-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Unicom (762.HK) - Profitability will still win revenue growth

Thursday, August 14, 2014  8683

8683

China Unicom(762)

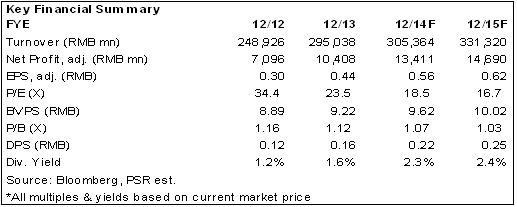

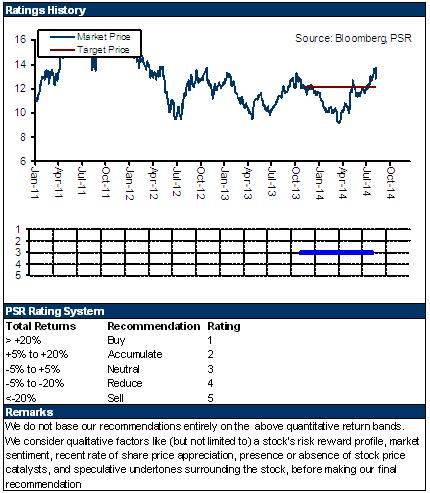

| Recommendation | Accumulate |

| Price on Recommendation Date | $13.020 |

| Target Price | $14.200 |

Weekly Special - 2333 Great Wall Motor

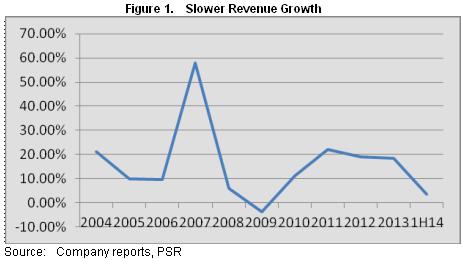

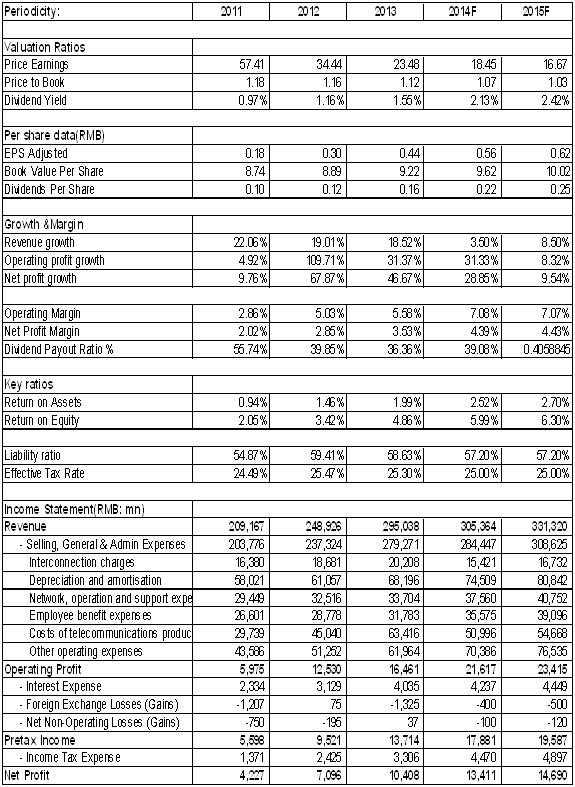

-In the first half year, China Unicom have realized the revenue of 149.57 billion RMB (same as below), only an increase of 3.6%, being the first single digit increase since the financial crisis, which is mainly influenced by the reform of transformation from business tax to VAT in telecommunication industry and keen market competition.

-However, the company's business structure is more optimized. Owing to adjustment of inter-network settlement costs and cutting of mobile phone subsidies make the company's cost expense run at a lower growth speed; and the company's profitability continues to improve which brings along the net profit of 6.69 billion yuan, an yearly increase of 25.8%, which is much higher than the revenue growth speed.

