-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

KINGDEE INT`L (268.HK) - PRC's promotion on the Cloud service as source of future revenue

Tuesday, December 2, 2014  17287

17287

KINGDEE INT`L(268)

| Recommendation | Accumulate |

| Price on Recommendation Date | $2.450 |

| Target Price | $2.750 |

Weekly Special - 2333 Great Wall Motor

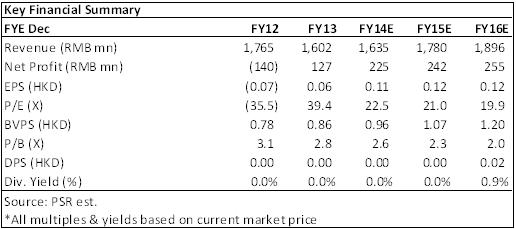

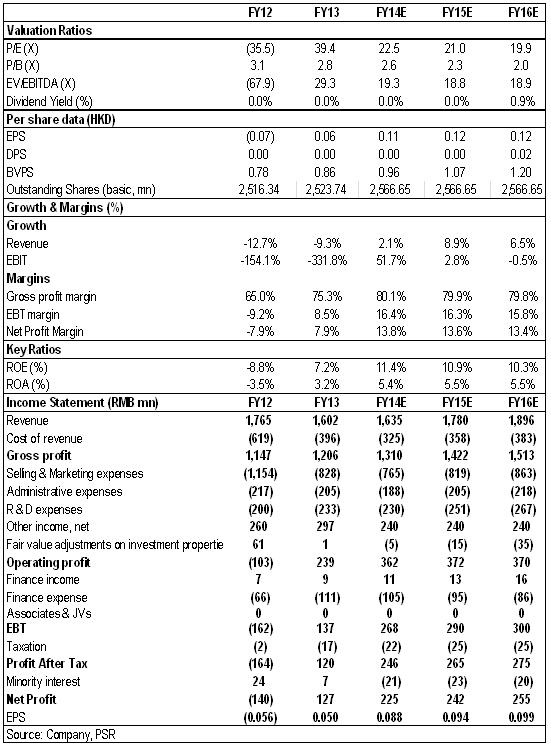

-The wholly owned subsidiary Kingdee China reported operation figures for the first three quarters. Revenue slightly up 0.47% yoy and net profit surged 582% yoy.

-PRC government has announced to promote China’s cloud service to neighborhood countries in support to the “New Silk Road” strategic development, which expected as the future growing source of revenue.

-We give Kingdee “Accumulate” rating while lower the target price to HK$ 2.75, equivalent to 21.8x/20x of 2014 and 2015 forecasted EPS, plus HK$ 0.35 net cash per share in the first half.

Financial Highlights

The wholly owned subsidiary Kingdee China reported operation figures for the first three quarters. Revenue amounted to RMB 1,075 mn, slightly up 0.47% yoy. Net profit surged 582% yoy to RMB 109 mn. Net profit margin 10.13% was close to the Group’s 10.86% in the first half. Cash from operating activities sharply increased 168% yoy to RMB 211.5 mn.

How we view this

The figures were in line with our expectation while we believed this showed a similar picture for the Group’s performance. We forecast the Group’s revenue for 2014 would just slightly higher than last year. Though the cloud business is believed to have further growth in the last quarter as well as 2015 since the PRC government has announced to promote China’s cloud service to neighborhood countries in support to the “New Silk Road” strategic development. Kingdee is expected to be benefited. Meanwhile, the cost structure has improved as mentioned in the last reports, which increase in revenue would widen the profit margins.

Investment Action

We believe the cloud business would experience rapid growth in the next few years. Besides the New Silk Road, the government has frequently announced to promote the local software and servers. Thus, more large enterprise may try Kingdee’s enterprise software or cloud server in the future

However, refer to the 1H14 data, we adjust the estimates on the other incomes, which are mainly the subsidies from government, resulting in lower profit and forecasted EPS. We give Kingdee “Accumulate” rating while lower the target price to HK$ 2.75, equivalent to 21.8x/20x of 2014 and 2015 forecasted EPS, plus HK$ 0.35 net cash per share in the first half.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()