-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CANVEST ENV (1381.HK) - Focus on waste-to-energy(WTE), enjoying a promising prospect

Thursday, July 20, 2017  14450

14450

CANVEST ENV(1381)

| Recommendation | Buy |

| Price on Recommendation Date | $4.160 |

| Target Price | $5.000 |

Weekly Special - 2333 Great Wall Motor

Focus on WTE with promising prospect: Canvest Environmental Protection, as the largest non-State-owned WTE provider in Guangdong Province, has expanded its business rapidly since going public. Now the Company holds 13 WTE projects which are mainly distributed in Guangdong, Guangxi and Guizhou, and its capacity in operation and total design capacity have reached 8,600 tons/day and 19,240 tons/day, respectively. At present, the Company has enjoyed a 30% market share in Guangdong Province and the percentage is expected to rise to 69% in 2020. In accordance with the Plan for the Construction of Urban Household Waste Harmless Treatment Facilities in the 13th Five-Year Plan Period, the daily MSW treatment capability in Guangdong Province will be improved from 18,400 tons in 2015 to 73,000 tons in 2020, which is one of the WTE markets with highest growth potentials. Meanwhile, the urban household WTE ratio across the country will be increased from 31% in 2015 to 54%. It is predictable that there is vast room for capacity growth of the Company in the future.

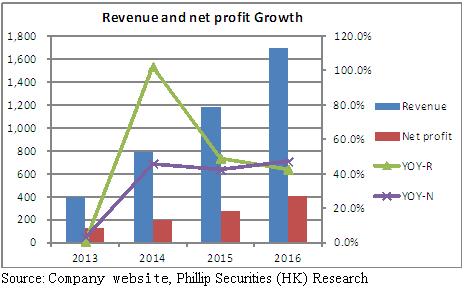

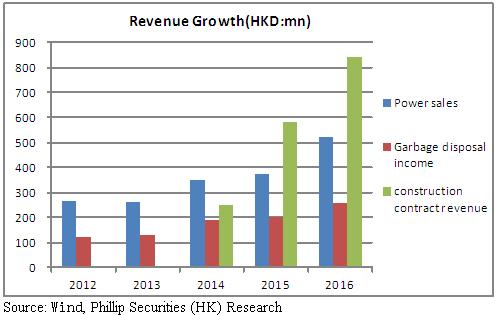

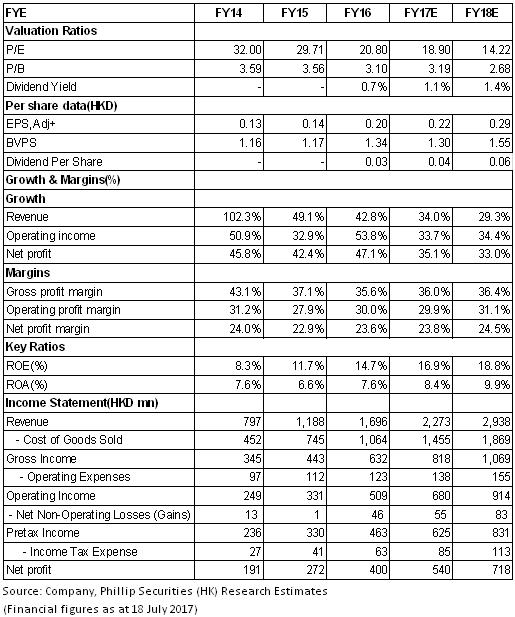

Moderate operation and outstanding profitability: From 2012 to 2016, the revenue rate and compound growth rate of net profit attributable to the parent company were 44.3% and 33.2%, respectively. In 2016, the revenue of the Company was HKD1,654 million (+39.6%), mainly benefiting from the increased income from electricity selling and waste treatment charges since the project was put into operation. The net profit attributable to the parent company reached RMB400 million (+47.1%) and the EPS was HKD0.198 (+45.5%). Specifically, the revenue from electricity selling and waste treatment charges accounted for 46.9%, with a 53.4% gross margin; the revenue from BOT construction services accounted for 51%, with a 16.7% gross margin. In terms of profitability, due to the increase of temporal costs and the change of income structure, the gross margin fell by 1.5% to 35.6%, and it is expected that in 2017 it will steadily pick up. Period expense kept stable and the net profit margin slightly declined by 0.7% to 23.6%.

