-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Guangzhou Baiyunshan Pharma (874.HK) - Share of Wong Lo Kat Continued to Expand

Tuesday, October 18, 2016  26481

26481

Guangzhou Baiyunshan Pharma(874)

| Recommendation | Buy |

| Price on Recommendation Date | $19.160 |

| Target Price | $24.480 |

Weekly Special - 2333 Great Wall Motor

Share of Wong Lo Kat Continued to Expand

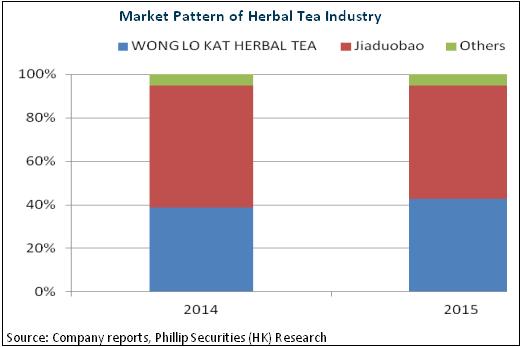

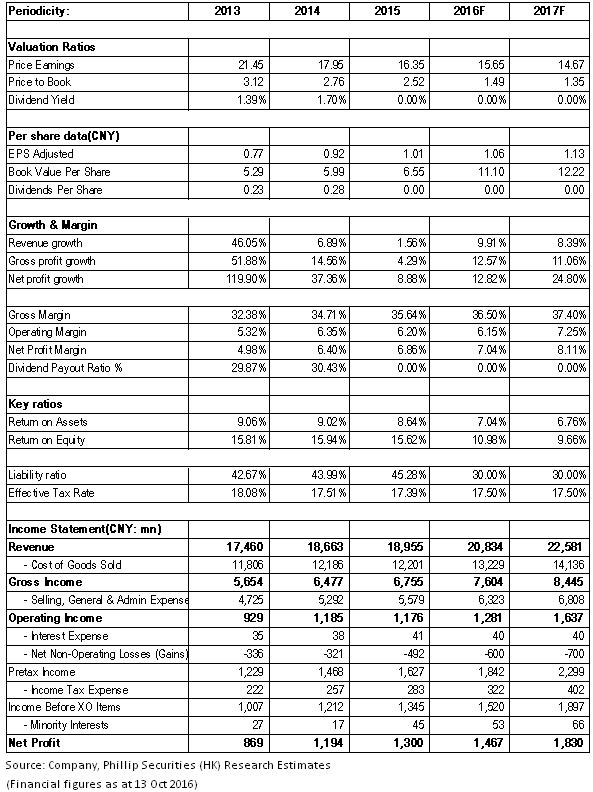

In 1H16, the company's Great Health business focusing on Wong Lo Kat saw sound development, and its revenue increased by 7.6% to RMB4.7 billion. Specifically, the Q2 revenue witnessed a QoQ increase of nearly 20%. Overall, Wong Lo Kat has recovered the sole right to use the trademark, advertisement, red can packaging and formula assets, contributing to increasingly obvious competitive edge and continued expand in market share. Jiaduobao has changed red cans into gold cans, and hence may lose some of the festive market share. In the meantime, it significantly reduced marketing expenses and changed the management this year. By contrast, Wong Lo Kat will increase terminal investment by virtue of considerable funds, so it is expected to continue enhancing competitive advantage.

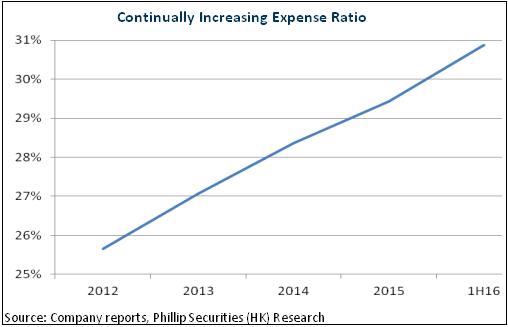

Additionally, we are optimistic about the improvements in profitability of Wong Lo Kat. Previously, the expense pressure on the two competitors was immense. Net profit margin of Wong Lo Kat plunged from about 20% to less than 5%, far lower the industry. Nevertheless, presently Jiaduobao emphasizes cost control and reduces advertising investment, so the expense pressure on the two parties was alleviated, and the profitability of Wong Lo Kat is projected to improve. In 2015, net profit margin of Wong Lo Kat rose by 0.23 percentage points to 5.03%.

Grand Southern TCM Business is Expected to Recover

In spite of an increase of over 60% in the revenues of An Gong Niu Huang pill and Jin Ge, the revenue of the company's Grand Southern TCM segment dropped by 7.9% to RMB3.5 billion in 1H16, which was mainly because of the influence of de-stocking by distributors and relocation of such enterprises as Qi Xing Pharmaceutical Factory. However, the improvement in product structure resulted in an increase of 3 percentage points in gross profit margin of Grand Southern TCM to 45.4%. Furthermore, with the relocation and reconstruction of pharmaceutical factories and completion of de-stocking, better performance in the second half of 2016 is expected.

It is worth mentioning that Pfizer's patent protection on Viagra expired. Increase in the company's Jin Ge lived up to expectations. Jin Ge is RMB34.5/pill, 73% cheaper than Viagra, which is RMB128/pill. Besides, the company continues to build drug sales network after private placement. Therefore, we expect that the market share of Jin Ge will significantly increase, and the sales may exceed the original target of RM B300-400 million in 2016.

The Government Participated in Private Placement with Heavy Investment

The company completed the private placement, with the non-public offering price of RMB23.56/share and the total size of RMB7.9 billion. The Guangzhou Municipal Government invested RMB7.3 billion, showing its firm support to the company. The company, as the only pharmaceutical listed platform of Guangdong SASAC, is likely to gather pharmaceutical resources. Additionally, the shareholding by YF Capital would also introduce the resources of Alibaba, so the company may speed up the efforts to promote regional medicine integration in the future.

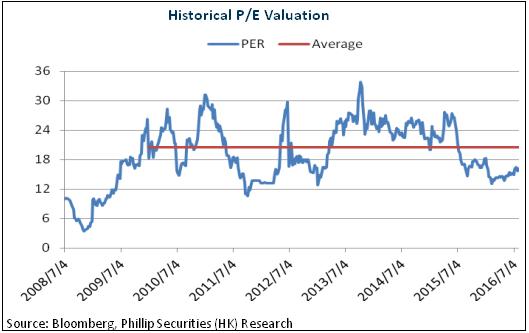

In conclusion, the company's Grand Southern TCM segment is projected to recover. The profitability of the Great Health segment will be improved, and the Great Commerce segment will witness constant and rapid growth due to policy changes. We grant it 20x EPS in 2016 and the target price of HK$24.48, with the "Buy" rating initially. (Closing price as at 13 Oct 2016)

Risks

Competition of consumer goods market is more intense;

Integration of Grand Southern TCM segment fails to meet expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()