-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

BAIC (1958.HK) - Benefit from Benz's new product cycle

Friday, July 17, 2015  13929

13929

BAIC(1958)

| Recommendation | BUY |

| Price on Recommendation Date | $7.820 |

| Target Price | $13.230 |

Weekly Special - 2333 Great Wall Motor

-BAIC develops her own brands of economical vehicles (namely “Senova” series, “Beijing” series and “Wevon” series) and also possesses the luxury vehicle brand of “Beijing Benz” as well as the medium-high end brand of “Beijing Hyundai”. In 2009, Beijing Automotive Industry Group acquired Saab Technology and applied them on her own brand of “Senova” series passenger cars.

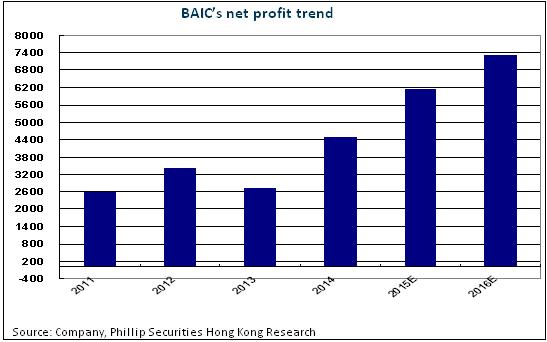

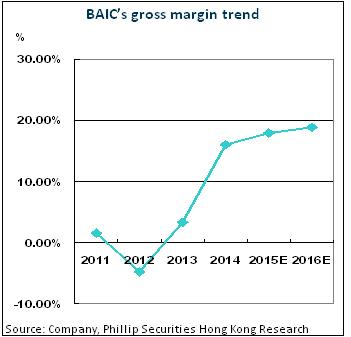

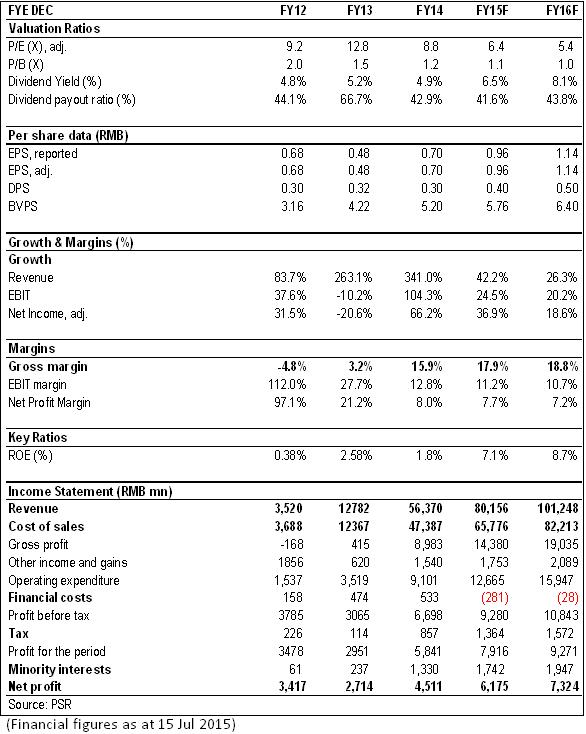

-Last year, the Company's annual income demonstrated a growth of 3.4 times, to RMB56.37 billion. Such surge of income is mainly due to the acquisition of Beijing Benz and the rapid growth of sales of newly launched vehicles. Gross profit margin also increased from 3.2% in 2013 to 15.9% in 2014. Net profit attributable to parent company recorded RMB4.511 billion, up 66% yoy, with corresponding earning per share as RMB0.7 (RMB0.48 recorded in 2013). Boosted by the hot sales of Beijing Benz, its Q115 net profit surged to RMB1.63billion, up 104% yoy, and its gross margin climb to 22.3%.

