-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Kangmei Pharmaceutical Co., Ltd. (600518.CH) - Layout in the Entire Industrial Chain of Traditional Chinese Medicine

Tuesday, December 23, 2014  29174

29174

Kangmei Pharmaceutical Co., Ltd.(600518)

| Recommendation | BUY |

| Price on Recommendation Date | $16.220 |

| Target Price | $19.800 |

Weekly Special - 002472.CH Shuanghuan Driveline

Steady Growth of Performance

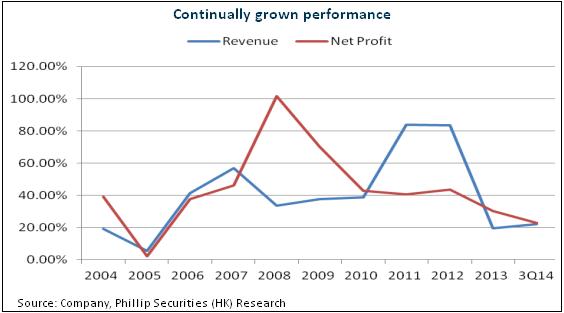

Kangmei Pharmaceutical is a large modern medical resource-based enterprise and a national key high-tech enterprise with the production of traditional Chinese medicinal decoction pieces as its core and the businesses covering the entire industrial chain of traditional Chinese medicine. By virtue of rich resource layouts and channel advantages and so on, company revenue and net profit from 2001 to 2013 were recorded with the compound growth of respectively 30%+ and 40%+. Since 2014, the company has continued its steady and robust growth, mainly benefiting from the high increases of traditional Chinese medicinal decoction pieces, western medicine trade and health products and food businesses.

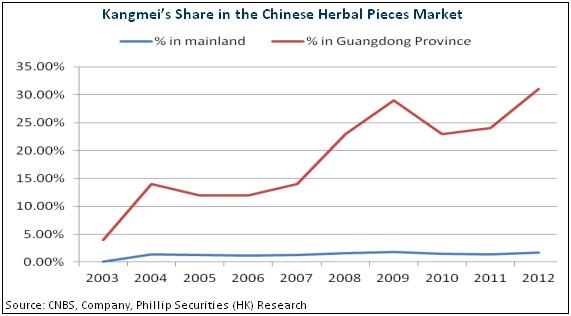

Kangmei has basically penetrated the upstream, midstream and downstream industries of the industrial chain of traditional Chinese medicine, up to medicinal herb cultivation and trade, down to production and development and terminal sale, which is gradually forming the control of the resources and circulation market of traditional Chinese medicinal herbs, and enjoys the advantage with its leading position in the same trade, and may obtain a certain right to speak in the field of traditional Chinese medicine.

The company has built a multi-channel marketing network. Kangmei has become the second listed pharmaceutical enterprise involved in direct marketing, plus the professional advantage of its direct marketing group. It is expected that the direct marketing channel will realize geometric growth, up to above one billion. In addition, e-commerce business of the company also steps into a fast lane, further forming an all-round sale pattern, which is expected to boost the acceleration in the growth of various businesses.

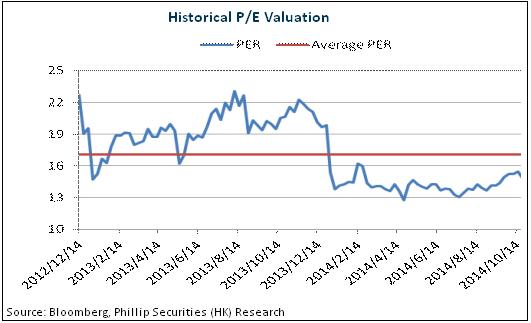

Valuation stands at a low level compared to the peer

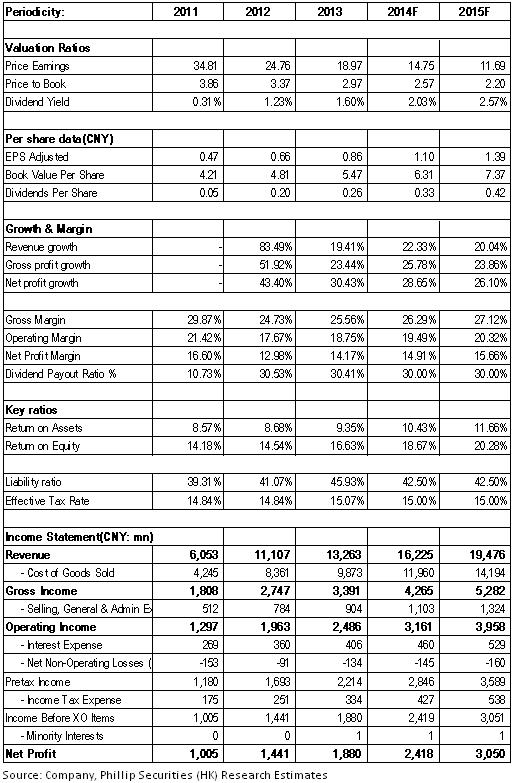

The company possesses an advantage of the entire industrial chain of traditional Chinese medicine. The capacity bottleneck of decoction pieces is gradually being eliminated, downstream consumer products have a rapid increase, and e-commerce platforms will also provide channel support, which make continuous growth hopefully. Currently, its valuation corresponding to the performance of 2014 is less than 15 times, a low point in the industry. We grant it 18X 2014EPS, and the target price can be CNY 19.80, with “Buy” rating initially.

