-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Mengniu (2319.HK) - Acquisition of Bellamy helping milk powder business development; maintaining whole financial year's guidelines

Thursday, October 24, 2019  7059

7059

Mengniu(2319)

| Recommendation | Accumulate |

| Price on Recommendation Date | $31.200 |

| Target Price | $34.600 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

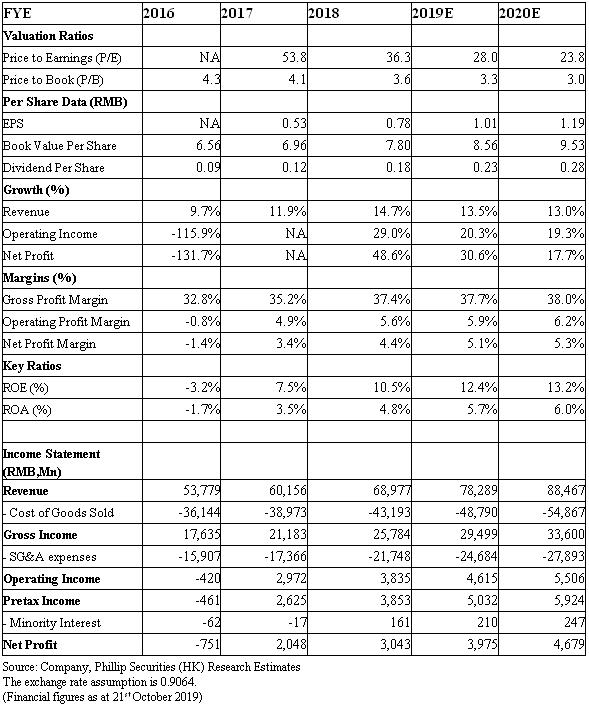

Mengniu announced that it intends to acquire Bellamy's Australia at a price of no more than AUD1.46 billion (HKD7.86 billion), with a planned share of AUD12.65 per share. Bellamy's net profit after tax is AUD21.7 million in FY2019. The P/E ratio is 67 times. Bellamy is Australia's first organic milk powder brand. It is listed on the ASX. It is a global recognised brand and has operations in Australia, New Zealand, China and Southeast Asia.We believe that the acquisition will be highly complementary to Mengniu's existing infant formula business, which will help Mengniu expand China and overseas markets. Organic IMF enjoys significantly faster growth and higher margins compared to the overall IMF market. Bellamy's gross profit margin of FY 2019 reached 43.5%, and the EBITDA rate reached 17.6%, both higher than Mengniu. Bellamy's FY 2018/2019 revenue fell 19% y.o.y. to AUD266 million, mainly due to the slower-than-expected approval of China's milk powder formula registration, and the e-commerce law. Mengniu said that after the acquisition, it will closely communicate with the relevant departments to assist Bellamy to accelerate the registration approval.

Mengniu's revenue in 1H of FY2019 increased by 15.6% y.o.y., if excluding Junlebao, the growth rate was 13%. Up to 9.5% of revenue growth came from sales volume growth, and the rest was the increase in ASP, mainly due to faster growth of basic products. The management team still maintains the guidance of the whole year, with low double-digit growth in revenue (including Junlebao, which will be finished disposal in 2H. Operating profit margin improved by 50 points in 1H and is expected to be maintained in 2H. Gross profit margin decreased by 0.1 ppt y.o.y. to 39.1%, while GPM was flat excluding Junlebao. Raw milk price rose by 5 to 6%, higher than management team's expectation. But thanked for the product mix optimization, the high-end milk business is growing rapidly. The prices of other raw materials fell, and the tax rate has also had a positive impact, which led to an improvement in operating profit margins.

After the announcement of the interim results, the stock price was under pressure. The market worried that the price of raw milk would remain high, and the market competition continued, which put pressure on operating profit. We believe the increase of raw milk price will help the performance of Modern Dairy (1117.hk) to resume. Mengniu's product mix will continue to be optimized, and it is expected that GPM can be maintained. After the completion of the disposal of Junlebao, profit margin can be improved. In 1H, the liquid milk business, which accounted for 83% of total revenue, increased by 14.4% y.o.y., the milk powder business increased by 43.8%, and ice cream decreased by 2.4%. For the liquid milk business, the market share of UHT products and chilled yogurt increased compared with the same period of last year. The former increased by 0.5 ppt to 28.5%, and continued to rank the second in the market. The latter increased by 1.3 ppt to 34.5%, and continued to be the market leader. For the e-commerce liquid milk category, the market share increased by 0.9 ppt to 24.6%, which also ranked the first in the market.

During the period, the income of Milk Deluxe and Just Yoghurt which belong to the room temperature product business increased by 20% and 24% respectively, and Fruit Milk Drink also recorded double-digit growth, while the basic white milk business increased by 19%. During the period, Milk Deluxe had been launched fully revamped packaging, Just Yoghurt had been launched new flavor products, Fruit Milk Drink had been launched high-end products. The chilled product business has also introduced new packaging and a variety of new products. We give a forecast PE of 31 times and target price of HKD34.6. (current price as of 21st October, 2019)

Valuation and risk

We are optimistic about the industry and the company's prospects, thus give forecast PE ratio of 31 times and target price of HKD34.6. Potential risks include failure to meet revenue growth, lower profit margins than expected, and huge fluctuations in raw milk prices. (current price as of 21st October 2019)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()