-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Ajisen (China) Holdings (538.HK) - Attractive valuation

Thursday, February 23, 2017  22830

22830

Ajisen (China) Holdings(538)

| Recommendation | Accumulate |

| Price on Recommendation Date | $3.090 |

| Target Price | $3.410 |

Weekly Special - 002050 Sanhua

Investment Summary

-Intensity of competitive rivalry within the restaurant industry is extremely high, we are not very optimistic about the firm's long-term prospects.

-The valuation is attractive, and the group has a stable cash flow.

-After cooperating with delivery service mobile applications, the takeaway delivery service can be a new potential growth engine.

Company Overview

Ajisen (China) Holdings Limited is a casual restaurant chain operator in China and Hong Kong. The company has established in 1996, mainly selling Japanese ramen and Japanese-style dishes under the Ajisen brand in China and Hong Kong. By incorporating Chinese people's culinary preferences and the essence of the Chinese cuisine, the Group has carefully developed over one hundred types of Japanese-style ramen and dishes that cater for the Chinese people's palate. All restaurants are not only selling Japanese ramen, as well as many Chinese cuisine influenced noodles and rice dishes.

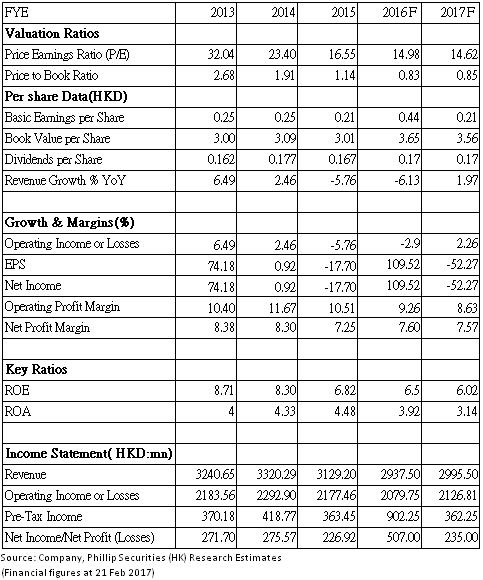

According to the 2016 interim result, the Group's revenue decreased to approximately HK$1,395.39 million, representing a decrease of 11.1% compared with the corresponding period in 2015. The gross profit of the Group reached approximately HK$987.89million, representing a decrease of approximately 9.8% for the same period in 2015. The net profit increased to approximately HK$671.15 million, which represents an increase of approximately 506.2% for the same period in 2015. The significant increase in net profit is mainly because the Group has recognized a fair value gain on financial asset (Baidu Takeout Delivery) designated as at FVTPL of approximately HK$745,938,000 in the 1H FY2016. For the period, the gross profit margin increased to approximately 70.8% from approximately 69.8% thanks to the stability in raw material costs and the value added tax reform in China. Not only did the property rentals and related expenses decreased by about 6.5%, the staff costs also decreased by about 12.5% for the period.

Overall, the performance of the core business is not optimistic. The revenue of the whole industry has grown up 6.6% YoY, but the revenue of firm has been deceased by 11.1%. This is mainly due to many new competitors entered into the restaurant industry. However, the increase of new competitors is slowing down. According to the data from the website (www.dianping.com), growths of catering industry in the first-tier cities (Beijing, Shanghai, Guangzhou and Shenzhen) were within 10% in the first half of 2016, far below that of 50% growth throughout last year. As at 30 June 2016, the Group's operates 662 Ajisen chain restaurants, apparently focuses on streamlining the existing stores, adopts a prudent strategy in opening new stores. In 2015, the Group focus on promoting its takeaway service, the number of restaurants offering takeaway service increased to 396 from 52 in 2014, and the number is expected to increase to 500 in 2016. In addition, the Group participated in the investment of the “Baidu Takeout Delivery” and became its shareholder.

Ajisen (China)'s Porter Five Forces Analysis

By incorporating Chinese people's culinary preferences and the essence of the Chinese cuisine, the Group has carefully developed over one hundred types of Japanese-style ramen and dishes that cater for the Chinese people's palate.

