-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of October 2013

Friday, November 1, 2013  4638

4638

Report Review of October 2013

Weekly Special - 2333 Great Wall Motor

Industry:

Local property and Others (Dennis), Mainland financial, Utilities (Xingyu Chen), Mainland (Fanguohe),Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing),

Local Property (Dennis)

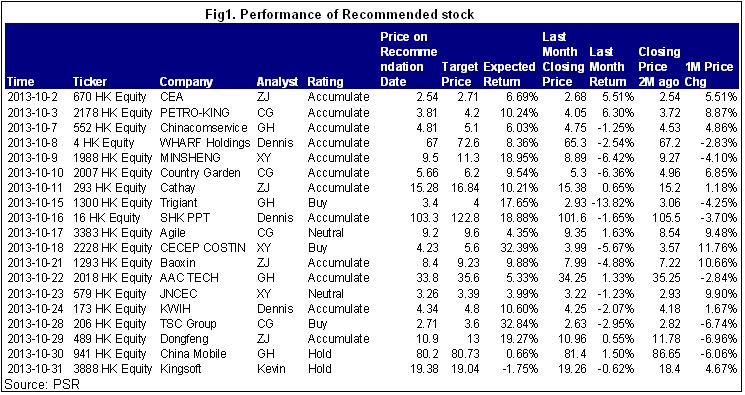

In October, we initiated research report on Wharf Holdings (0004.HK), and updated Sun Hung Kai Properties (16.HK), and K. Wah Int`l(173.HK).

Wharf Holdings (0004.HK): We initiated research report on Wharf, Wharf's earnings from China investment properties are increasing. We want to highlight that Wharf is developing 5 International Finance Square (IFS) in China with total GFA of ~2.0 mn sqm (~5.7 times of current completed China IPs size). Chengdu IFS, Wharf's next flagship development modelled on Harbour City in HK, will open in Jan 2014 and the project is expected to fully complete in 3Q14. The pre-leasing of retail area is satisfactory with 92% pre-leased as of June 2013. The tenant mix is quite diversified from luxury brands, Prada, Chanel, LV to UNIQLO, PAGEONE, food court, etc. Management expects annual rental income of RMB500 mn when fully operational, which is almost half of current level. We think positive on the Chengdu IFS based on decent retail demand (satisfactory pre-leasing) and grade A office demand ( >90% occupancy rate in Chengdu grade A office). We estimate the Chengdu IFS will drive operating profit from China IPs by ~45% in FY14. We give a TP of HK$72.6, based on 25% target discount to our FY14 NAV estimate (~0.4 s.d. above the long-term average).

Sun Hung Kai Properties (16.HK): SHK re-launched 181 units of The Cullinan in West Kowloon, a HK residential project, recently (~60% of the unsold units). SHK will provide several types of discount to up to 14% (3% to SHKP Club member, 2% for not applying a second mortgage loan, 9% from early completion cash rebate). We want to highlight that SHK provide special cash rebate, 70% of total amount of stamp duty (including ad valorem stamp duty and buyer's stamp duty) to purchaser who signed on or before 31 Oct 2013. With the special cash rebate, the discount will be nearly 30% of the asking price. This strategy aimed to attract the mainland and company buyers. Although the aggressive price cut will hurt the margin, the impact will not be big due to the low land cost of The Cullinan. We expect the operating margin will be still >40%.

We expect SHK to continue the similar strategy for the upcoming projects, especially the luxury projects, to accelerate asset turnover, which will offset the margin compression and reduce the earning risks. We retained the same TP of HK$122.8, based on 30% discount to our FY14 NAV estimate of HK$175.4 (vs. historical average NAV discount: 16.4%). The major upside potential will be the faster-than-expected asset turnover.

K. Wah Int`l (173.HK): We held an investor presentation at our office on 17 Oct, 2013 and invited K. Wah management as speaker. Here are some key takeaways: 1.) Even the land cost in first-tier cities of China such as Shanghai is high now, K. Wah management said they would continue to submit tender if the price is reasonable. K. Wah's gearing ratio was 19% only and has cash or equivalent of HK$4.45 billion as of June, 13, which will support the land replenishment opportunities. 2.) Management said they have no plan to sell equity interest in Galaxy Ent (27.HK) under healthy balance sheet and low gearing ratio. K. Wah holds 3.9% stake in Galaxy Ent, which accounted for 30.5% of K. Wah's GAV in our estimate. 3.) We revised our NAV estimate up by 8.3% to HK$10.4 per share to reflect the higher valuation of Galaxy Ent (27.HK). We remained the same target NAV discount of 53.4%, same as the long-term average. We raised TP by 8.2% to HK$4.82.

Mainland Financial (Xingyu Chen)

HSI showed the adjustment in October after the strong growth in September, HSI increased slightly compared with September, above 23,000 by the end of this month. During the period, the large weighted sectors such as banking, and insurance appeared the better performance in general. Most of Chinese banks` prices went up slightly compared with the beginning of this month, especially increased strong this week, mainly because the market still holds an optimistic view of the sector after 3Q results announced in the last week of this month.

