-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Suntien Green Energy (956.HK) - Stable growth with moderate expansion

Tuesday, May 27, 2014  6728

6728

China Suntien Green Energy(956)

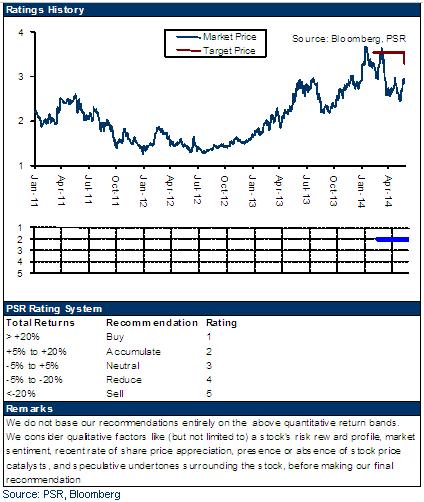

| Recommendation | Accumulate |

| Price on Recommendation Date | $2.850 |

| Target Price | $3.300 |

Weekly Special - 603179.CH Xinquan

Introduction of the company

The Company was jointly established in February 2010 with contribution by HECIC, and it focuses on the sales of natural gas and the development and utilization of wind power in Hebei Province, meanwhile, it is also specialized in the development of other new energy technology. The Company was listed in the Hong Kong Stock Exchange in October 2010.

Summary

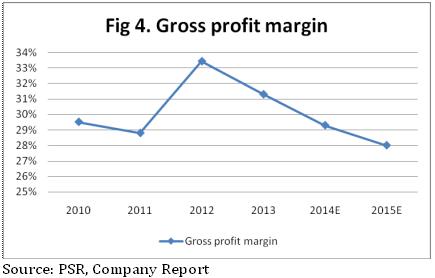

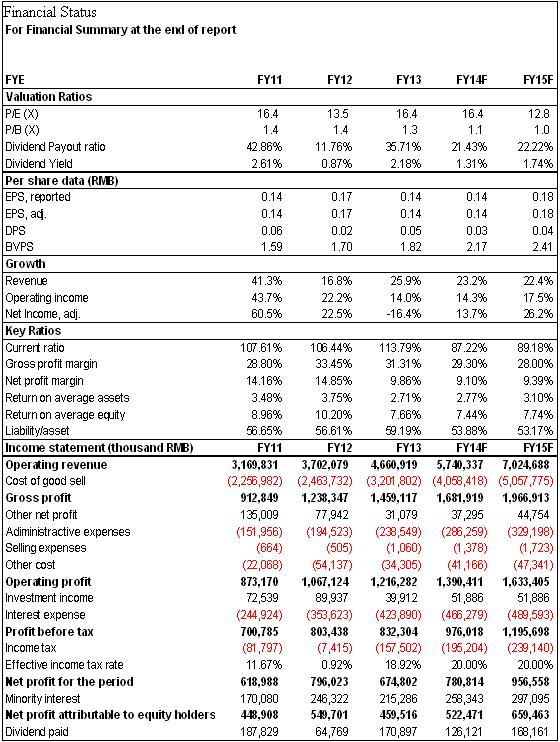

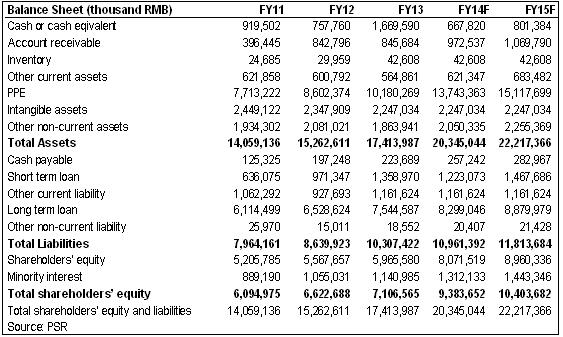

-The Company's annual revenue amounted to RMB4.66 billion, up 25.9% y-y, benefited from the sales growth of natural gas and the increase of wind power generating capacity. Net profit reached to RMB460 million, down 16.4% y-y, which was mainly because of the large decrease of net CERs income and the increase of income tax, the profit was lower than our expectation.

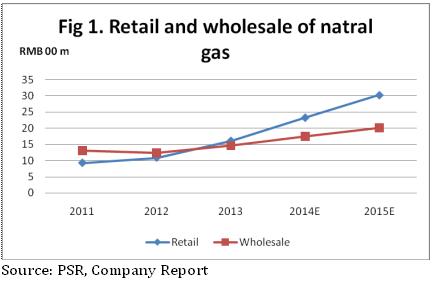

-The Company's sales volume of natural gas increased by 19% y-y to 1,484 million cubic meters, and newly added industrial and residential users increased by 21% and 33% y-y respectively, the retail business increased faster while the wholesale business grew stably.

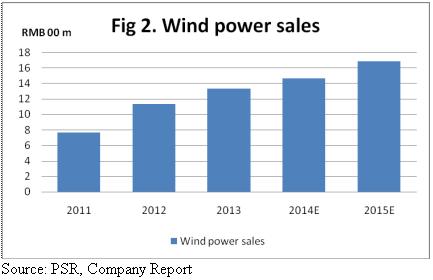

-The power generation of the Company's wind farms reached to 2,927 million KWh in 2013, up 15.8% y-y. Abandoning rate trended to go down nationwide except Hebei Province, representing the effects of the growth of power constraints due to the accelerated construction of new wind power projects. We believe the utilization hours of the Company in 2014 will be lower than that of 2013.

-The construction of the Company's natural gas projects goes smoothly, besides the pipeline construction, there are 2 CNG primary filling stations, 2 CNG refilling stations and 1 LNG refilling station have commenced. The Company has 7 projects in the fourth approved list of the Twelfth Five-year Plan with the amount of 485MW, and Sichuan, Guangxi, and Xinjiang each have one project besides Hebei, and the Company will do the preparations for the preliminary stage of wind power projects in Shandong, Yunnan, and Henan, which means the Company starts to expand the wind power business not only in Hebei but also in the whole country.

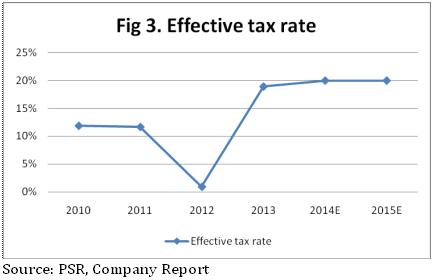

-The Company's income tax amounted to RMB158 million in 2013 with the effective tax rate of 18.9%, compared with RMB7 million with the tax rate of 0.92% in 2012, which was mainly because of the expiration of the preferential policies of the Company's natural gas projects, the tax rate will increase to 25%, and there are no duty free treatment for 3 wind farms any more. The income tax rate may continue to go up considering the expiration of the preferential policies of the Company's projects in future.

-Overall, the Company's businesses developed stably, both the sales of natural gas and the wind power operation business maintained the growth between 15% to 20%, and there is stronger consumption demand of natural gas in future due to the industrial structural adjustment in Hebei Province, but the Company also faces the risks in the decrease of wind power utilization hours and the income tax growth. We combine the valuation of the companies in both wind power operation and natural gas sales, give the Company's 12-month target price to HK$3.30, equivalent to 19/15xP/E in 2014E/2015E respectively, and recommend Accumulate rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()