-Beijing Hyundai is the largest contributor of profit. Beijing Hyundai's two new factories in Cangzhou and Chongqing would commence operation next year, with preliminary planned annual production capacity as 300,000 vehicles each, and expected accomplishment by 2016 year-end and 2017 year-end respectively. Beijing Hyundai's total production capacity would possibly increase to 1,650,000 vehicles in the future. This can provide an effective solution to the current problem of production bottleneck.

-Benz has entered into a new product cycle since 2014H2, with the new C Class Benz marked a kick-off. Benz launched the new SUV model of GLA in April 2015, and will further introduce the brand new GLK in 2015Q4. Moreover, the new E Class sedans will be launched in 2016. Benz set her target to regain the top rank in the global luxury vehicle market by 2020 and Beijing Benz is benefited from her long-term expansion business strategy. We expect Beijing Benz would start a period of rapid growth from 2015 to 2017.

-The self-owned brands of BAIC Motor would launch Senova X65, Senova D80, Senova X55, Senova C33 and Senova CC etc in 2015. The proportion of SUV will be amounted to 20% approximately. SUV will be the major growth momentum of the Company's self-owned brands, and this would help to lower the loss incurred from BAIC Motor's self –owned brands.

Investment Thesis

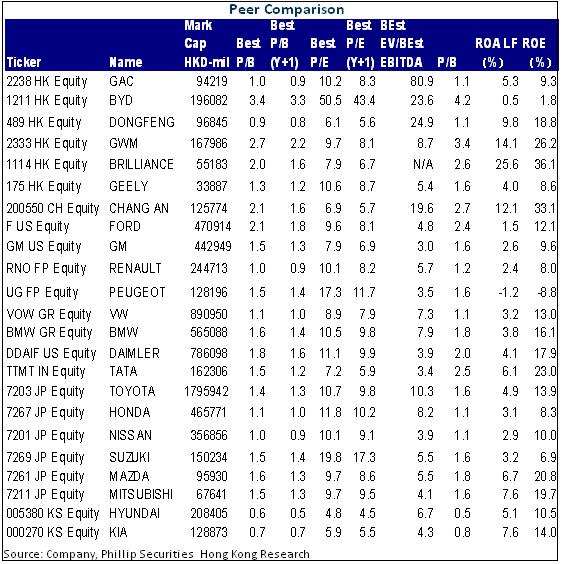

We expect the 2015/2016 revenue of the Company to be RMB80.2 billion and RMB101.2 billion respectively; and the forecasted EPS to be RMB0.96 and RMB1.14 respectively, with benchmarking companies including Brilliance Auto, BYD Auto, Great Wall Motor and Geely Automobile. We expect the valuation of the Company's share to be 10.8x of 2015 expected P/E and 9.1x of 2016 expected P/E respectively, and grant the rating of “BUY” for the first time, with the target price of HKD13.23. (Closing price as at 15 July 2015)

Company Profile

BAIC Motor (1958.HK) is the main platform for the business of passenger car manufacturing of Beijing Automotive Industry Group Company Limited, which develops her own brands of economical vehicles (namely “Senova” series, “Beijing” series and “Wevon” series) and also possesses the luxury vehicle brand of “Beijing Benz” (which joined BAIC Motor as a subsidiary on 17 November 2013) as well as the medium-high end brand of “Beijing Hyundai”. In 2009, Beijing Automotive Industry Group acquired Saab Technology, including the structural design, engine transmission gear box and production mode of three types of Saab vehicles, which was applied on the production of comparatively high-end own brand of “Senova” series passenger cars.

The Company has diversified production lines, covering mid- to large-size sedan, mid-size sedan, compact sedan, small-size sedan, SUV, MPV and CUV products. The holding shareholder of the Company, Beijing Automotive Industry Group, ranks the fifth largest automotive group in China and holds approximately 45% of the Company's equity. Daimler AG and Shougang Limited also hold 10% and 13.54% of the Company's equity respectively.