All restaurants are not only selling Japanese ramen, but also many Chinese noodle soups and rice dishes:

1. Competitive Rivalry (Extremely Strong Force)

Ajisen faces extremely tough competition because the restaurant market is already saturated in China and Hong Kong. The restaurant industry has many firms of various sizes, such as global chains like McDonald's, KFC, and local middle/small sized restaurants. Also, most medium and large firms aggressively market their products. In addition, the group's customers had low switching costs, which means that they can easily transfer to other restaurants. And also, many branded Japanese Ramen restaurants such as Ippudo or Butao are expanding in China and Hong Kong in recently years. Many wealthy customers rather choose Ippudo or Butao. Thus, this element of the Five Forces analysis of Ajisen(China) shows that competition is the most significant external forces for the business.

2. Threat of New Entrants (Strong Force)

The threat of new entrants is strong, since entry barriers within the industry is low. The moderate capital costs of establishing a new restaurant makes it easy for small or medium-sized firms to entry the industry. However, the group has a relative well-known brand, it is not easy for new competitors to replicate. However, the brand image advantage has become significantly weaker after the 2011 scandal. Back in 2011, the company was accused of lying about the ingredients it used in its soups.Thus, this element of the Five Forces analysis shows that the threat of new entrants is a considerable issue for the group.

3. Threat of Substitutes (Strong Force)

The threat of substitutes is high, there are many substitutes to Ajisen's products, such as products from small local noodle shops to high end Japanese ramen restaurants such as Ippudo and Butao. And also, Consumers can cook their food at home. Because of the low switching costs, consumers can easily move from ajisen toward other restaurants.

4. Bargaining Power of Customers (Strong Force)

The bargaining power of customer is strong as well, because of the low switching costs, consumers can easily move from Ajisen toward other restaurants. Moreover, nowadays customers are well informed about the quality and price because of the internet.

5. Bargaining Power of Suppliers (moderate force)

The Bargaining Power of Suppliers is moderate. The Group continued to increase the proportion of the direct procurement, and maintained its close partnership with large suppliers of meat products, such as Shuanghui and Yurun. In 2015, the proportion of the direct procurement of raw materials within the Group had reached 73%. In addition, the Group has also invested in an egg supplier in 2015.

6. Conclusion

Overall, the competition within the restaurant industry is extremely tough, we are not optimistic about the long-term prospects. The biggest competitive advantage we reckon is the central kitchens. By making full use of the six central kitchens, and the modern food processing technique, the Group standardized all products on a ready-made basis, thus promoted the production efficiency, maintained consistent taste of all products and further assured food safety. However, the advantage of the Japanese ramen brand image has become significant weaker after the 2011 scandal. Because back in 2011, the company was accused of lying about the ingredients it used in its soups, resulting in a huge negative impact on the brand image.

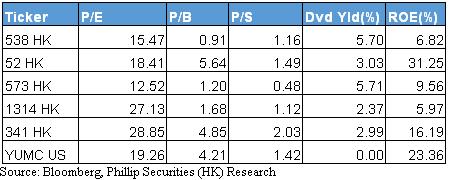

Peer Comparison

The table in above shows the peer comparison of the group. From the PB point of view, the group is the cheapest within its peers, and the group is also the second cheapest in term of PE. Moreover, the firm also provides a fat dividend yield of 5.7%. On the other hand, the earning power of the firm is significant lower than the industry leader YUMC (Yum China) and 341 (cafe de coral), since the ROE of firm is only 6.82%, significantly lower than YUMC and 341. Overall, in terms of PE and PB, the group's valuation is more attractive than its peers, but its earning power is also significantly weaker.

The Valuation is attractive

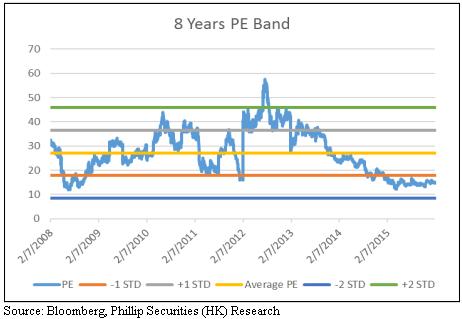

First of all, to examine whether the stock is undervalued, historical PE band could be useful.

The chart below shows 8 years of PE ratio of the stock, the statistic started on 2/7/2008, with 2 standard deviations.

From the chart above, we can see that the valuation is actually appealing. Approximately, the average 8 years PE ratio is 27.14x, one standard deviation below is 17.8x, and the stock trades well below 17.8x.

