-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

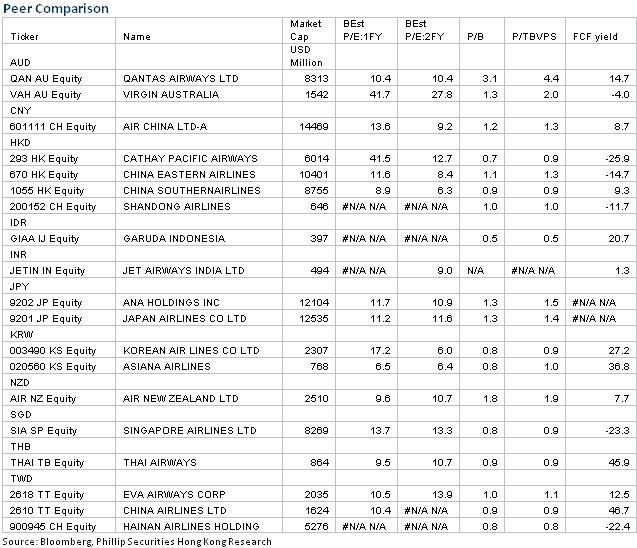

Cathay Pacific (293.HK) - 2018H result review: Maintain the TP and Rating

Monday, August 27, 2018  8426

8426

Cathay Pacific(293)

| Recommendation | Accumulate |

| Price on Recommendation Date | $12.320 |

| Target Price | $14.300 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

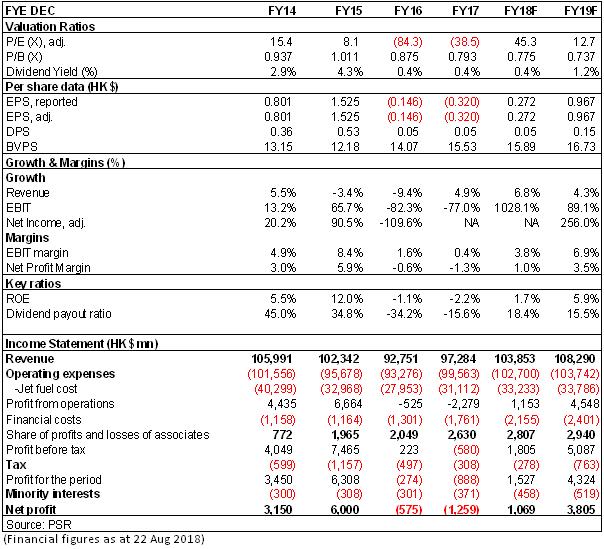

Sound demand rebound and mild cost growth make Cathay's 2018H1 loss shrinking by near 90% yoy. We believe that the Company's H2 result prospects are mixed with recovery of demand continually and the moderate cost growth. The positive factor is the gradually fading fuel hedging losses, and the negative factor is the shrink of share of profit from Air China due to the exchange losses. We temporarily maintain the financial forecast and target price unchanged at HK$14.3 for the Company, reaffirming the accumulate rating. (Closing price as at 22 August 2018)

Nearly 90% reduction of Losses in 2018H, Recovering Distributing the Interim Dividends

Cathay recently announced interim results, and the total revenue rose 15.7% to HK$53.08 billion yoy in the first half of 2018, recording a loss of HK$263 million, HK$1.788 billion less yoy, a loss of 6.7 cents EPS, and an interim dividend of 10 cents.

Fuel Costs Increased, But Fuel Hedging Losses Decreased Sharply

Fuel costs increased by 7.4% during the period as the gasoline price went up by 28% and the fuel consumption by 2.1%. But some of the increase was offset by an 80% reduction in fuel hedging losses. In addition, the Company invested more and more fuel-efficient new models to reduce fuel consumption per revenue ton kilometre by 2.5%.