-We expect that the revenue growth speed of China Unicom will slow down. But, the prospect of performance remains optimistic, because the Tower Company has been rapidly established to cut capital expense, and at the same time, the marketing expense will continue to drop, while the profitability of the company is most sensitive to the cut of expense.

-Compared with the first mover advantage of 4G by China Mobile, China Unicom has faced challenges in increasing new users in the first half year. But recently, the company is planning to increase100 thousand 4G base stations by the end of this year. On the basis of strengthening 3G network (about 500 thousand 3G base stations have been established), to deploy LTE network in hot spot zones in large scales; and China Unicom will keep increasing users’ experience, and transplant the 3G advantages to 4G era of which newly added users are expected to grow rapidly. Besides, the company gains an upper hand with its original 3G network and will carry on the strategy of 4G/3G integrated operations. Therefore, construction of 4G networks will enjoy cost advantage.

Investment Action

In general, owing to outside competition of the license granting of virtual network operators, rapid growth of WeChat and other OTTs, as well as inner pressure of the tariff adjustment of operator, China Unicom and other operators are facing much larger market pressure. However, the company enjoys an advantage of differentiated 3G with rich flow operating experience. Investments including construction of 4G base stations will be conducive to the company for re-developing of new users in our opinions. Besides, the company's profitability prospect is better than revenue growth and active exploration of diversified ownership is also expected to bring improvement of operating efficiency and vitality.

3G advantage enables the company to enjoy a higher valuation level than other competitors which should be maintained. We grant it 20X 2014EPS, at a target price of HK$14.2. We upgrade it to “Accumulate” rating.

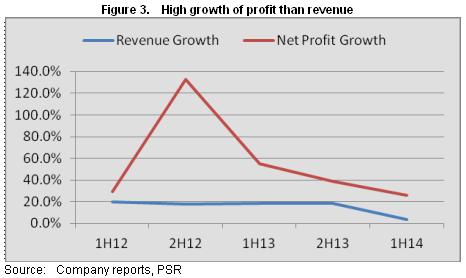

Performance increases by 25.8% in 1H14

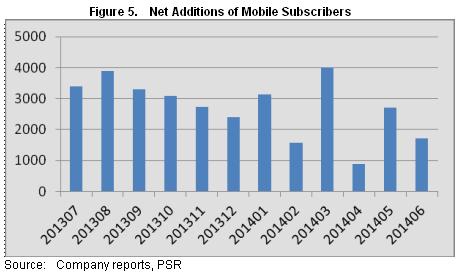

According to the recent interim statements published by China Unicom, the company has realized the revenue of RMB 149.57 billion yuan (same as below) in the first half year, only a yearly increase of 3.6%, which is the first single digit increase since the financial crisis. Taken together, slowing down of revenue growth is mainly caused by the impact of the reform from business tax to VAT in the telecom industry and keen market competition, such as the earlier 4G deployment of China Mobile, and the impact from virtual network operator, Tencent and other OTT businesses. Therefore, net additions of the company's mobile users are declining, and ARPU goes down. In the first half year, the company's blended mobile ARPU value was 47.0 yuan with yearly decreasing of 3.1%, out of which ARPU value of 3G was 68.7 yuan, 11.5% down year-on-year, which was the first time to break 70 yuan.

But, the company's service revenue have realized an increase of 9% to 127 billion yuan of which have maintained the leading position in the industry with 3.4% higher than the average growth rate. While the terminal sales revenue declined by 19% annually. Therefore, the company's business structure has become more optimized, with mobile services accounting for 64% of the operating revenue and non-voice service accounting for 59.5%.