According to the quarterly results, the banks` performance meets our expectation, the profit growth of domestic listed banks slowed down due to the stronger competition in deposit market with the interest rate liberalization, and the small and medium-sized banks gained the higher growth rates. Net profit growth rates were between 6.27% and 14.91% in the first three quarters, of which ABC owned the highest as 14.9% with the lowest as 6.27% of CMBC, decreased significantly. The main reasons of the decrease of profits were the slow-down of interest and intermediate business incomes. For instance, BoCom's NIM down 0.03ppts in 3Q, and recorded 2.53%, decreased by 0.07ppts y-y. Its quarterly net profit dropped around 19%. Additionally, net commission fee of ICBC declined 15% q-q. CITIC Bank is the only one to gain the increase of NIM among the small and medium-sized banks.

However, domestic economy declined after the financial crisis in the U.S. in 2008, and started to affect the real economy from last year, especially, the bad debts appeared in Zhejiang Province among the small and medium-sized banks. By the end of 3Q, the asset quality of domestic banks continued to deteriorate, most of the banks` NPLs increased and only CRCB realized the dual decrease of the ratio and amount, and CMB recorded the largest growth of the NPLs. However, some banks` NPL ratio maintained stable or decreased slightly due to the large settlement and write-off of the bad debts this year.

As at the end of 31 October, CMB's share price has the best performance among 9 domestic listed banks with the growth of 9% in Oct, and CMBC recorded the worst one, decreased by 4% at the same time. Overall, we still hold a cautiously optimistic view for the banks` development, and maintain Buy rating to the sector.

Mainland Telecom (Fanguohe)

Overall speaking, the telecom sector has basically taken akin tendency to HSI. Benefiting from the optimistic expectation of 4G license issue in October, it achieved a rise in the first half. However, many companies have eased in the second half. Besides the failing of license issue, they were also suppressed by the weak market and the first fall of China Mobile's performance in 3Q13.

In our view, the sector will still show weak in short term, but investors can buy in the pullback. First, the capital expenditure of the three operators will accelerate in 4Q13, China Mobile and China Telecom have taken collective bidding and purchasing for 4G, which will help relative companies achieve better performance than the first half in 2013. Second, the award of 4G licenses will still be a positive catalyst for the sector.

Mainland Property & Oil/Gas service (Chengeng)

In October, 2013 I wrote four research reports on Country Garden, Agile, PKOS and TSC, which got success by unique operation model. We recommend TSC. TSC Group is an excellent enterprise in Chinese marine industry. The company shows its considerable competitiveness in technology strength, development strategy and company governance. At present, TSC Group is at the stage of technology and market cultivation, therefore, many financial data are not desirable in the short term. But from the transformation occurring to the company, we can see that TSC Group will enter the stage for a new round of rapid growth. We predict that there will be a substantive breakthrough in the international order of TSC Group in the next three years, and it can be expected that its performance and market share will see a remarkable increase. Although there is a bigger fluctuation in the share price of the company, TSC is still a value investment target with lower risk coefficient in medium-to-long term. Therefore, we give TSC Group a "Buy" rating and a target price of 3.6 HKD per share in the next 12 months, 15.8 times of the forward PE in 2014.

Automobile (ZhangJing)

In August, we updated 4 research reports including China Eastern Airline (670), Cathay Pacific (293), Baoxin Auto (1293) and Dongfeng Group (488). We recommend Cathay Pacific and Dongfeng firstly.

Affected by the strong demand of long-haul routes and major tourist routes in Asia, there was a good beginning of the peak season in summer holiday in 3Q with the high load factor in economy class. To satisfy with the recovery of the demand, Cathay began to increase more flights, and all cancelled long-haul routes last year are restored by Sep. 2013, or increase the route frequencies, including Los Angeles, New York, Toronto and London. Overall, we believe the recovery of the Company's passenger part will be accelerated in 2H compared with 1H, and lift our target price for 12 months to HK$16.84, equivalent to 25/17/14xP/E and 1.1/1.1/1.0xP/B in 2013/2014/2015 respectively. We reiterate “Accumulate” rating.

Benefited from the low y-y base and the newly introduced cars during the period began to take effect, sales of passenger car of Dongfeng Group in September increased by 52% y-y to 193,700 units, 30% m-m. Dongfeng Nissan and Dongfeng Honda have outstanding performances. There are eight new models to be introduced in 2H, including five new models and three face-lifted ones. We believe after nearly one year's adjustment, with the continuous recovery of Japanese brands market and the introduction of more new cars, it is the probability of large events that Dongfeng's achievements in the second half will get substantial improvement. Our target price for 12 months of HK$13 is based on 8.9/8.2/7.8xP/E and 1.4/1.3/1.3xP/B in 2013/2014/2015 respectively, which is the lowest valuation among peers in HKEx. We give it “Accumulate” rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()