-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

KINGSOFT CORP LTD (3888.HK) - Concern on the sustainability of high growth in Internet business

Monday, May 12, 2014  9925

9925

KINGSOFT CORP LTD(3888)

| Recommendation | Neutral |

| Price on Recommendation Date | $22.000 |

| Target Price | $21.420 |

Weekly Special - 002050 Sanhua

Company Profile

Kingsoft is a leading Internet-based software companies in China. It provides online games, Internet security software, office software and cloud services. Group has in-house software development team, and provides application software services through their own Internet platform. In online games they have the famous “JX series” as the flagship product for many years and attracted millions paying players. For Internet security and office software, there are Kingsoft Anti-Virus and WPS Office. Products are mainly sold in the mainland China, but also exported to Hong Kong, Macao, Taiwan and Southeast Asian countries.

Financial Highlights

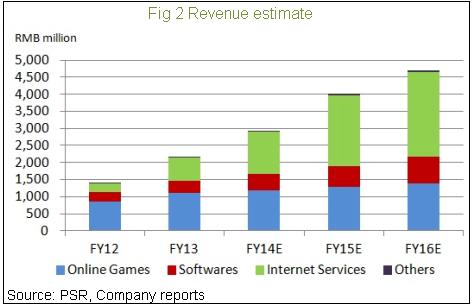

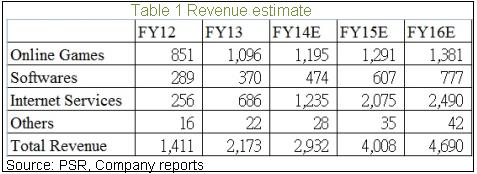

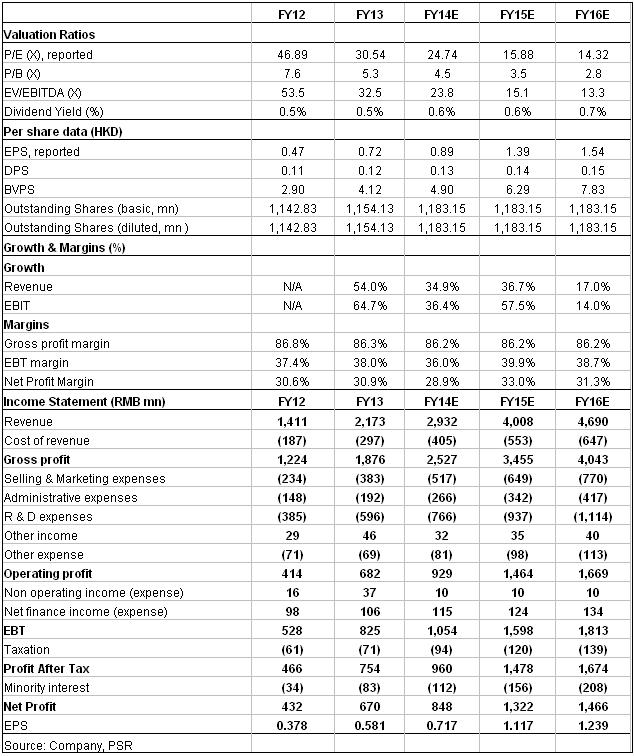

The revenue rose by 54% yoy to RMB 2.173 billion (as below) for FY13, which revenues from online games increased by 28.7% to $1.096 billion and from application software surged 94% yoy to $1.056 billion. Gross profit increased by 53.3% to $1.876 billion, the gross profit margin was about the same of 86% as before. Operating profit was $682 million, an increase of 65% while profit attributable to shareholders was $671 million, an increase of 55%. Final dividend was HK$ 0.12. Kingsoft's performance for last year was excellent, especially in the Internet services and software, both achieved significant increase in sales.

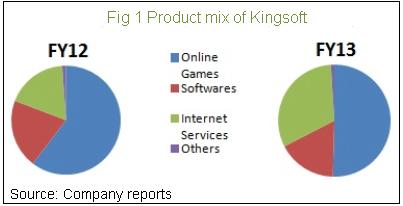

Changes in product mix, the Internet service will become the main source of revenue

Compared to the previous financial year, the product mix for FY13 has changed significantly. In FY12, revenue from online game was a major source of revenue for the company, accounted for 60%of the total revenue; followed by the software business, 20% of total revenue; Internet services, including Internet security software, online platform and mobile applications, consist of only 18% of the total revenue. However in FY13, revenue from online game was $1.096 billion, accounted for 50% of total revenue; software revenue as $370 million, 17% of the total while revenue from Internet service surged to $686 million, as of 32% of total revenue.

It is expected in the next few years, the revenue from Internet service will continue to rise. The proportion will increase to 45% to total revenue in FY14, which will become the largest source of income. In FY16, there will be a further rise to 53%.

One thing to mention, the revenue from Internet service in FY13 was $686 million, a substantial increase of 168% from $256 million. But this increase may due to the rapid growth in online sales for “Double Eleven Shopping Festival” (Single Festival), and increase revenue from KIS game platform. Therefore it is expected

1) Despite that there will still be impressive sales volume in this year's Shopping Festival, the growth is difficult to compare with last year; 2) The growth will mainly achieved by KIS game platform and its mobile Internet applications.