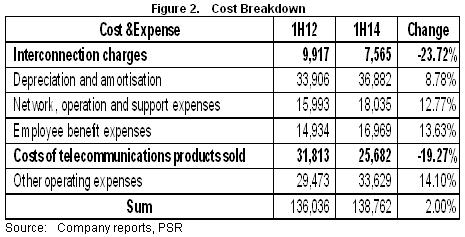

Meanwhile, the company's cost expense increase is lower than the revenue increase, which was mainly benefited from: 1) the adjustment of inter-network settlement cost started earlier this year, such a cost of the company was saved by 2.35 billion yuan at a rate of 23.7%; 2) the subsidy amount for 3G mobile phones was down 21% to 3.33 billion yuan, out of which the subsidy in the second quarter was 1.54 billion yuan of yearly 22.5% down, and quarterly 13.9% down. Finally, the company's profitability continued to improve with EBITDA yearly increase of 13.1% to 47.82 billion yuan of which accounts for 37.6% of the service revenue, yearly increase of 1.4% which have led to net profit of 6.69 billion yuan of yearly increase 25.8%, with the growth speed much higher than the revenue growth, which is corresponding to earnings per share of 0.281 yuan.

Profitability will still win revenue growth

Considering that FDD license for China Unicom is still not opened nationwide and the deployment of 4G is falling behind, as well as the policy of business tax transforming to VAT will not officially start to implement until June. Inevitably China Unicom's revenue growth will maintain a trend of slowing down, and keep a low increase speed of single digit.

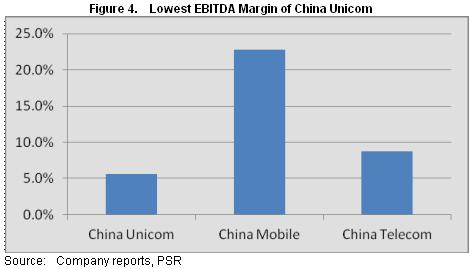

However, we expect that the company's prospect of the performance remains optimistic. Firstly, though the policy of business tax transforming to VAT is expected to decline the profit of almost 40%, the adjustment of inter-network settlement cost basically offsets negative impact. Secondly, along with the rapid establishment of China Communication Facilities Service Limited Company (the Tower Company), the company will reduce the cost for construction of steel towers, supporting facilities, and operation maintenance. As a weak operator, the company will benefit from such a progress and save capital expense. Thirdly, the SASAC has already issued a circular to the three operators, clearly requiring an annual marketing expense cutting of 20% in coming three consecutive years, and this measure is expected to deliver great impact on the operators` mobile phone subsidy, and the three major operators are expected to cut mobile phone subsidy of more than 10 billion yuan in 2014. While in 2013, the expense of mobile phone subsidy by China Unicom was 7.8 billion, accounting for 3.2% of the revenue. It is worthy to mention that China Unicom's profit margin is the lowest among the three major operators, only 5%, while China Mobile is 22%, and China Telecom is 9%. Therefore, the company's profitability is expected to be most sensitive to the cutting of marketing expense.

China Unicom will build 10 thousand 4G base stations

China Unicom had obtained the experimental license for FDD LTE in 16 cities by the end of June, and recently the company has planned to add 100 thousand 4G base stations. In 1H14, the number of the newly built TD-LTE base stations by China Unicom was only 5773, which was not only far behind China Mobile's 300 thousand scale, but also later than China Telecom's progress.

In the first half year, just based on the leading position over 4G license and construction, China Mobile's newly added users have kept growing which have already gained a leading advantage. On the contrary, the number of newly added users of China Unicom has declined. On the basis of strengthening system based 3G networks in future (about 500 thousand 3G base stations have been established), and strengthening the deployment of LTE networks in hot spot zones, China Unicom is expected to increase user's experience, or may transplant the 3G advantage to 4G era, and the newly increased users are also expected to gain rapid development. During the first half year, its traffic operation has gained an edge with yearly data traffic increased 82.1% which is far more than the industry average of 52.1%.

Moreover, although construction of base station will be strengthened, the company still maintains the previous capital expense plan of 80 billion yuan. For one thing, this is benefited from the establishment of the Tower Company, which will help the company save expenses; for another, the company gains an upper hand with its original 3G networks and will carry on the strategy of 4G/3G integrated operations, so it will keep enjoying cost advantages while constructing 4G networks.

The catalyst

FDD license is available nationwide;

Probe into diversified ownership;

Higher-than-expected newly added 4G users and ARPU.

Risks

Intensified competition of 4G charges;

Capital expenditure is higher than expectation.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()