Acquisition of Beijing Benz and speedy growth of self-owned brands are the main causes of surge of business

Last year, the Company's annual income demonstrated a growth of 3.4 times, to RMB56.37 billion. Such surge of income is mainly due to the acquisition of Beijing Benz and the rapid growth of sales of newly launched vehicles. Boosted by the acquisition of Beijing Benz, the Company's gross profit margin also increased from 3.2% in 2013 to 15.9% in 2014. Net profit attributable to parent company recorded RMB4.511 billion, up 66% yoy, with corresponding earning per share as RMB0.7 (RMB0.48 recorded in 2013).

Even facing the adverse situation of growth slowdown of the automotive market in 2014, the Company's self-owned brands, Beijing Benz and Beijing Hyundai recorded a total sale of 1,575, 200 vehicles, up 17% yoy. Among this total sale volume, Beijing Hyundai contributed 71.1%, while Beijing Benz and Beijing series vehicles contributed 19.7% and 9.2% respectively. With respect to the pace of growth, Beijing series vehicles and Beijing Benz recorded growth rates of 2014 sale volume of 53.1% and 25.4% respectively, far higher than the average growth rate of the Chinese automotive industry. Meanwhile, Beijing Hyundai recorded a growth rate of sale volume of 8.7%.

Beijing Hyundai is the largest contributor of profit

Beijing Hyundai offers a full series of SUV products namely Santafe, ix35, Tucson and ix25, targeting at various markets of high-end, medium-end and low end; and thus achieving a full coverage of SUV products priced between RMB120,000 to RMB210,000. In the market of sedans, Beijing Hyundai would launch new models including Sonata 9, brand new ix35 and Mistra1.6T in 2015. Beijing Hyundai's two new factories in Cangzhou and Chongqing would commence operation next year, with preliminary planned annual production capacity as 300,000 vehicles each, and expected accomplishment by 2016 year-end and 2017 year-end respectively. Beijing Hyundai's total production capacity would possibly increase to 1,650,000 vehicles in the future. This can provide an effective solution to the current problem of production bottleneck.

Beijing Benz starts new product cycle

Benz has entered into a new product cycle since 2014H2, with the new C Class Benz marked a kick-off. Benz launched the new SUV model of GLA in April 2015, and will further introduce the brand new GLK in 2015Q4. Moreover, the new E Class sedans will be launched in 2016. Benz set her target to regain the top rank in the global luxury vehicle market by 2020 and Beijing Benz is benefitted from her long-term expansion business strategy. We expect Beijing Benz would start a period of rapid growth from 2015 to 2017. Contribution of profit from Beijing Benz would gradually increase in the future, with sale volume and profitability rising continuously.

Loss from self-owned brands may decrease

The self-owned brands of BAIC Motor would launch Senova X65, Senova D80, Senova X55, Senova C33 and Senova CC etc in 2015. The proportion of SUV will be amounted to 20% approximately. SUV will be the major growth momentum of the Company's self-owned brands, and this would help to lower the loss incurred from BAIC Motor's self –owned brands. Furthermore, the Company's passenger cars using new energy under self-owned brands recorded the sale volume of 5892 vehicles in the first half of the year. Such leading sales figure ranked the third in the Chinese market. The current end-user sales demonstrated a situation with supply shortfall and high demand. The burst of demand for vehicles using new energy is expected to be indicated in this year's business of the Company.

Investment Thesis

We expect the 2015/2016 revenue of the Company to be RMB80.2 billion and RMB101.2 billion respectively; and the forecasted EPS to be RMB0.96 and RMB1.14 respectively, with benchmarking companies including Brilliance Auto, BYD Auto, Great Wall Motor and Geely Automobile. We expect the valuation of the Company's share to be 10.8x of 2015 expected P/E and 9.1x of 2016 expected P/E respectively, and grant the rating of “BUY” for the first time, with the target price of HKD13.23.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()