And the sales of office software, benefited by the PRC government's policy of protecting legitimate software which required to use the legitimate software in the public organizations. This stimulated the sales of WPS Office software and software business is expected to have nearly 30% annual growth in the coming years.

Steady growth in the online game business, good cost controls

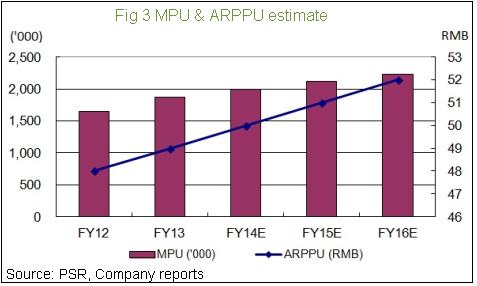

For FY13, company's online game business recorded 28.7% growth, mainly due to the ten consecutive quarters growth of its flagship game "JX 3". In the fourth quarter of FY13, "JX 3" had published its additional patch, led to its daily average peak concurrent users (DAU) increased by 3% qoq to 630 thousands, but a slightly decline yoy. As of the end of FY13, the average monthly paid users (MPU) was 1.87 million, an increase of 13% yoy and 4% qoq. However, compared to peak 2,000,000 paying users in summer, it could not fully regain the lost ground. The average monthly revenue of paying users (ARPPU) slightly increased 2% to RMB 49. It was expected the future online gaming revenue will grow slowly, with an average annual growth rate ranging from 7% to 9%.

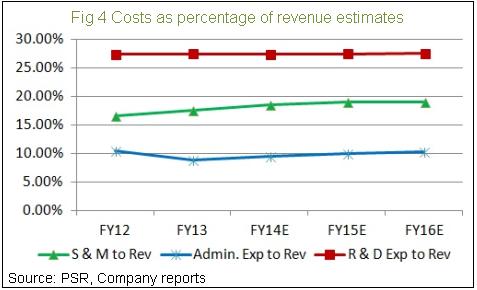

Despite the rapid growth in total revenue, expense to revenue did not increase significantly. Research and development expenses rose 55% to $596 million, sales and marketing expenses increased by 64% to $383 million and administrative expenses increased by 30% to 192 million. The overall expense to revenue rose only according to its operating income, reflecting the company's good cost control.

Spin-off of Cheetah Mobile Inc, focus on Internet and mobile services

Kingsoft spin-off its former Kingsoft Internet Software (KIS) Holdings Ltd, renamed to Cheetah Mobile Inc. (CMI) and applied for the initial public offering of American Depositary Shares in NYSE, which was priced at US$ 14 and started to trade on board on May 8. According to company reports, CMI shall not engage in games and software research and development, or operation of its self developed games. CMI will mainly engage in information security software, web browser. Its main mission is to develop and operate mobile games and applications, and provides online advertising services and Internet value-added services. After the spin-off of CMI, Kingsoft's voting power on CMI remains unchanged, but the stake will decrease 7.1% to 47%. Therefore, the profit attributable to non-controlling interests will increase, resulting to profit attributable to Kingsoft's to reduce accordingly.

In addition, Kingsoft has also announced its subscription of 31.94 million of Xunlei Series E preferred shares, representing 9.98% of the total shares that had been issued. These preferred shares were convertible at any time to Xunlei Series ordinary shares. The subscription was to strengthen Kingsoft's Internet services penetration rate.

Valuation

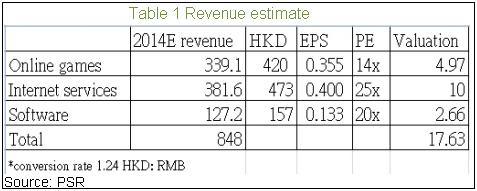

We believe that the market valuation of over 40x P/E of Kingsoft at the beginning of this year is indeed too high. Despite of supportive government policy for its software business and the high growth in Internet business, the revenue growth of Internet service in FY13, in partly due to a substantial increase in online sales for the Single Festival last year. Besides, the market estimate on Kingsoft's mobile Internet revenue was just over-optimistic. Given the recent market volatility, the out-performing stock last year dropped significantly recently, and investors begin to pay attention to the high valuation of IT stocks. After re-examine the valuation, we estimate the 6-12 months target price for Kingsoft to be HK $ 21.42, which is 24 times of FY14 forecasted earnings and give rating as "neutral". This is calculated by the valuation HK $ 17.63 for operation and HK $ 3.79 for cash.

However, in the long run, HK $ 21.42 is only equaled 15.4 times and 14 times of the forecasted earnings in FY15 and FY16 respectively. It is expected the long-term valuation will rise back to the around 20 to 25 times.

Potential risks

Revenue from online games decrease

Internet business growth slows down

After the spin-off Cheetah Mobile, revenue affected by reduction in stake

Costs and expenses increase more than expected

Financial Status

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()