During the 2008 financial crisis, the stock was trading at similar PE ratio, however, the current market sentiment is significant better than 2008.

From the chart, we also can see the PE ratio dropped significantly after the 2011 scandal. Back in 2011, the company was accused of lying about the ingredients it used in its soups. Not only did the revenue drop, the market expectation dropped a lot further.

We also prepared a PB chart for the stock in below:

From the chart in below, we can see that the PB ratio is almost the lowest since it listed. Before 2015, the stock has never traded below its book value. On the other hand, we also need to examine the earning power.

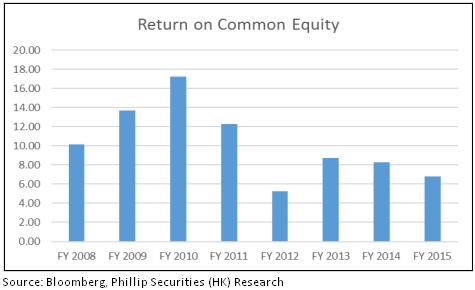

From the bar chart in above, we can see that the ROE of the firm is only 6.82% for the FY2015, which is lower than the histroical average. Howoever, the group has never suffered operating loss, ROE figures were positive in all financial years.

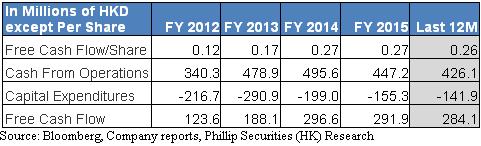

The group has a stable cash flow

For the restaurant industry, the cash flow can be the most crucial part.

From the table above, the group has a stable operating cash flow of 426.1 Million HKD in last 12 financial months, which represents a 5% decrease over the whole FY2015. But the capital expenditure was also decreased by about 8.63%, to only 141.9 million HKD. The free cash flow per share is still 0.26, which is almost identical to the FY2014 and FY2015.

Moreover, to find out whether the stock is undervalued, we used a simple Discounted Cash Flow Model for evaluating the intrinsic value.

Our DCF model suggest an intrinsic value of HKD 3.70 under normal assumption, corresponding to 17.62 FY17 PE, corresponding to 14.81 FY17 PE. The calculated free cash flow for the year 1 is 291.864 Million HKD. We conservatively assumed the perpetual growth rate is 0. The cost of debt is 2.13% as well as an effective tax rate of 16.97%, according to the company report. The risk free rate that the model use is 3.24%, which is the 10 years china government bond yield. The 10 years monthly Beta of 538 is 0.982, market return is 7.16%, which is the 21 years HIS market return. Resulted that the calculated cost of equity is 7.10%. Base on the debt to equity ratio, the WACC that the model use is 6.20%. As a result, our model calculated that the intrinsic value of the stock is HKD 3.70 per share. Since the current price is about 20% lower than the intrinsic value, it is reasonable to say that the stock is undervalued, meaning the downsize risk could be limited.

Delivery service can be a new potential growth engine

As a response to the development trend of the industry, the Group has stepped up its efforts in the promotion of takeaway services in restaurants across China. In 2015, the Group focused on promoting its takeaway service. The number of restaurants offering takeaway service increased to 396 from 52 in 2014, and the number is expected to increase to 500 in 2016. And the firm has established cooperation with a number of takeaway service mobile applications, including “Baidu Takeout Delivery”, “Ele.me”, and “Meituan”. In addition, the Group also invested in the “Baidu Takeout Delivery” and became its shareholder. The group also believed that after the outburst of catering take-out took place in 2015, the situation of three takeout platforms (Ele.me, Meituan and Baidu Takeout Delivery) has established and the campaign for subsidies has faded away. After cooperating with three major delivery service mobile applications, the takeout delivery service possibly to be a new potential growth engine.

Valuation

Taking all the points mentioned above into consideration, Ajisen(China) holdings 's target price is therefore $3.41, with accumulate rating assigned, represents 7.75x FY16 PE and 16.24x FY17 PE. (Closing price as at 21 FEB 2017)

Risks

-Even more extremely tough competition within the industry, could have a huge impact on the revenue of the group.

-Property rentals and related expenses could increase significantly, could result a significant increase for the firm's costs.

-Delivery service unable to become a new profit growth engines, the long-term prospects of the firm could turn out more unfavorable.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()