-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Chow Tai Fook Jewellery (1929.HK) - Resilient Business Performance in 1HFY2023, resume normalcy become a positive catalyst

Tuesday, January 3, 2023  1557

1557

Chow Tai Fook Jewellery(1929)

| Recommendation | Accumulate |

| Price on Recommendation Date | $15.800 |

| Target Price | $17.220 |

Weekly Special - 1810 Xiaomi

Resilient Business Performance in 1HFY2023

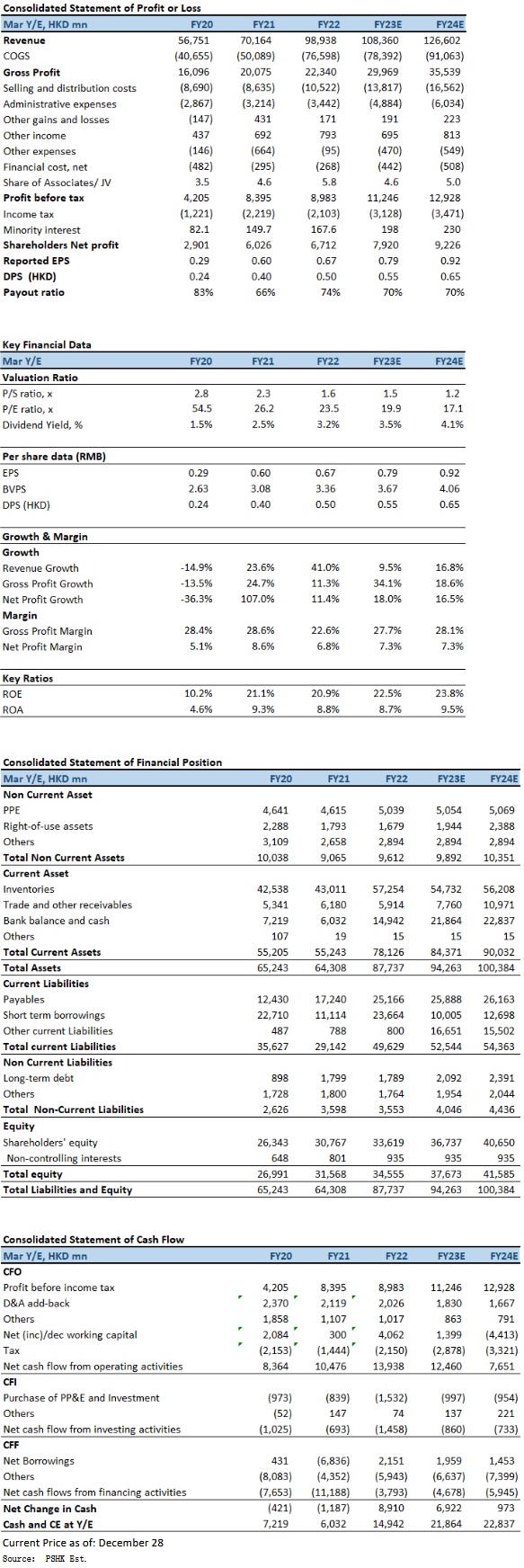

Chow Tai Fook Jewellery (CTF) revenue grew 5.3% to HK$46,535mn in1HFY2023. Revenue growth was driven by the steady expansion of retail network and robust demand for gold jewellery and products in the Mainland. Gross profit increased 1.6% to HK$10,962mn. Adjusted gross profit margin declined to 22.4% from 23.5% in the same period last year, mainly attributable to a higher share of our wholesale business and gold jewellery and products. Core operating profit was down by 2.7% to 4,349mn due to the flourishing wholesale business and a higher contribution from gold jewellery and products. Profit attributable to shareholders decreased by 6.8% to HK$3,336mn, mainly due to a net foreign exchange loss 268.9mn (1HFY2022: net gain of 46.6mn) arising from the weakening of RMB. EPS was HK$0.33, with an interim dividend of HK$0.22 per share in 1HFY2023, representing a payout ratio of approximately 66.0% (1HFY2022: 61.4%).