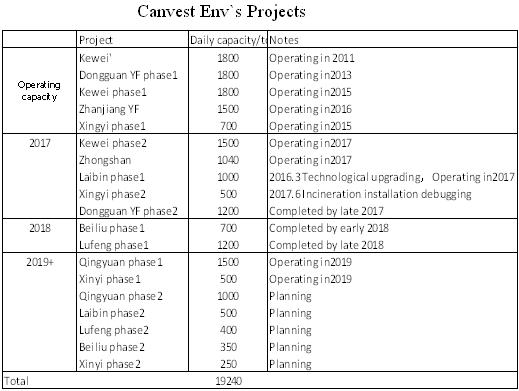

Smooth project acquisition and operation: In 2016, the Company's newly increased capacity was 5,940 ton/day through acquisition and bidding and planned to keep the newly increased capacity at the level of above 6,000 ton/day in 2017. In terms of project operation, the second phase of the Kewei and Zhongshan have been put into operation since April 2017; the technical reform of the first phase of Laibin China Sciences has been completed and the project is expected to put into operation in H2 of this year; at present the second phase of Xingyi has come to the stage of incinerator debugging; the second phase of Dongguan Canvest will be completed by the end of this year. It is expected that the capacity in operation of the Company will reach 11,140 ton/day by the end of this year. In terms of projects under construction, Project Qingyuan has been deferred due to the problem of site selection and planning and will be replaced by Project Lufeng, whose construction will be started in the H2 of this year and is expected to be completed by the end of the next year. In the future, the Company will continue to keep stable project acquisition and commencement, in hope of achieving the 30% compound growth target in the 13th Five-Year Plan period.

Influential shareholders: At the beginning of 2017, the Company has achieved strategic cooperation with BOC & UTRUST Private Equity Fund Management (Guangdong) Co., Ltd. and Utrust International (Utrust Holdings is a financial holdings group directly subordinated to the Department of Finance of Guangdong Province), and it is expected that the cooperation with Utrust Holdings will bring abundant project resources to the Company, and as a result enhance the competitive advantages in Guangdong Province. In February 2017, the Company has introduced Shanghai Industrial Holdings Limited as the strategic investor. The dominant shareholder of Shanghai Industrial Holdings Limited is the biggest overseas comprehensive enterprise in Shanghai, and Canvest Environmental Protection, as a private enterprise, is also known for its quick response capability and risk control capability, so the cooperation of the two enterprises is perfectly possible to facilitate the business expansion of the new projects across the country.

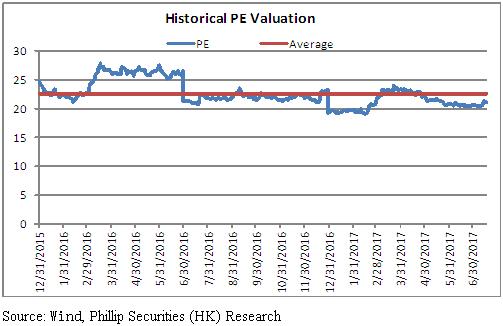

Investment ratings: Canvest Environmental Protection, dedicating to its major industry of WTE, is outstanding in project acquisition capability as well as outstanding operation efficiency. Benefiting from favorable government policies and the expansion of WTE market in Guangdong Province as well as across the country, the Company, with great certainty, enjoys a relatively stable momentum for performance growth in the next three years. We predict that from 2017 to 2018, the Company's revenues will reach HKD2.27 billion and HKD 2.94billion, respectively; net profit HKD 0.54 billion and HKD 0.72 billion, respectively; EPS 0.22 and 0.29, respectively and we set HKD5.0 as its target price, rated as "Buy". (Closing price as at 18 July2017)

Risk Warnings

The newly increased projects are below expectation;

Project construction and operation progress are below expectation;

Tthe progress of its cooperation with Utrust/Shanghai Industrial Holdings Limited is below expectation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()