-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Fortune REIT (778.HK) - Steady Growth Continues

Monday, August 7, 2017  19073

19073

Fortune REIT(778)

| Recommendation | Neutral |

| Price on Recommendation Date | $9.690 |

| Target Price | $9.500 |

Weekly Special - 425 Minth Group

Investment Summary

- Tenants in the shopping malls engage mainly in the consumer staples industry, providing stability to the rental income

- High and stable dividend yield , and dividend is expected to grow at a mild rate

Business Overview

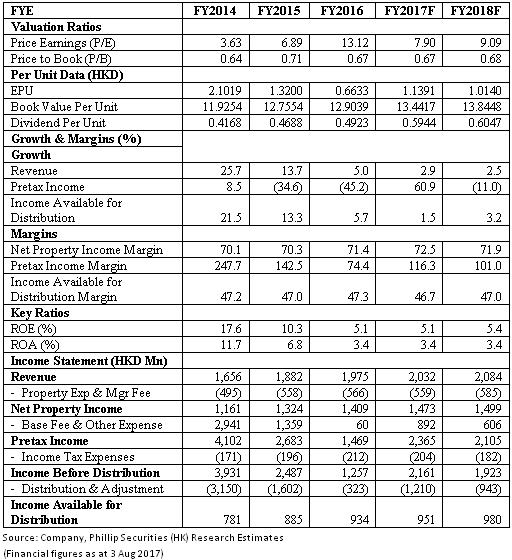

1H2017 result is in line with our expectation: In 1H2017, Fortune REIT's revenue had a YoY increase of 2.5% to HK$1,003.3Mn and net property income had a YoY increase of 3.0% to HK$727.0Mn. The differential between the two is caused by the lower YoY increase of property operating expenses due to effective cost control by the Trust. In fact, the cost to revenue ratio decreased from 25.7% in 1H2016 to 25.3% in 1H2017, contributing to a higher increase in net property income. Income available for distribution increased 3.7% and is mainly caused by the decrease in borrowing cost, which decreased significantly in 1H2017 and had a 5.2% decrease, a result of the Trust refinancing its debt at a lower cost. In 1H2017, the Trust raised its dividend per unit by 3.0% and declared an interim dividend of HK$0.2553 per unit.

Effective cost management promotes growth of net property income: In 1H2017, the Trust achieved a 25.3% cost to revenue ratio. This cost to revenue ratio is the lowest ever since FY2010. The decrease in the operating expenses is mainly caused by the decrease in energy consumption and the receipt of the one off rebate for energy charges, resulting in a decrease in utility charges. However, the cost to revenue ratio for the FY2017 full year is expected to be higher than that of the 1H2017 because in 1H2017 there was a one off energy charge rebate. Due to the non-existence of one off rebate of energy charges, we expect the net property income margin to follow the past years trend and narrow. The following tables list the cost to revenue ratio as well as the property operating expenses incurred by the Trust's properties between FY2010 and FY2017, with FY2010 having the lowest cost to revenue ratio across a decade.

Balance sheet continues to be well-managed: In April 2017, Fortune REIT completed refinancing its loan maturing in FY2018. The new HK$1,200Mn loan will mature in FY2022, maintaining the weighted average maturity of the Trust's debts at around 3.6 years as at 30/6/2017, which is a slight decrease in the term in comparison with the 3.7 years as at 31/12/2016. The effective borrowing cost maintains at around 2.41% in 1H2017, a 2 basis point increase in comparison with FY2016. In particular, 60% of the debt has been hedged via interest rate swaps and caps, allowing the company to lower the interest rate risk due to the possible rate hike. Gearing ratio maintains at a healthy level of 28.4% on 30/6/2017, with only 5 investment properties used to secure for the loans and debts. Since the Trust has a stable stream of cash flow in the form of rental income, effective cost management and large number of unsecured investment properties, the capital structure is considered to be healthy and we believe the Trust is able to finance its asset enhancement initiative with ease.

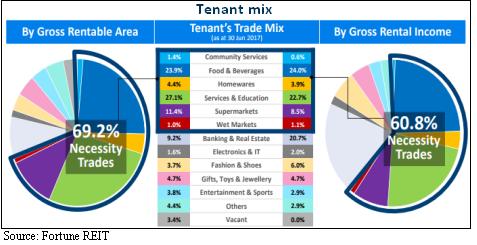

High and stable dividend yield but growth will be mild only: The REIT has a good dividend yield and dividend is steadily rising across years. The tenants of the properties owned by the REIT are highly diversified, with about 60.8% of the gross rental income being generated by the daily necessity industry, such as food and beverages, education, supermarkets and wet markets, thus enabling the Trust to be less affected by shocks in the economy.

The Trust is expected to have no major capital expenditure other than the asset enhancement work on Fortune Kingswood. Moreover, the properties of the Trust has an average occupancy rate of 96.6% throughout the reporting period. Therefore, future growth will likely be fueled by the increase in rent. The Trust can also benefit from the increase in rent collected from the consumer discretionary sector, which contributes to the remaining 39.2% of the rental income, during good time in the economy. Therefore, we expect in the foreseeable future, the growth of the Trust will grow, but at a relatively slower rate.

Investment Thesis, Valuation and Risk

Our valuation model suggests a target price of HK$9.50: Fortune REIT receives a stable stream of income from its investment properties, whose tenants largely engage in the consumer staples sector, allowing the Trust to be less affected by the turbulent economic environment. The Trust also has effective cost management and financial management strategies, as evident by the low cost to revenue ratio and the healthy capital structure. Therefore, a target price of HK$9.50, corresponding to a 30% discount to NAV, and a `Neutral` rating, have been assigned. (Closing price as at 3 Aug 2017)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()