MAINLAND CHINA MARKET

Revenue in the Mainland was up 6.2% to HK$40,927mn in 1HFY2023. On a constant exchange rate basis, revenue increased by 9.3% in the period. Same Store Sales (SSS) dropped by 7.8% YoY (SSSG turned positive in 2QFY2023, and RSV increased by 28.0% YoY). SSS of gold jewellery and products was down 3.3% YoY. ASP of the product category increased to about HK$5,500 during the period (1HFY2022: HK$5,200). SSS of gem-set, platinum and k-gold jewellery dropped 13.9% during the period. Gem-set jewellery ASP climbed to approximately HK$7,500 (1HFY2022: HK$7,200).

As at 30 September 2022, there are 6,547 POS in Mainland China (4,929 franchised CHOW TAI FOOK JEWELLERY POS). Wholesale (mainly represents sales to franchisees and provision of services to franchisees) share in revenue expanded 630 basis points to 55.0% in the period. During the period, CTF opened a net of 933 CHOW TAI FOOK JEWELLERY POS in the Mainland (with approximately 90% of the net openings were franchised POS). RSV of franchised POS in the Mainland grew robustly by 29.2% YoY, and the growth was faster than that of the self-operated POS. E-commerce channel in the Mainland delivered an encouraging RSV growth of 15.1%. Its share to the RSV in the Mainland was steady at about 5.0%. In terms of retail sales volume, its share was about 13.0%. Its ASP was approximately HK$1,800 during the period (1HFY2022:HK$1,900).

HONG KONG & MACAU OF CHINA AND OTHER MARKETS

Revenue in Hong Kong, Macau and other markets was down by 0.5% to HK$5,608mn. Share to the Group's revenue amounted to 12.1%. Although retail revenue was improving in Hong Kong, wholesale revenue decreased by 25.1% mainly due to the pandemic-control measures in Hainan Province, which constrained the sales from duty-free business. SSSG increased by 1.3% YoY, while SSS volume growth was down by 8.7%. SSS of gold jewellery and products was up 6.1% in 1HFY2023, outperforming other product categories. ASP of the product category enjoyed an upward trend and reached about HK$7,000. SSS of gem-set, platinum and k-gold jewellery dropped 6.9% in the period. Yet, on a quarterly basis, it rebounded to positive growth in the second quarter. ASP of gem-set jewellery also increased by about 18% to HK$16,400. 89 POS in Hong Kong & Macau of China, closed a net of 3 POS. 43 POS in Other markets, while opened a net of 2 POS.

Investment Thesis

Management expected that 3QFY2023 performance to continue subdued as it was in 1QFY2023, mainly due to the prolonged impact of COVID in mainland China, and guided a high single digit sales decline in mainland China during 2HFY2023. However, some new products would be launched in during peak periods of consumption in Q4, and expect to help stabilize the sales. Management guided SSS growth of low-single-digit to mid-single-digit in mainland China, and teens growth in Hong Kong & Macau in FY2024. As the company expected to focus on improving store efficiency and growth quality, the number of net store openings will slow down to 600 to 800, and it is expected that FY2024 sales growth will be low-to-mid-teens. In addition, the company targeted to increase the proportion of self-operated stores in next year (higher gross profit margin than franchised), and with the help of product upgrade (the launch of the new Wonderful Life Collection) and reduced discounts, it is expected that there would be continued improvement of the overall core operating profit margin. We expected that there would be signs of recovery month-over-month in mainland China SSS since restrictions were gradually relaxed. We maintain FY2023-FY2024 EPS to be HKD0.79 and HKD0.92 respectively (reported on September 5, 2022), but considering that the return to normalcy in the Mainland will be a relatively positive catalyst, we raise the PT to HKD17.22, implies a FY2023E P/E of 21.7x (one standard deviation above 2-yrs historical average). Our investment rating is upgraded from “Neutral” to “Accumulate”.

Risk factors

1) Resurgence of COVID in Mainland China bring prolonged impact; 2) Sharp fluctuations in FX and gold price; 3) Economic recovery momentum slower-than-expected, consumer confidence weak; and 4) higher-than-expected operating costs.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()