-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

AAC Technologies (2018.HK) - Non-acoustic products continue to grow

Thursday, November 19, 2015  9416

9416

AAC Technologies(2018)

| Recommendation | Neutral |

| Price on Recommendation Date | $55.050 |

| Target Price | $54.640 |

Weekly Special - 3606 Fuyao Glass

The revenue of AAC Technology in the first three quarters of 2015 increased by 36.51% yoy, to RMB 7.891 billion; while gross profit and net profit in the period under review increased by 36.38% (to RMB 3.278 billion) and by 37.06% (to RMB 2.096 billion) respectively. The EPS in the first three quarters amounted to RMB 1.71. Main reasons of the increase in revenue lie on the technological upgrade of the Company's products and the new solutions for clients causing an increase of orders of both acoustic and non-acoustic products. Domestic clients` demand for upgrading speakers kept recovering. The excellent sales performance of Apple iPhone6S/6S+ and Apple Watch boosted the business expansion of haptics faster than expected. The proportion of non-acoustic business has exceeded 40% of the revenue.

With the need of brand development by domestic mobile phone producers, the enhancement of acoustic devices would continue, so that the prices and profitability of related products may improve as a result. In the aspect of acoustic device production, AAC Technologies will not only gain from the consistent growth of proportion of Chinese clients in the global market, but also be benefitted from the extension of the Company's technology from high-end mobile phones to mid-/low-end ones.

The non-acoustic products continue to grow. We expect that flagship products launched by producers of mobile phones with Android system, which include smart phones, tablet PCs and wearable devices will still be extensively equipped with haptics. As AAC is the leading company in the production of haptics, it is expected that CAGR of the income from haptics would exceed 30%. Moreover, the Company's RF antenna integrated solutions is getting popularity among domestic clients, and it will become the key momentum of growth.

The prospect still bright

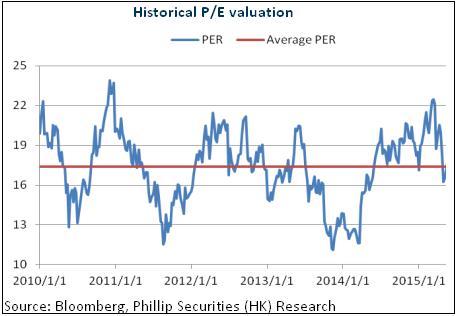

Historically, the business performance of AAC Technologies demonstrated seasonal features. This year the Company is benefitted from the driving force of high unit-priced non-acoustic products, the results in H2 may further beat expectation. Having considered the upgrade of acoustic equipment and the leading advantages of non-acoustic products, we keep our optimistic view towards the development of the Company. Since the Company produced speaker devices for smart phones, the Company's valuation ranged between 11x to 22x of P/E, with average of 17.4x. Taking into account of the development prospect with persistent growth, we grant the Company a valuation corresponding to 18x of 2015e EPS, with the target price of HKD54.64, and the rating of “Hold”. (Closing price as at 17 Nov 2015)

Q3 results beat expectation

The revenue of AAC Technology in the first three quarters of 2015 increased by 36.51% yoy, to RMB 7.891 billion; while gross profit and net profit in the period under review increased by 36.38% (to RMB 3.278 billion) and by 37.06% (to RMB 2.096 billion) respectively. The earning per share in the first three quarters amounted to RMB 1.71. In Q3, the Company recorded the revenue of RMB 3.18 billion, up 32.5% qoq; while net profit in Q3 increased by 33.2% qoq, to RMB 851 million. The earning per share in Q3 was RMB 0.69.

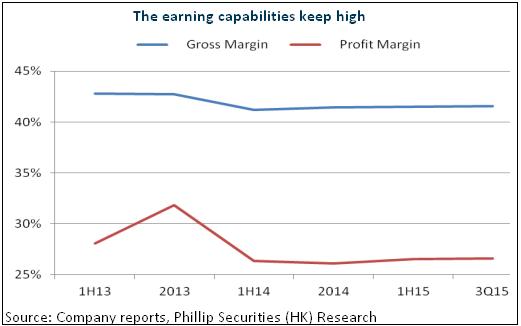

Overall, the business of the Company consistently demonstrated strong growth which beat market expectation. Main reasons of the increase in revenue lie on the technological upgrade of the Company's products and the new solutions for clients causing an increase of orders of both acoustic and non-acoustic products. Domestic clients` demand for upgrading speakers kept recovering. The excellent sales performance of Apple iPhone6S/6S+ and Apple Watch boosted the business expansion of haptics faster than expected. The proportion of non-acoustic business has exceeded 40% of the Company's revenue. In terms of profitability, the Company's gross profit margin in Q3 raised by 0.1 ppts qoq, to 41.6%, which reflected the enhancement of the Company's product structure.

Acoustic products kept upgrading

Even though the market of smart phones is heading towards its ceiling, among the signature high-end models by producers like Huawei, Xiaomi etc., the new generation of speaker devices with better acoustic performance and new features (for example, waterproof function) has become more and more well-received by consumers. Some of the high unit price speaker devices supported the income growth of acoustic business of the Company. In our views, with the need of brand development by domestic mobile phone producers, the enhancement of acoustic devices would continue, so that the prices and profitability of related products may improve as a result. In the aspect of acoustic device production, AAC Technologies will not only gain from the consistent growth of proportion of Chinese clients in the global market, but also be benefitted from the extension of the Company's technology from high-end mobile phones to mid-/low-end ones. Moreover, the Company started production plants in Vietnam since 2014, with the number of staffs expanded 10 times from the initial number of 350. Diversification of production base can also serve to lower production cost, and thus enhance profitability.

Non-acoustic products continue to grow

Pressure-touch and haptics are becoming the key trend for interaction between users and phone devices. Benefitted from the outstanding performance of haptics, non-acoustic products can almost contribute half of the Company's revenue. Even though Apple cut the number of orders for components in Q4, it is expected that flagship products launched by producers of mobile phones with Android system, which include smart phones, tablet PCs and wearable devices will still be extensively equipped with haptics. As AAC is the leading company in the production of haptics, it is expected that CAGR of the income from haptics would exceed 30%.

Moreover, the Company's RF antenna integrated solutions is getting popularity among domestic clients, and it will become the key momentum of growth. Although the Company entered the market of mobile phone metal casing at a later stage, it can provide integrated solutions which include metal casing and RF antenna. Meanwhile, most of the Chinese OEM producers in this aspect have inadequate resources on research and development. Therefore, the gross profit margin of business of integrated solutions was as high as 40%, and the Company just ranked second only to Catcher Technology.

Catalyst

Better-than-expected development of non-acoustic business;

Better-than-expected growth of domestic customers.

Risk

Worse-than-expected decline of orders from Apple;

Intensified market competition and decline of selling prices of products.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()