-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Traditional Chinese Medicine (570.HK) - Destocking of Chinese Traditional Medicine Basically Ends

Wednesday, January 25, 2017  21161

21161

China Traditional Chinese Medicine(570)

| Recommendation | Buy |

| Price on Recommendation Date | $3.600 |

| Target Price | $5.080 |

Weekly Special - 2333 Great Wall Motor

Concentrated Chinese Medicine Granule (CCMG) Market Access Liberalization Remains to Be Seen

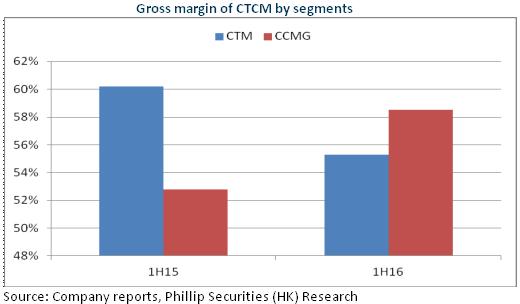

After the acquisition of Tianjiang Pharmaceutical in 2015, China Traditional Chinese Medicine (CTCM) has taken the leading position in the domestic CCMG sector. Overall, with outstanding security, effectiveness, convenience and the sustained 15% drug-price addition policy, CCMG may take a part of the Chinese traditional medicine market. Also, currently all TCM hospitals are eligible to sell CCMG, while in the past only those of secondary or above levels did. The CCMG market will maintain high growth, and the company, as a leader, will benefit from its expansion.

Previously only five enterprises produced CCMG, but the market-access policies are likely to be loosened, causing market concerns about disorderly competition. We believe, against the backdrop of the supply-side structural reform, CCMG national standards will be set relatively high in order to ensure TCM quality and protect the brand. Furthermore, within the three years (2017-2019) during formulating the industry standard guidelines, all companies in the industry will be encouraged to conduct research and develop industry standards for more than 500 CCMG products, which only five enterprises are able to sell at present. New manufacturers can only sell CCMG products after meeting the industry standards during the transition period, and are required to undergo a six-month production stability test prior to commercial production. Therefore, we expect new entrants to have very limited impact on the current market pattern.

CTCM has enhanced its core competitiveness through R&D, with the research of high-performance liquid chromatography (HPLC) of more than 150 varieties completed, and will continue to improve corporate internal quality standards. In the meantime, the company will support CCMG's high profitability through the centralized procurement of 105 medicinal materials. In addition, the CCMG marketing network has nearly covered all provinces in China, among which 18 provinces have recorded a sales volume of over RMB100 million. With the further marketing reform in such aspects as academic promotion and incentive system, the marketing advantage of CCMG will be consolidated. It is notable that the company plans to invest RMB2 billion in the next three years to expand production capacity, of which extraction capacity will rise from 28,500 tons to 60,000 tons and granulation capacity from 8,000 tons to 16,000 tons, and this will further enhance the company's scale edge and consolidate its leading position.

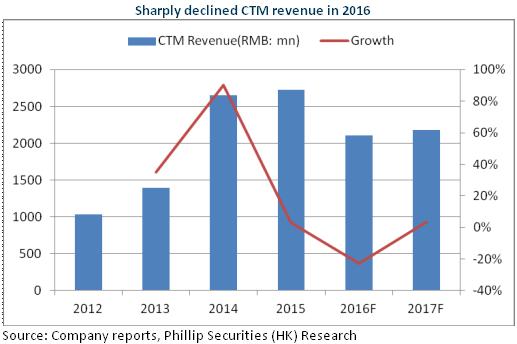

Destocking of Chinese Traditional Medicine Basically Ends

In H1, the revenue and net profit from the company's original Chinese traditional medicine business fell by 19.5% and 32.9% to RMB1.14 billion and RMB160 million, respectively, due to the introduction of "two invoices" policy and medical insurance cost control and reduction of inventories in channels, as well as the drop in tender price of the company's products by 3 to 4% on average, and the second bargain in some provinces. In H2, the deepening of destocking led to the decline in drug products over 20% YoY and the scale shrinkage triggered the sharp fall in profits.

However, currently destocking pressure has been basically released, with distributors` channel inventory falling from 4 months turnover at the end of 2015 to around 2 months, and the inflection point has appeared. We expect, in 2017, the company's Chinese traditional medicines will develop steadily, or even resume single-digit growth.

Valuation Reaches Margin of Safety

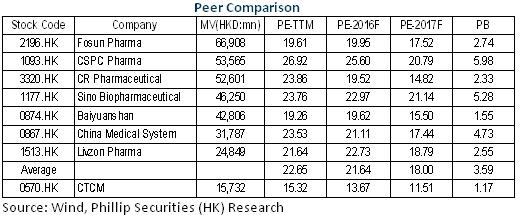

The company has resumed dividend and will maintain a payout ratio of more than 30%, which is expected to enhance the market recognition. We adopt the Sum of the Parts Valuation (SOTP), and give the company's CCMG business and Chinese traditional medicine business 20X P/E ratio and 10X P/E ratio, respectively. The target price is HK$5.08, with the "Buy" rating. (Closing price as at 23 Jan 2017)

Risks

Further price drop in products;

Competition intensifies more than expected.

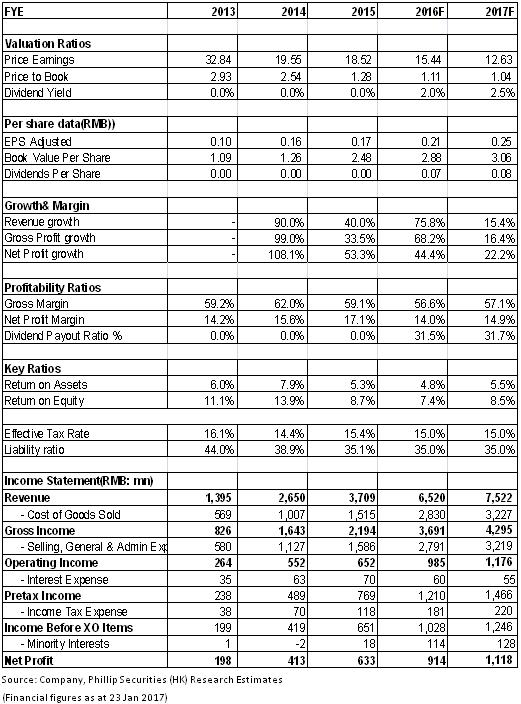

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()