Operating Profits Turn Positive

Since 2016H2, the Company has recorded three consecutive six-month operating losses. In 2018H1, driven by a 15.7% yoy increase in total revenue and an 8% increase in operating expenses, the operating profit turned from negative to positive again, reaching HK$697 million. However, the net financial expenditure overspent nearly HK$200 million or 24% yoy to HK$1 billion, and profit that should account for the affiliated company decreased by HK$0.84 billion. Finally, profit of the shareholders still recorded a small loss.

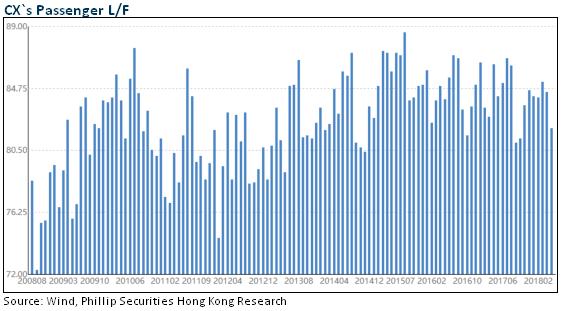

Passenger Yield Improves

During the period, the increase of passenger capacity (+3.2%) was faster than that of the number of passengers (+1.9%). The P L/F decreased gently by 0.5ppts to 84.2% yoy. However, due to the improvement of revenue management, the increase of fuel surcharges, and strong demand for first class and business class, the yield of passenger transport rose 7.6% to 55.4 cents yoy, and overall revenue of passenger increased by 10.4% to HK$35.45 billion.

Freight Keeps a Strong Momentum

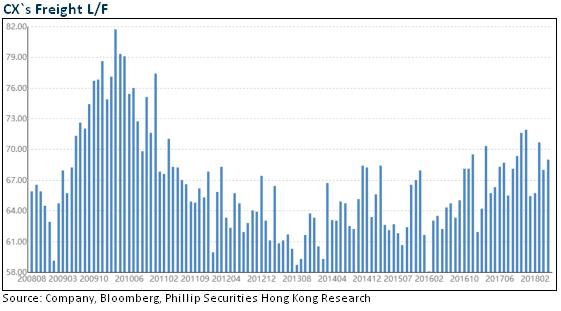

Increased demand for specific cargo shipment and the movement of higher value goods to and from Asia led to a sharp rise in freight yields of 16.3% yoy to HK$1.93. And overall freight revenue increased sharply by 23.4% yoy to HK$12.97billion. The growth of cargo tonnage (+7.5%) continued to be stronger than cargo capacity investment (+4.1%) and the cargo L/F increased by 2.1 ppts yoy to 68.3%.

The Tree-year Transformation Program Has Passed a Half

The three-year enterprise transformation plan has passed a half. During the period, the Company restructured the team structure of its headquarters, appointed a new management and leadership team to implement a series of cost control measures, and achieved some results. The basic cost per ton kilometer (except fuel) increased by only 3.3%, from HK$2.13 to HK$2.20. The management said the Company also plans to move toward simpler, more efficient and other directions, but it will also make investment expenditure for future development, such as hiring more staff and enhancing cabin services to improve customer experience.

Operating Data Maintain Good, Keeping the Target Price Unchanged

Cathay's operating data for the first seven months of 2018 showed that the P L /F of Chinese mainland and North American routes still kept increasing, improving by 1.4 and 2.7 ppts, respectively. The P L /F of other routines decreased by 1.0-3.1 ppts. The Company is adding more capacity to Europe, to grasp the revival of demand of Europe. Freight business has maintained a relatively high boom, and P L /F has increased by 2 ppts to 68.6%.

We believe that the Company's H2 result prospects are mixed with recovery of demand continually and the moderate cost growth. The positive factor is the gradually fading fuel hedging losses, and the negative factor is the shrink of share of profit from Air China due to the exchange losses. We temporarily maintain the financial forecast and target price unchanged at HK$14.3 for the Company, reaffirming the accumulate rating.

Risk

Surging oil price

RMB depreciation

Demand affected by economy

Transformation program failed

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()