, reform from the business tax to a value-added tax will expand to communication industry, and operators are likely to meet with the situation of tax burden increase. Plus the 4G capital expense and marketing investment maintained in a high position, relevant stock prices are still expected to be suppressed.

ZTE, the main equipment supplier, also published the quarter report, whose net profit increased by 203.51% to 0.622 billion RMB. It mainly benefited from a large number of revenue confirmations of 4G main equipment with high gross profit margin, progress achieved from overseas businesses and the decrease of finance expenses brought by RMB devaluation. As the core supplier of main equipment, ZTE is expected to obviously benefit from the advent of 4G investment period and its cellphone terminal business will also turn around. We keep an optimistic attitude to the company.

The report of MIIT shows that in the first quarter of 2014, cellphone shipment volume was 0.1 billion sets, a decrease by 24.7% on year-on-year basis. Wherein, the shipment volume of domestic brands was 66.86 million sets, an decrease by 34.9% on year-on-year basis; while the shipment volume of international manufacturers, such brand representatives as Apple and Samsung, was 33.95 million sets, an increase by 9.2% on year-on-year basis. Just for smart mobile phones, the shipment volume of the first quarter was 89.11 million sets, a decrease by 9.8%. However, we think, 4G cellphones will become the new engine of cellphone industry in China. Currently, 4G cellphone sales only account for 4.1% of the sales of domestic enterprises, while those of international enterprises account for 20.6%. Shortly before, downstream terminals such as Coolpad Group have experienced a great call-back, and we think they still face optimistic opportunities in the future.

Mainland Property & Oil/Gas service (Chengeng)

In April, 2014 I wrote three research reports on Tencent, GEG and Antonoil, which got success by unique operation model. We recommend “Tencent”. Tencent has significant advantage in Chinese Internet social platform, and it is one of the most excellent Internet companies in China. Better business models and more diversified Wechat services will support the monetization of mobile terminal, which will become the major driving force for the future share price. Based on the new upsurge of Internet application and favorable expectation on the development prospect of Tencent, we give Tencent Holdings the rate of "Buy", with the target price of 680 HKD for 12 months, which amounts to 43 times and 32 times of expected P ratio in 2014 and 2015 respectively.

Automobile & Air & Infrastructure (ZhangJing)

We released 4 reports: updated Qingling(1122.HK), GAC(2238.HK), CSA(1055.HK) and initiated coverage on Xinyi Glass(868.HK) on April, among which, we recommend GAC most as the invest values emerged after the adjustment.

The Company plans to introduce several new models in 2014 including: GAC Honda's new FIT, new Odyssey, small-sized SUV based on the platform of FIT, and updated Crosstour; GAC Toyota plans to introduce a new compact sedan and updated Camry. The Company announced to inject 1.8 billion into GAC Fiat, and expects to import Jeep's SUV, which would go into operation as early as the end of 2015. As the importing SUV brand with the largest sales volume, Jeep will offer the great opportunity for the Company's growth. We believe the Company's performance will be improved continually in 2014, lifted our 2014/2015F EPS to RMB 0.72/0.92yuan, respectively for 74% and 29% yoy growth. We revise the Company's 12-month target price to HK$9.57, equivalent to 10/8xP/E for 2014/2015 respectively, then Accumulate rating

New energy & Environmental Goods

The stock price of this sector has downward trend and high volatility this month. The overall valuation level went down and there is a large upside potential in the future. Market waits good news and giving guidance to industry. Two new policies were published in this month. The Ministry of Environmental Protection published `the announcement of approval of launching environmental service trials` on April 4th. It means the new development of changing from environmental protection industry to service. The main tasks of the service are providing emission reduction, pollution abatement and environmental evaluation consultant service to government and other companies. The announcement also appoints 19 trials, include China Energy Conservation and Environmental Protection Group and Sound Group, the subsidies of them, CECEP COSTIN (2228.HK), China Ground Source Energy (8128.HK) and Sound International (967.HK) are all listed in Hong Kong market. The National People's Congress approved the new `Environmental Protection Law` on April 22nd. It provides more restrict requirement to companies, and will punish deregulation severely. It forces more companies to increase environmental protection service cost. We feel confident about the industry's future development.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()