-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ND Paper (2689.HK) - Ex-factory Price Going Down in March

Wednesday, April 5, 2017  22714

22714

ND Paper(2689)

| Recommendation | Accumulate |

| Price on Recommendation Date | $8.350 |

| Target Price | $9.500 |

Weekly Special - 175 Geely

Price Trends of Raw Materials and Products

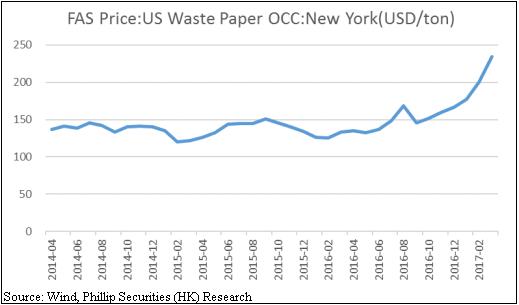

The chart below shows the price trend of US waste paper OCC.

The following chart shows the prices of domestic waste paper. The prices of domestic waste paper went down sharply in March. In 1HFY17 the purchase value of domestic recovered paper accounted for approximately 36.7% of the total value of the Group's purchase of recovered paper.

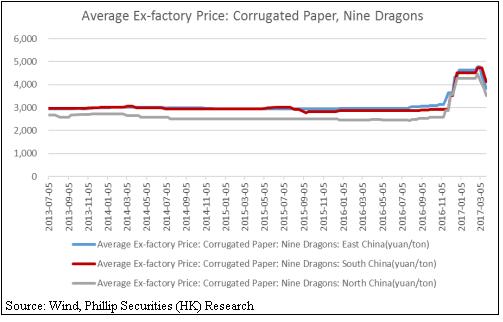

The company produces a broad variety of packaging paperboard products, and the following chart shows the average ex-factory prices of corrugated paper of NDP. The average ex-factory prices of corrugated paper of NDP went down from high level in March.

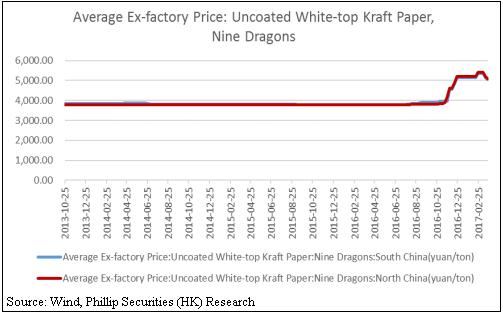

The following chart shows the average ex-factory price of uncoated white-top kraft paper of NDP. The average ex-factory prices of uncoated white-top kraft paper of NDP also went down from high level in March.

Change of Product Prices

The company raised the price by RMB 100-200 in February. The company planned to raise the price again by RMB 100-200 in March. However, according to Wind, the average ex-factory prices of corrugated paper and uncoated white-top kraft paper of NDP all went down in March. And according to Wind, the ex-factory prices of dulex board paper, corrugated paper, uncoated white-top kraft paper, light coated white-top kraft paper and cardboard of some of the industry's companies went down in March. And the price of FBB paper went up in March.

Continuing to Consolidate its Leading Advantage

The government continued to exercise stringent control over environmental protection with high pressure. The increase in paper-making projects was affected by faster closure of outdated and inefficient capacities and much more stringent approval requirements on new capacities, especially prohibition of approval on coal fired power plants. As the industry leader, NDP has high technique of emission and will expand the production capacity in Vietnam, Shenyang, Quanzhou, Chongqing and Hebei Yongxin. The total design production capacity of NDP is expected to exceed 16 mtpa in 2018. NDP will continue to consolidate its leading advantage and this will benefit the future business.

Valuation

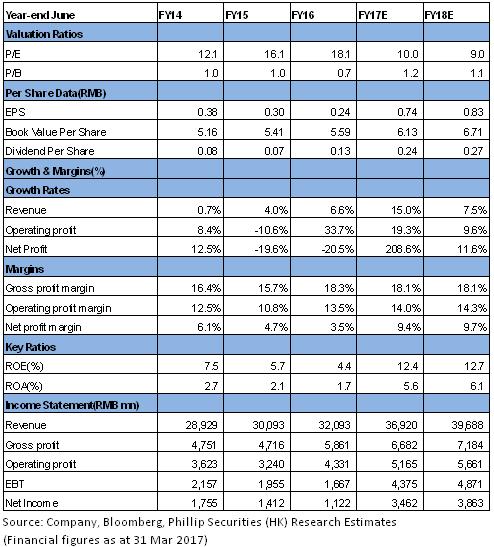

We maintain Accumulate Rating and lower TP to HK$9.50. We also lower our FY2017/FY2018 revenue forecasts by 1.1%/1.1% and lower our net profit forecasts by 2.8%/2.7%. Our TP of HK$9.50 represents 11.4/10.2x FY2017E/FY2018E P/E. (Closing price as at 31 March 2017)

Risk

Foreign exchange risk;

The prices of raw materials such as coal and waste paper rise.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()