Steady Growth of Performance

As shown in the third-quarter report in 2014 of Kangmei Pharmaceutical, the recorded business revenue in this period was CNY 11.577 billion yuan, with the year-on-year growth of 22.16%; the net profit belonging to shareholders of the listed company was 1.498 billion yuan, with the year-on-year increase of 8.02% and the earnings per share of 0.681 yuan; and net profit excluding non-recurring items was 1.482 billion yuan, with the year-on-year rise of 7.53%. It is worth mentioning that on October 10, the company got again the notice about the continuation of high-tech enterprise. If it is estimated with a tax rate of 15%, the company's net profit, in fact, increases at an annual rate of 22%, maintaining a relatively high growth speed.

Specifically, the company's traditional Chinese medicinal decoction pieces, Western medicine trade and health food businesses have realized high increases. Firstly, the revenue of the traditional Chinese medicinal decoction pieces in the first three quarters had a year-on-year rise of 50%, continuing the growth acceleration compared with the increase of 39% in the first half year. At present, Beijing production base of traditional Chinese medicinal decoction pieces has acquired GMP certificate. It is expected that the capacity of 6,000 tons will be put into production successively. Bozhou base and other bases are also handling procedures such as production authentication. Secondly, benefiting from hospital pharmacy trusteeship, the revenue of Western medicine trade business had a year-on-year increase exceeding 80%. Thirdly, the revenue growth of health products was about 100%. The direct marketing business of the company in cooperation with the PICC was offically launched, with the revenue contribution being over 200 million yuan in the first three quarters.

Meanwhile, the company's profitability remained steady, the combined gross margin reduced by 0.15 percentage points, marketing expense ratio basically kept balance, management fee rate reduced by 0.23 percentage points and financial fee rate increased by 0.24 percentage points.

Layout of the Entire Industrial Chain of Traditional Chinese Medicine

In recent years, Kangmei has actively implemented a strategy of the entire industrial chain of traditional Chinese medicine and has begun to take shape, occupying a leading position in the sector. The company has built GAP and standardized planting bases with an area exceeding 50 thousand mu in Yunnan, Sichuan, Jilin, Gansu and so on, involving pseudo-ginseng and Panax ginseng, etc. And it has set up nine production bases of traditional Chinese medicinal decoction pieces in Guangdong, Beijing, Shanghai, Sichuan, Jilin, Anhui, Gansu and so forth. Thus, a nationwide production layout is basically completed.

In addition, the company has merged and acquired professional markets of traditional Chinese medicinal herbs in Bozhou, Anhui, etc., the newly-built national largest Kangmei (Bozhou) Huatuo International Chinese Medicine City has been put into use, and currently the company has managed the professional trading markets of traditional Chinese medicine which occupy over 75% of the national trading volume. At the same time, the company newly builds Kangmei Hospital, merges and acquires and integrates many domestic public hospitals, and trusts nearly one hundred hospital pharmacies. Furthermore, it invests the construction of Ophiocordyceps Sinensis Global Trading Center in Xining, Qinghai Province and builds Sino-ASEAN Kangmei Yulin Chinese Medicinal Herbs (Spices) Trading Center in Yulin, Guangxi Province. Generally speaking, Kangmei Pharmaceutical has basically penetrated the upstream, midstream and downstream industries of the industrial chain of traditional Chinese medicine, up to medicinal herb cultivation and trade, down to production and development and terminal sale, which is gradually forming the control of the resources and circulation market of traditional Chinese medicinal herbs, and may obtain a certain right to speak in the field of traditional Chinese medicine.

Build A Multi-Channel Marketing Network

Apart from traditional channels, the company also obtains national direct marketing business license and becomes the second listed pharmaceutical enterprise involved in direct marketing. In light of the rarity of direct marketing license, the company’s direct marketing group possesses professional advantages. We expect that its direct marketing channel is hopeful to realize geometric growth, achieving a level of over one billion yuan.

Meanwhile, the e-commerce business of the company also steps into a fast lane. Since a large trading platform of traditional Chinese medicinal herbs (e Medicine Valley) was launched online, depending on more than 30 warehousing logistics centers nationwide, the company has established nearly 20 standards of listed variety, with the business electron plate reaching over 10 billion yuan. Meanwhile, subsidiary "Kangmei Mall" and O2O trading platform of traditional Chinese medicinal herbs "Kangmei Chinese Medicine City" have also been put into operation online. Generally speaking, the company has constituted an all-round sale pattern including hospital direct supply, OTC selling, wholesale distribution, chain store selling, terminal retail, e-commerce, direct marketing and so on, which is expected to boost the acceleration of the growth of various businesses.

Catalyst

Newly-added capacity of traditional Chinese medicinal decoction pieces is released rapidly;

The growth in the fields of health products and foods exceeds expectations;

The expansion of direct marketing channel is faster than expectation.

Risks

The trading business of medicinal herbs has excessively great demand for cash flow;

The scale of projects in process is enormous.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()