-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Cowell e Holdings (1415.HK) - Low valuation has basically reflected multiple risks

Monday, May 9, 2016  12032

12032

Cowell e Holdings(1415)

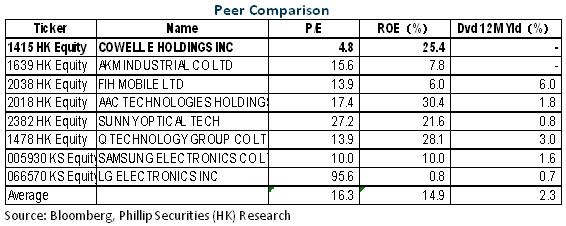

| Recommendation | Buy |

| Price on Recommendation Date | $2.780 |

| Target Price | $3.700 |

Weekly Special - 2333 Great Wall Motor

Steady Growth in 2015

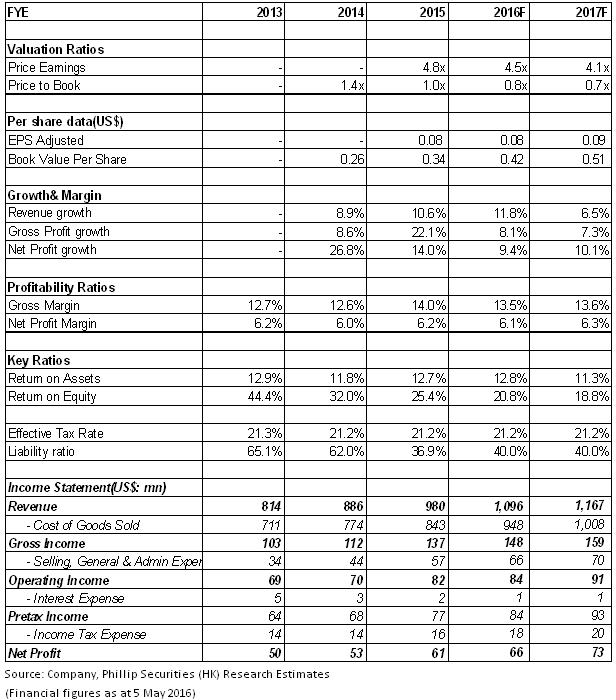

The annual revenue of Cowell e (hereinafter referred to as the "Company") in 2015 was USD980 million with a YoY increase of 10.6%, and net profit was USD60.7 million with a YoY increase of 14.1%. The sales growth of flip-chip camera modules had driven the total module shipments by an increase of 2% to 197.4 million pieces, and the sales price had also increased due to structure upgrade. However, delivery of the Company's chip-on-board (COB) modules to LG had declined.

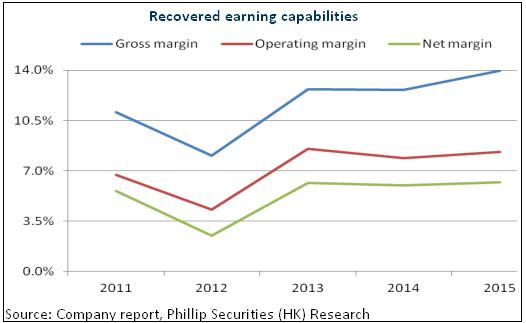

In respect of profitability, the Company's gross profit margin had increased by 1.3 percentage points to 14%, which was mainly the result of the Company's effective management of supplies (with supplies reduced) and productivity improvement. Additionally, the asset-liability ratio had dropped by 25 percentage points to 36.9% through listing and financing, while financial expenses had also decreased by USD1.5 million, making further contribution to performance growth.

Orders of Apple Continue to Be the Main Driving Force in Growth

With advanced flip-chip packaging technology, strong R&D capability, and its high-quality lens modules, the Company has been the only manufacturer supplying Apple with front lens modules for each generation of iPhone/iPad since 2009 (with 50%/20% share of orders). Decrease in the order share of iPhone front lenses is the short-term uncertainty facing the Company, but the Company still has better capacity advantage over potential new suppliers (Foxconn or ASE). In 2016, the Company will have the largest flip-chip front lens module production capacity (with an increase of 35% to 20kk/m already in 2015), so we think the market has worried too much about potential competitors.

It is worth noting that Apple currently contributes 82% of the Company's revenues, which is expected to maintain a steady growth in 2016. Apart from the increase of sales price due to lens upgrade, the output of flip-chip camera modules is expected to grow further. Delivery of CM of Apple's iPhone SE began in April 2016. It is reported that the market demand for the model has exceeded expectation, and Apple has already increased its orders in the second quarter from 3.5 to 4 million units to over 5 million units, and the order in the third quarter will keep up to the same level. In addition, Apple plans to launch new generations of iPhone and iPad in the second half of the year or present substantial innovations. As it is normally the case that shipments will be greatly increased following the introduction of Apple new products, Cowell e is also expected to benefit therefrom.

The new-generation iPhone 7 will probably be installed with dual rear cameras. Since Sharp's financial problem may affect the stability of its supply, Apple may probably introduce new suppliers of rear camera module. The Company, with experience of advanced packaging technology and stable supply since 2009, has the hope to become one of the suppliers of rear cameras to Apple in 2016. The average sales price of rear camera is USD14, which is at least twice the average price of front camera of USD6. Furthermore, the complex production process of rear camera creates higher profit margin than front camera, which can positively impact on the Company's profitability.

Diversification of Risks and Underestimation of Value

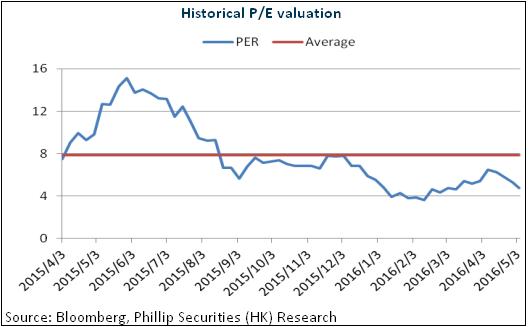

In addition to expanding and maintaining good working relationship with Apple, the Company's management intends to take the lead in expanding the Company's product portfolio using its expertise in semiconductor industry, such as to develop advanced infrared cut-off filters, and at the same time, develop diversified customer base to reduce risks of excessive dependence on one single company. Besides, with the Company's steady growth and good capital structure, we believe that the Company has basically reflected the multiple risks in its valuation which is fairly low. We grant the company the target price of hk$3.7, equivalent to 6X EPS in 2016, with the “Buy” rating initially. (Closing price as at 5 May 2016)

Risks

Market competition has increased.

Shipment of iPhone and iPad is lower than expected.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()